“For the first time in the nation’s history, there is no longer an authoritative, public record of who owns land in each county,” testified Peterson.

Epoch Times-

Homeownership is fraught with many problems, especially during a recessionary period. A major problem can arise when the property is still encumbered with a fixed-rate mortgage (FRM), an adjustable-rate mortgage (ARM), or any other mortgage variation under FRM or ARM, including balloon mortgages and mortgage loans guaranteed by, for example, the Federal Housing Administration.

What is not public knowledge is that a title or a deed to a property, which should de facto decree full ownership, may not in fact do so, thus requiring costly litigation.

After the 60 Minutes Segment on Foreclosure Fraud on April 3, 2011, I was contacted by over 2,000 individuals, seeking help or wanting to help.

FOR ALL THOSE WHO WANT TO HELP RESEARCH THE DOCX FORGERY SCHEME:

1. Search the official records of your county and find all the Mortgage Assignments filed by Docx in 2009. Search by bank: Deutsche Bank, Bank of NY Mellon, U.S. Bank, HSBC, Wells Fargo, etc.

These are very recognizable. On each form, in the left hand corner, there is a statement that the Assignment was prepared by Docx in Alpharetta, GA.

For examples, click on the word PLEADINGS on the Home Page of www.frauddigest.com (my online magazine) – then click on the second entry – 10 Versions of Linda Green signatures on mortgage documents.

Print each example you find in your county Official Records. Identify and circle the name of the borrorwer/homeowner on each record.

2. Go Back to the Official Records. Search the name of each homeowner on the Docx Assignments for Lis Pendens.

Print the Lis Pendens that corresponds to the Assignment and staple these together.

Note that there will not be a Lis Pendens for every Assignment – many homeowners will have already handed over the keys or agreed to a short sale to avoid litigation.

3. Sort by Law Firm Preparing the Lis Pendens.

In Florida, for example, the firms using these Assignments will include Law Offices of David Stern, Law Offices of Marshall Watson, Shapiro & Fishman, Florida Default Law Group, Law Offices of Daniel Consuegra, Akerman & Senterfitt, Gladstone Law Group and many others.

These are the firms that continued to use the forged documents, never “noticing” that:

(1) the signatures varied so significantly that forgeries were likely;

(2) the same individuals used so many different job titles that the validity was unlikely;

(3) the dates of the Assignments indicated a fraudulent document because the Assignments came after the Lis Pendens.

4. Compile a report of these findings – LAW FIRMS USING FORGED AND FABRICATED DOCUMENTS TO FORECLOSE.

State plainly which law firms used these documents and attach the documents supporting your conclusions.

5. Send your reports to the following:

(1) your local State Attorney;

(2) the Disciplinary Committee of the Bar Association in your state;

(3) the FBI/attention: Mortgage Fraud Taskforce;

(4) the U.S. Attorney for your district;

(5) the Attorney General for your state;

(6) your country recorder;

(7) your area newspaper/television investigative reporter.

6. You may also sort by the BANK that used these fraudulent documents to take homes, and include that information in your reports.

Please send a .pdf file of your letter (without attachments) to szymoniak@mac.com.

If you are very ambitious, you may also add the face value of all of the Docx Assignments you locate so that you can report the total amount that banks took or tried to take using these forged and fabricated documents in 2009.

WHEN WE ALL COMPLETE THIS PROJECT, WE WILL MOVE ON TO FORGED AND FABRICATED ASSIGNMENTS PREPARED BY LAW FIRMS (such as David Stern in Florida and Baum in NY) AND OTHER SERVICERS.

Most Americans have never heard of it, but this mortgage industry holds interests in 50 percent of all U.S. home loans.

No, not Fannie Mae, or Freddie Mac either.

Mortgage Electronic Registration Systems, otherwise known as MERS, is a private firm that tracks ownership in hundreds of thousands of home loans. The computerized network allows banks to buy and sell mortgages without having to record the transfers at the county level.

