Missing from this article is how homeowners are being fraudulently foreclosed upon and how this affects title to the homes.

Once again, homeowners continue to get shafted by those in office.

Just because you have money doesn’t mean you made it because you’re smart!See Video Below…

ST. Pete Times-

TALLAHASSEE — The push is on in Florida to cut the courts out of the foreclosure process.

Supporters of the concept — which is used in nearly 30 states — say it will speed foreclosures, get houses back onto the real estate market and boost the economy.

Opponents say it puts property owners at the mercy of banks.

Gov. Rick Scott, House Speaker Dean Cannon and Senate President Mike Haridopolos all say they are interested in considering legislation to change Florida laws so judges won’t have to referee foreclosures.

Here is never-before-seen footage of Rick Scott during a deposition in an anti-trust lawsuit against his former company Columbia/HCA Health. Scott’s company was fined a record $1.7 billion on charges of Medicare fraud. Despite being a lawyer and being CEO of one of the nation’s largest hospital chains, Scott evades answers to even the most basic questions. If Scott won’t answer questions when under oath, how can we expect him to be honest with us?

Tuesday, August 2, 2011

10:00 AM – 12:00 PM

538 Dirksen Senate Office Building

The witnesses will be: Mr. Jack Hopkins, President and CEO, CorTrust Bank, on behalf of the Independent Community Bankers of America; and Ms. Faith Schwartz, Executive Director, Hope Now Alliance. Additional witnesses may be announced.

All hearings are webcasted live and Individuals with disabilities who require an auxiliary aid or service, including closed captioning service for webcast hearings, should contact the committee clerk at 202-224-7391 at least three business days in advance of the hearing date.

Witnesses

Panel 1

* Mr. Jack Hopkins

President and Chief Executive Officer

CorTrust Bank, on behalf of the Independent Community Bankers of America

* Ms. Faith Schwartz

Executive Director

Hope Now Alliance

T/O: At what point does the Florida Bar need to step in?

From Kim Miller:

Palm Beach County Chief Judge Peter Blanc said in a letter Wednesday to David J. Stern that Stern’s suggestions to deal with thousands of abandoned cases are not permitted by Florida rules of law.

On Monday, Stern wrote a letter to Palm Beach County Chief Judge Peter D. Blanc, pitching new strategies for the courts in dealing with his inevitable exit from the business of foreclosure prosecution. His letter places much of the blame on the lenders who ended their relationship with his firm but have not yet transferred the cases to new lawyers, leaving them in limbo and clogging up the overloaded courts.

WASHINGTON, D.C. – On Friday, March 4 at 10:00 a.m., the Congressional Oversight Panel for the Troubled Asset Relief Program (TARP) will convene in 538 Dirksen Senate Office Building to hold its final hearing. The Panel will hear expert testimony from the agencies who helped to coordinate the government’s unprecedented response to the 2008 financial crisis, as well as from several of the nation’s leading economists, who will offer their assessments of the TARP’s impact on financial stability and the U.S. economy.

By statute, the Congressional Oversight Panel will dissolve on April 3, 2011. The Panel will issue a final report on the TARP in mid-March.

WHO: Members of the TARP Congressional Oversight Panel

Witnesses

Panel One:

Timothy Massad, Acting Assistant Secretary for Office of Financial Stability, U.S. Department of Treasury

Panel Two:

Jason Cave, Deputy Director for Complex Financial Institutions Monitoring, Federal Deposit Insurance Corporation

Patrick Lawler, Chief Economist and Head of the Office of Policy Analysis and Research, Federal Housing Finance Agency

William R. Nelson (ADDED), Deputy Director, Division of Monetary Affairs, Federal Reserve System

Panel Three:

Joseph E. Stiglitz, Nobel Laureate and University Professor, Columbia Business School, Graduate School of Arts and Sciences (Department of Economics) and the School of International and Public Affairs

Allan H. Meltzer, Allan H. Meltzer University Professor of Political Economy at Carnegie Mellon University

Simon H. Johnson, Ronald A. Kurtz (1954) Professor of Entrepreneurship, MIT Sloan School of Management, and Senior Fellow, Peterson Institute for International Economics

Luigi Zingales, Robert C. McCormack Professor of Entrepreneurship and Finance and the David G. Booth Faculty Fellow, University of Chicago Booth School of Business

WHAT: Final Hearing on the TARP’s Impact on Financial Stability

WHEN: Friday, March 4, 2011; 10:00 a.m.