An added bonus for the banks is the avoidance of county fees. When MERS is used to turn a regular mortgage into an investment, financial institutions don’t pay “recording fees,” which are usually small charges of between $50 and $100, to the counties where the underlying properties are physically located.

FOR IMMEDIATE RELEASE:

Greensboro, NC

March 2, 2011

Contact:

Jeff Thigpen, Guilford County Register of Deeds

Ph. 336-451-5300

Ph. 336-641-3239

jthigpe@co.guilford.nc.us

THIGPEN WANTS TO TAKE ON MORTGAGE GIANTS:

SEEKS INVESTIGATION OF “MERS” FOR REIMBURSEMENT OF $1.3 MILLION IN LOST REVENUE TO GUILFORD COUNTY

Guilford County Register of Deeds Jeff Thigpen announced today that he will be conferring with County Attorney Mark Payne, NC Attorney General and Secretary of State as to whether the Mortgage Electronic Registration Service (MERS) owes Guilford County fees estimated at $1.3 million in lost revenue from mortgage assignments. Thigpen also wants to review pending legal actions against MERS and consider options to protect the integrity of public land recordation offices.

“As Register of Deeds, I have two primary responsibilities in land records: a sworn duty to protect the chain of title and a fiduciary responsibility to collect recording fees. Quite frankly, MERS has undermined both. Through their own “private for-profit” Register of Deeds mortgage tracking office, MERS has created a dangerous centralization of power whose sole purpose is to protect and serve the interests of major banking conglomerates and undermine public recording offices,” said Thigpen.

“For me, the question is clear. Do we want land records in America to be governed by major banking conglomerates on Wall Street or the people and laws of the United States of America?”

MERS has an electronic registry and database system that tracks more than 65 million mortgages for its paid membership throughout the country and aides the mortgage backed securities trade in the secondary market. MERS is reportedly involved in 60% of US mortgage loans. It was established by some of the largest mortgage lenders in the United States including Wells Fargo, Chase Mortgage, Citi Mortgage, Countrywide Home Loans, Inc. and Bank of America among others in 1997. A number of class action lawsuits and civil racketeering suits have arisen against MERS recently, including a suit alleging its members owe California $60-120 billion for circumventing land recording fees.

MERS has also been at the center of recent foreclosure chaos.

Since the founding of America, counties in the United States have maintained public records of land, mortgages and deeds of trust, by maintaining indexes of grantors and grantees. Register of Deeds offices ensure transparency and an important check and balance in private property ownership. County recording practices have been in place for 300 years. “It is interesting that the first fundamental change in public land title recording systems was not initiated by publicly elected leaders, but a small group of mortgage industry insiders. Now it’s coming back to bite all of us- homeowners and taxpayers. MERS creates a system where only certain eyes see the data and what’s going on. I have a real problem with that as a Recorder.

Thigpen is asking for clarity on the California suit and others surrounding MERS business practices in packaging and repackages home owner loans through securitization. MERS has saved larger financial firms millions of dollars while avoiding recordation and payment of fees related to mortgage transfers.

Since 2005 there were 47,553 deeds of trust that list MERS as a beneficiary filed in the Guilford County Register of Deeds office. Experts have indicated that those kinds of loans are repackaged and sold two and four times on average under the MERS system. “One repackaging of MERS documents would have generated $665,742 if documentation had been filed in our office. Two repackaged loans would have generated $1,331,484. And that’s conservative estimate.”

Thigpen maintains the lost recording fees would help local elected officials reduce budget deficits and maintain core services such as public education and public safety in this time of fiscal crisis.

Thigpen’s primary concern relates to recent court rulings in Arkansas, Kansas, Maine and Missouri questioning MERS legal standing in home foreclosures and suits challenging that MERS filings may be fraudulent. “If MERS filings are false statements, there are laws that say if you decrease the money that you pay for a service through using those false statements then you can get damages. The legal term is “unjust enrichment”. Thigpen wants to explore unjust enrichment and other options related to recovery of lost revenue.

Thigpen acknowledges that NC General Statutes do not currently require assignments to be filed in local Register of Deeds offices which allow the public to know the rightful owner of a mortgage. “That may need to change among other things”, says Thigpen. Thigpen points to a major policy change from MERS in the past two weeks conceding that assignments should be filed in public registries across the country even if the state law does not require it and instructed members not to foreclose in MERS name. “It indicates to me that they know they need to fix this.”

“It used to be that if you bought a house, the mortgage would stay at a single bank until you paid it off. Times have changed. Through securitization, mortgages are all put in a blender and sold off to Wall Street investors and Fannie and Freddie among others. MERS has its finger on the spin button. At the end of the day with MERS, Susie Homeowner can’t keep track of who owns her loan and if she’s going to get hit with new fees or even foreclosure.

“This type of unregulated greed is giving charity to all the people who should be giving it and undermines good business practices.” says Thigpen. Thigpen points out those local credit unions like State Employees Credit Union who didn’t participate in sub-prime lending have avoided legal difficulties.

“This is a mess and the MERS system impacts millions of homeowners across the country in danger of having their homes foreclosed”, said Thigpen. He wants a review of the lawsuits and investigations into MERS by state attorney generals and others and believes it will take a coordinated at the local, state and federal level to resolve it. “To me these issues with MERS are simple. Are major banking conglomerates going to tell the truth or not; and are we going choose to have two standards of justice in America: one for Big Money and the other for the rest of us?

Thigpen will also join Southern Sussex Massachusetts Register of Deeds John O’Brian, Jr. in urging national organizations such as the International Association of Clerks, Recorders, Election Officials and Treasurers (IACREOT) to address MERS in the coming weeks.

National Association of Land Title Examiners and Abstractors

7490 Eagle Road

Waite Hill, OH 44094

February 10, 2011

Restoring Integrity to the Land Title Records – A Commentary on MERS

As the faults in the MERS system of mortgage tracking become ever more apparent, so do the consequences begin to take shape. And, as high profile cases of abuse of process rapidly hit the mainstream press, as details continue to emerge, we can see with ever increasing clarity the problems caused by the systematic omission of mortgage

assignments from the public land records.

Earnings at Bank of America, the largest U.S. lender, may suffer materially if using Mortgage Electronic Registration Systems or MERS is found to be invalid, according to a regulatory filing last week. Citigroup and PNC said fines or other penalties may result from investigations into MERS and allegations of faulty foreclosure practices.

“They’re recognizing the writing on the wall, that there are serious problems associated with the basic business model and legal theories of the MERS system,” Christopher L. Peterson, a law professor at the University of Utah in Salt Lake City who has written articles on Reston, Virginia-based MERS, said yesterday.

Laurence Platt, a partner at the firm K&L Gates, which defended Wells Fargo and US Bank in the Ibanez case, basically threatened the American homeowner with sky-high interest rates if the banks aren’t allowed to run their own private land recording system.

If local governments succeed in the fight against how banks have recorded the transfer of mortgage notes through the Mortgage Electronic Registration Systems, home loans could become as expensive as credit cards, K&L Gates Partner Laurence Platt said Wednesday […]

Platt admitted there were issues with the system, but he warned that scoring short-term political points could be the end of affordable housing.

“They are making secured credit unenforceable,” Platt said. “If you think you’re going to get 4% mortgages on unsecured loans, you’re wrong. You’re going to get credit card rates. MERS was designed to make it easy to transfer assignments in modern economics.”

This occurred on a panel at a meeting of the Mortgage Bankers Association, where Platt appeared with Georgetown Law Professor Adam Levitin, who has been critical of MERS. I corresponded with Levitin, and this was an accurate rendering of Platt’s remarks.

“My response was that’s nonsense,” Levitin wrote in an email. “No one, absolutely no one, is arguing that a valid security agreement should not be enforced. Instead, the issue is whether we should enforce invalid security interests or let parties that do not hold a security interest enforce someone else’s. I hardly think that denying parties that right will result in a change in the cost of credit. It might result in them changing law firms, however, to ones that didn’t screw up their securitization deals.”