WHERE: Room 538, Dirksen Senate Office Building

The hearing is open to press and public and will be webcast on the Panel’s website at cop.senate.gov. Individuals with disabilities who require an auxiliary aid or service, including closed captioning service for webcast hearings, should contact the Panel’s staff at 202-224-9925 at least two business days in advance of the hearing date.

The Congressional Oversight Panel was created to oversee the expenditure of the Troubled Asset Relief Program funds authorized by Congress in the Emergency Economic Stabilization Act of 2008 and to provide recommendations on regulatory reform. The Panel members are former Senator Ted Kaufman; J. Mark McWatters; Richard H. Neiman, Superintendent of Banks for the State of New York; Damon Silvers, Policy Director and Special Counsel for the AFL-CIO; and Kenneth Troske, William B. Sturgill Professor of Economics at the University of Kentucky.

Members of the committee questioned Special Inspector General Barofsky and others about the quarterly report on the Troubled Asset Relief Program (TARP) and Home Affordable Mortgage Program (HAMP) . Chairman Rep. Darrell Issa, (R-CA) Witnesses: Neil Barofsky, special inspector general for the troubled asset relief program Department of the Treasury Tim Massad, Acting Assistant Secretary for Financial Stability and Chief Counsel

House Committee on Oversight & Reform hearing on latest SIGTARP report:

Thomas A. Cox is a retired bank lawyer in Portland, Maine who serves as the Volunteer Program Coordinator for the Maine Attorney’s Saving Homes (MASH) program. He represents homeowners in foreclosure, and assists and consults with other volunteer lawyers in providing pro bono legal services to these Maine homeowners.

Another Super Tremendous Job! Listen to her carefully for those of you who may not be aware of the secrets behind the modification game. She tells exactly how it’s playing out.

United States House of Representatives

Committee on the Judiciary

Hearing on: “Foreclosed Justice: Causes and Effects of the Foreclosure Crisis”

Written Testimony of

Christopher L. Peterson

Associate Dean for Academic Affairs and Professor of Law

University of Utah, S.J. Quinney College of Law

Salt Lake City, Utah

December 2, 2010

10:00 a.m.

It is an honor to appear today before this Committee. Thank you for the opportunity to share some thoughts on our national foreclosure crisis. My name is Christopher Peterson and I am the Associate Dean for Academic Affairs and a Professor of Law at the University of Utah where I teach contract and commercial law classes. I commend you, Chairman Conyers, Representative Smith, and other members of the Committee for organizing these hearings and for providing an opportunity to discuss this important and timely national issue.

The foreclosure crisis is an extremely complex problem. With so many fundamental changes, opportunities for moral hazard, agency cost problems, consumer abuses, and impending lawsuits, it is easy to lose track of some of the basic legal and business practice problems that departed from past traditions and helped bring us to our present situation. In particular, it is somewhat perplexing that relatively little attention has been paid to the one company that has been a party in more problematic mortgage loans than any other institution. Mortgage Electronic Registration Systems, Inc., commonly known as MERS, is a corporation registered in Delaware and headquartered in Reston, Virginia.1 MERS operates a computer database that includes some information on servicing and ownership rights of mortgage loans.2 Originators, servicers, and other financial institutions pay membership dues and per?transaction fees to MERS in exchange for the right to use and access MERS records.3 In addition to operating its computer database, MERS also pretends to own mortgage loans in order to help its members avoid paying fees to county governments.

My testimony is largely derived from two scholarly articles I have written on this topic which I invite the committee to review for further information.4 My prepared statement today will: (1) discuss the Origin and Business Practices of MERS; (2) explore the problematic legal foundation of MERS; (3) suggest that MERS is a deceptive and anti?democratic institution designed to deprive county governments of revenue; (4) explain how MERS is undermining mortgage loan and land title record keeping; (5) argue that MERS was a contributing factor in the foreclosure crisis and has made resolving foreclosures more difficult; and (6) propose some solutions for the committee to consider.

F. DANA WINSLOW

NYS SUPREME COURT JUSTICE

Before the House of Representatives

DECEMBER 2,2010

ON

CAUSES AND EFFECTS OF THE FORECLOSURE CRISIS

HOUSE OF REPRESENTATIVES COMMITTEE ON THE JUDICIARY

FORECLOSED JUSTICE:

CAUSES AND EFFECTS OF THE FORECLOSURE CRISIS

Hon. F. Dana Winslow

December 2, 2010

Excerpts:

3.2.4 Robo·signing. Questionable validity of signatures on assignments and affidavits

attesting to ownership of the Note and Mortgage. Examples:

3.2.4.1 Signed by: “Duly Authorized Officer,” “Authorized Signer,” “Attomey·in·

Fact” or “Authorized Agent.” What do these titles mean? What is the function

afthe person signing the documents, and what is the basis of their personal

knowledge?

3.2.4.2 Same person signs several documents, in several different capacities: e.g.,

“Vice President of [Assignor Mortgagee)” is also the “Assistant Secretary of

the Servicer” for the Plaintiff Mortgagee, and an employee of the law firm

bringing the foreclosure action.

3.2.5 Validity of notary stamps on assignments.

3.2.5.1 Assignment documents notarized several months after the assignment was

purportedly effected.

3.2.5.2 Notarized in blank – name of the person whose signature was purportedly

witnessed is omitted.

Written Testimony of

James A. Kowalski, Jr., Esquire

Law Offices of James A. Kowalski, Jr., PL

Jacksonville, FL

Before the

Committee On The Judiciary

United States House of Representatives

“Foreclosed Justice: Causes and Effects of the Foreclosure Crisis“

Excerpt:

The focus on speed is part of the business model for the servicers. As those of us

who have litigated these cases for years now, and as all of us now know as a result of the

robo-signing scandals, most of the servicers use “Signing Officers” – rows of individuals

who sit before reams of documents prepared by others, with not even a modest wink at

the business records exception to the hearsay rule, and who sign the documents only to

have the document transported across the business campus to rows of notaries, who attest

to the signatures without ever complying with the basics of their state’s notary laws.

Some of the mill firms now employ their own “Signing OffIcers” – individuals

who will sign Assignments of Mortgage on behalf of the owners of the pool, supposedly

authorized by the servicer pursuant to the Pooling and Servicing Agreement which

applies to the particular securitized trust. The documents are prepared entirely by the

servicer.

On occasion, the law fIrm employees also sign the AffIdavits in support of

motions for summary judgment fIled by the law fIrms – here, the lawyer’s offIce staff

becomes the material witness for the lawyer’s client.

Wednesday, December 1, 2010

09:30 AM – 01:00 PM

538 Dirksen Senate Office Building

The witnesses for Panel I will be: Ms. Phyllis Caldwell, Chief, Homeownership Preservation Office, United States Department of the Treasury; The Honorable Sheila C. Bair, Chairman, Federal Deposit Insurance Corporation; The Honorable Daniel K. Tarullo, Governor, Board of Governors of the Federal Reserve System; Mr. John Walsh, Acting Comptroller of the Currency, Office of the Comptroller of the Currency; and Mr. Edward DeMarco, Acting Director, Federal Housing Finance Agency. The witnesses for Panel II will be: Mr. Terry Edwards, Executive Vice President, Credit Portfolio Management, Fannie Mae; Mr. Donald Bisenius, Executive Vice President, Freddie Mac; Mr. Tom Deutsch, Executive Director, American Securitization Forum; and Professor Kurt Eggert, Professor of Law, Chapman University School of Law.