A Utah court case in which the owner of a Draper townhouse got clear title to the property, even though he still owed $132,000 on it, raises new legal and financial questions about a property-records database created by mortgage bankers.

The award of a title free of liens means that whoever owns the promissory note on the Draper property — likely a group of faraway investors — no longer has the right to foreclose to collect on a delinquent loan. Indeed, the townhouse owner has sold the property and kept the money. Those who own the promissory note probably don’t even know what occurred.

Last year, the owner of the Draper property contacted attorney Walter T. Keane to help him deal with lenders, though Keane won’t say what the problem was and the owner declined an interview request.

The lawsuit over the title to the townhouse named Garbett Mortgage and Citibank FSB as the holders of promissory notes as recorded on trust deeds filed with the recorder’s office. Integrated Title Services was listed as trustee of the Garbett Mortgage trust deed, while First American Title was the trustee of the CitiBank trust deed.

But there also was another entity listed on the trust deeds called the Mortgage Electronic Registration Systems (MERS). The Mortgage Bankers Association, the Washington, D.C.-based trade group that represents major mortgage lenders, created MERS in the mid-1990s.

Under the state’s quiet title laws, Keane said he did not have to name MERS or serve it legal papers in the lawsuit because it was not the legal owner of title to the property. Those were title companies. In addition, attorneys contend, MERS cannot be the “beneficiary” or holder of the promissory note because it readily has admitted it has no financial interest in any notes or mortgages.

This article discusses some of the legal aspects of the Mortgage Electronic Registration Systems or “MERS” with regard to its potential legal liabilities and how these liabilities may affect related public companies.

We maintain that the potential legal liabilities faced by these companies are very large and may seriously injure their stock prices. We believe that the affiliates of MERS may be held liable for MERS violations based on various legal theories, including conspiracy, and if the courts pierce the corporate veil of MERS.

A list of some of the companies that may be affected is found at the end of this analysis.

MERS

MERS is a private non-stock Delaware member corporation that operates an electronic registry to track servicing rights and ownership of mortgage loans in the United States. MERS acts as a so-called “straw man.” MERS clouds land records as the purported owner of mortgages transferred by lenders, investors and loan servicers. MERS maintains that it eliminates the need to file assignments in the county land records with the purpose of lowering costs for lenders. This naturally reduces county recording revenues from real estate transfers.

Legal Issues Faced by MERS

Not Qualified to do Business in Most States

MERS is not qualified to business in most of the states in which it operates. The problem here is that MERS has allowed itself to be the plaintiff in many hundreds of thousands of mortgage foreclosures in states where it is not qualified to do business and therefore has no standing to sue. Most, 95% or more of these cases, were uncontested and therefore resulted in the loss of the defendants home after a telephone hearing that lasted a few minutes.

Remarks of R.K. Arnold

President and CEO of MERSCORP, Inc.

Before the

Subcommittee on Housing and Community Opportunity

House Financial Services Committee

November 18, 201

Excerpts:

The MERS database is important to individual borrowers because it provides a free and

accessible resource where borrowers can locate their servicers, and in many cases, learn who

their note-owner is as they change over time.

<SNIP>

To do this, MERS relies on specially designated employees of its members, called

certifying officers, to handle the foreclosure. To be a MERS certifying officer, one must be an

officer of the member institution who is familiar with the functions to be performed, and who

has passed an examination administered by MERS. Generally, these are the same individuals

who would handle the foreclosure if the lender was involved without MERS.