Individuals with disabilities who require an auxiliary aid or service, including closed captioning service for webcast hearings, should contact the committee clerk at 202-224-7391 at least three business days in advance of the hearing date.

Remarks of R.K. Arnold

President and CEO of MERSCORP, Inc.

Before the

Subcommittee on Housing and Community Opportunity

House Financial Services Committee

November 18, 201

Excerpts:

The MERS database is important to individual borrowers because it provides a free and

accessible resource where borrowers can locate their servicers, and in many cases, learn who

their note-owner is as they change over time.

<SNIP>

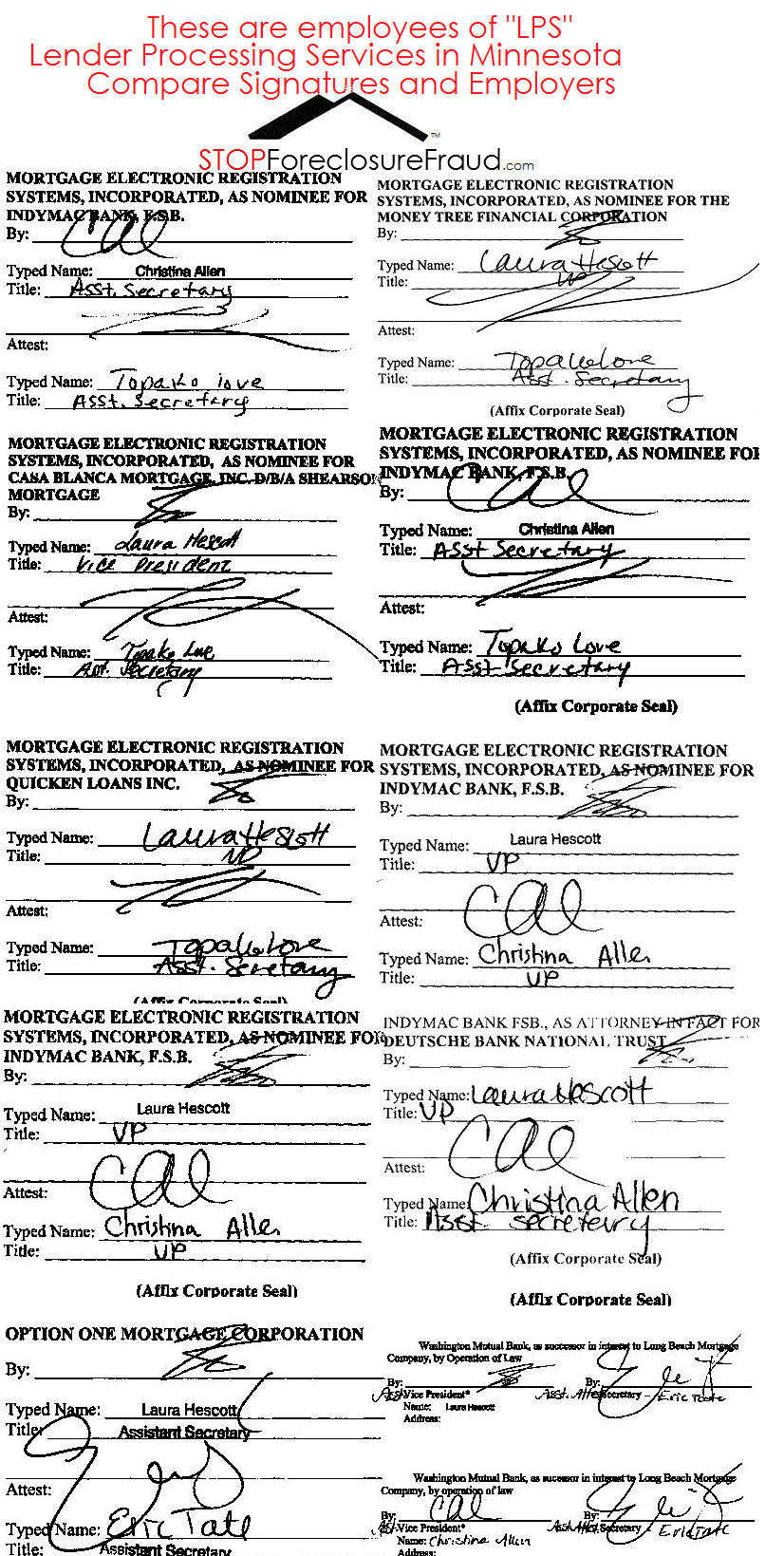

To do this, MERS relies on specially designated employees of its members, called

certifying officers, to handle the foreclosure. To be a MERS certifying officer, one must be an

officer of the member institution who is familiar with the functions to be performed, and who

has passed an examination administered by MERS. Generally, these are the same individuals

who would handle the foreclosure if the lender was involved without MERS.

In my opinion if this is a correct statement than without reading into the rest we have a problem because you see in the image below these are not designated employees or officer of the “member institution”…but were or are employees of LPS. Not to mention the obvious issues. I am not an attorney.

Testimony of Mr. R.K. Arnold, 11/16/2010

Senate Banking, Housing and Urban Affairs Committee

Excerpt:

Under the corporate law in Delaware (where MERS is incorporated), there is no requirement that an officer of a corporation also be an employee of that corporation. A corporation is allowed to appoint individuals to be officers without having to employ those individuals or even pay them. This concept is not limited to MERS. Corporations cannot operate without officers; they can and often do operate without employees. It is not uncommon for large organizations to have all its employees employed by an operating company and for those employees to be elected as officers of affiliated companies that are created for other purposes (all corporations are required by law to have officers to act for it). Even for loans where MERS is not the mortgagee, employees of the servicer are generally delegated the power to take actions (e.g., initiate foreclosures) and execute documents (e.g., lien releases and assignments) on behalf of the owner of the loan (and the servicer, in turn, may further delegate such authority to a third-party vendor).

<SNIP>

If the note-owner chooses to have Mortgage Electronic Registration Systems, Inc. foreclose, then the note-owner endorses the note in blank (if it has not already done so), making it bearer paper, and grants possession of the note to a MERS certifying officer. This makes MERS the noteholder. Since MERS is already the mortgagee in the land records, MERS is now able to legally begin the foreclosure process on behalf of the note-owner.

SFF is in search of “THE AGREEMENT” that might exist between “MERS” and “NOTE-OWNER”, might be an actual Trust or Trustee. But this is not in public records.

I was impressed with Mrs. Thompson and her knowledge. Excellent read with Mr. Levitin’s testimony.

Excerpts:

What robo-signing reveals is the contempt that servicers have long exhibited for rules, whether

the rules of court procedure flouted in the robo-signing scandal or the contract rules breached in

the common misapplication of payments or the rules for HAMP modifications, honored more

often in the breach than in reality. Servicers do not believe that the rules that apply to everyone

else apply to them. This lawless attitude, supported by financial incentives and too-often

tolerated by regulators, is the root cause of the robo-signing scandal, the failure of HAMP, and

the wrongful foreclosure of countless American families.

The falsification of judicial foreclosure documents is closely and directly tied to widespread

errors and maladministration of HAMP and non-HAMP modification programs, and the forcedplaced

insurance and escrow issues. Homeowners for decades have complained about servicer

abuses that pushed them into foreclosure without cause, stripped equity, and resulted, all too

often, in wrongful foreclosure. In recent months, investors have come to realize that servicers’

abuses strip wealth from investors as well.3 Unless and until servicers are held to account for

their behavior, we will continue to see fundamental flaws in mortgage servicing, with cascading

costs throughout our society. The lack of restraint on servicer abuses has created a moral hazard

juggernaut that at best prolongs and deepens the current foreclosure crisis and at worst threatens

our global economic security.

The current robo-signing scandal is a symptom of the flagrant disregard adopted by servicers as

to the basic legal and business conventions that govern most transactions. This flagrant

disregard has been carried through every aspect of servicer’s business model. Servicers rely on

extracting payments from borrowers as quickly and cheaply as possible; this model is at odds

with notions of due process, judicial integrity, or transparent financial accounting. The current

foreclosure crisis has exposed these inherent contradictions, but the failures and abuses are

neither new nor isolated. Solutions must include but go beyond addressing the affidavit and

ownership issues raised most recently. Those issues are merely symptoms of the core problem:

servicers’ failure to service loans, account for payments, limit fees to reasonable and necessary

ones, and provide loan modifications where appropriate and necessary to restore loans to

performing status.

Diane E. Thompson has represented low-income homeowners since 1994. She currently works of counsel for the National Consumer Law Center. From 1994 to 2007, Ms. Thompson represented individual low-income homeowners in East St. Louis at Land of Lincoln Legal Assistance Foundation. While at Land of Lincoln Legal Assistance, Ms. Thompson served as the Homeownership Specialist, providing assistance to casehandlers representing homeowners in 65 counties in downstate Illinois, and the Supervising Attorney of the Housing and Consumer unit of the East St. Louis office. She has served on the boards of the National Community Reinvestment Coalition and the Metropolitan St. Louis Equal Housing Opportunity Council. She was a member of the Consumer Advisory Council of the Federal Reserve Board from 2003-2005. Between 1995 and 2001, Ms. Thompson served as corporate counsel to the largest private nonprofit affordable housing provider in the East St. Louis metropolitan area. She received her B.A. from Cornell University and her J.D. from New York University.

Watched the hearing yesterday and Mr. Levitin was extremely impressive!

Please watch the video for explosive info regarding securitization, “Nothing-Backed Securities”…transfers are void!

Sorry for the quality but was the best I could do.

.

———————————————————————–

.

Written Testimony of

Adam J. Levitin

Associate Professor of Law

Georgetown University Law Center

Before the

Senate Committee on Banking, Housing, and Urban Affairs

“Problems in Mortgage Servicing from Modification to Foreclosure”

November 16, 2010

2:30 pm

Excerpts:

A number of events over the past several months have roiled the mortgage world, raising

questions about:

(1) Whether there is widespread fraud in the foreclosure process;

(2) Securitization chain of title, namely whether the transfer of mortgages in the

securitization process was defective, rendering mortgage-backed securities into non-mortgagebacked

securities;

(3) Whether the use of the Mortgage Electronic Registration System (MERS) creates

legal defects in either the secured status of a mortgage loan or in mortgage assignments;

(4) Whether mortgage servicers’ have defaulted on their servicing contracts by charging

predatory fees to borrowers that are ultimately paid by investors;

(5) Whether investors will be able to “putback” to banks securitized mortgages on the

basis of breaches of representations and warranties about the quality of the mortgages.

These issues are seemingly disparate and unconnected, other than that they all involve

mortgages. They are, however, connected by two common threads: the necessity of proving

standing in order to maintain a foreclosure action and the severe conflicts of interests between

mortgage servicers and MBS investors.

It is axiomatic that in order to bring a suit, like a foreclosure action, the plaintiff must

have legal standing, meaning it must have a direct interest in the outcome of the legislation. In

the case of a mortgage foreclosure, only the mortgagee has such an interest and thus standing.

Many of the issues relating to foreclosure fraud by mortgage servicers, ranging from more minor

procedural defects up to outright counterfeiting relate to the need to show standing. Thus

problems like false affidavits of indebtedness, false lost note affidavits, and false lost summons

affidavits, as well as backdated mortgage assignments, and wholly counterfeited notes,

mortgages, and assignments all relate to the evidentiary need to show that the entity bringing the

foreclosure action has standing to foreclose.

Concerns about securitization chain of title also go to the standing question; if the

mortgages were not properly transferred in the securitization process (including through the use

of MERS to record the mortgages), then the party bringing the foreclosure does not in fact own

the mortgage and therefore lacks standing to foreclose. If the mortgage was not properly

transferred, there are profound implications too for investors, as the mortgage-backed securities

they believed they had purchased would, in fact be non-mortgage-backed securities, which

would almost assuredly lead investors to demand that their investment contracts be rescinded,

thereby exacerbating the scale of mortgage putback claims.

Sorry about the quality…had to go with what I had at the time.

NOTE: Mr Arnold said there is 20,000 who sign 7 documents but not in this clip.

Ms. Diane E. Thompson Counsel National Consumer Law Center

Mr. R. K. Arnold President and CEO Mortgage Electronic Registration Systems, Inc

I wish I could have recorded this on HD so everyone can witness some of the lies the Bank Reps were telling. They are really out of touch with reality.

At one point when JPMorgan’s David Lowman began to speak some attendees stood up and yelled, then escorted out the room after a brief pause.

__

__

<SNIP>

SHELBY: I CAN SEE WHO OWNS THE MORTGAGE?

ARNOLD: There is no assignment if MERS is the Mortgagee

Problems in Mortgage Servicing From Modification to Foreclosure

Tuesday, November 16, 2010

02:30 PM – 05:00 PM

538 Dirksen Senate Office Building

The witnesses will be: The Honorable Tom Miller, Attorney General,State of Iowa; Ms. Barbara J. Desoer, President, Bank of America HomeLoans; Mr. David Lowman, CEO, Chase Home Lending; Mr. Adam J. Levitin,Associate Professor of Law, Georgetown University Law Center; and Ms.Diane Thompson, Counsel, National Consumer Law Center. Additional witnesses may be announced at a later date.

![[VIDEO] Highlights of Maine Attorney Thomas Cox: “Foreclosed Justice: Causes and Effects of the Foreclosure Crisis” Pt 2](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2011/01/ThomasCox8.jpg&w=100&h=57&zc=1&q=90)

![[VIDEO TRUTH] ATTY VANESSA G. FLUKER “WHY YOU WON’T GET A MODIFICATION”](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/12/VF2.jpg&w=100&h=57&zc=1&q=90)

![[VIDEO] POWERFUL FORECLOSURE TESTIMONY: Sandra Hines Tells House of Reps What Many Feel](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/12/SandraHinesDetroit.jpg&w=100&h=57&zc=1&q=90)

![[VIDEO] WITNESSES “MERS DECEPTION”: Foreclosed Justice: Causes and Effects of the Foreclosure Crisis PT 2](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/12/shellgames.jpg&w=100&h=57&zc=1&q=90)

![[2] Testimony of R.K. Arnold President and CEO of MERSCORP, Inc. Before the Subcommittee 11/18/2010](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/strawman2.jpg&w=100&h=57&zc=1&q=90)

![[1] Testimony of R.K. Arnold President and CEO of MERSCORP, Inc. Before the Senate Committee 11/16/2010](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/strawman3.jpg&w=100&h=57&zc=1&q=90)

![[UPDATE 3:15pm] R.K ARNOLD MERS CEO TO BE PRESENT Senate Banking Committee Hearing today, 11/16/2010 (Will be webcast)](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/video.jpg&w=100&h=57&zc=1&q=90)

{kind=link}

Recent Comments