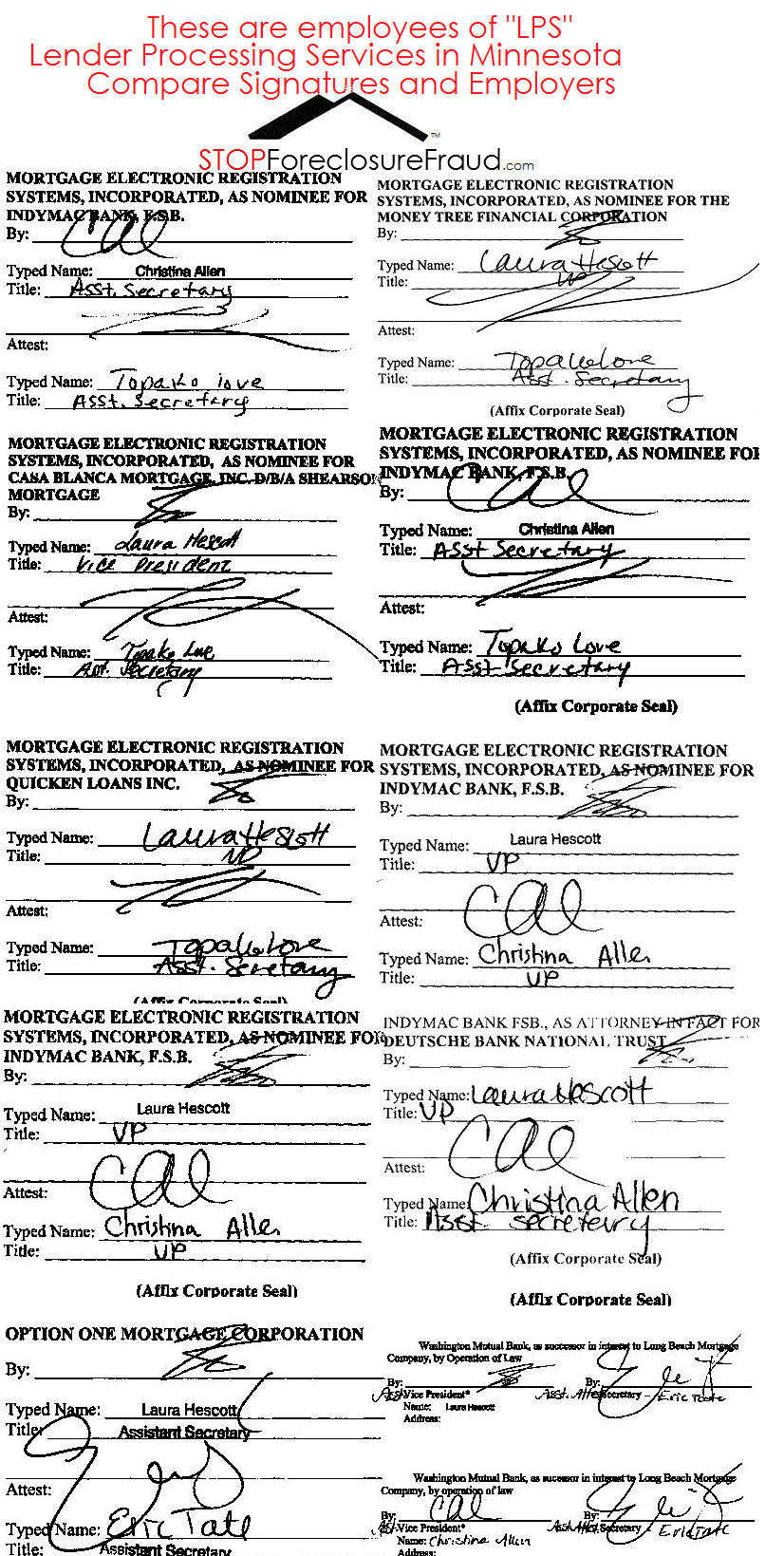

In my opinion if this is a correct statement than without reading into the rest we have a problem because you see in the image below these are not designated employees or officer of the “member institution”…but were or are employees of LPS. Not to mention the obvious issues. I am not an attorney.

Testimony of Mr. R.K. Arnold, 11/16/2010

Senate Banking, Housing and Urban Affairs Committee

Excerpt:

Under the corporate law in Delaware (where MERS is incorporated), there is no requirement that an officer of a corporation also be an employee of that corporation. A corporation is allowed to appoint individuals to be officers without having to employ those individuals or even pay them. This concept is not limited to MERS. Corporations cannot operate without officers; they can and often do operate without employees. It is not uncommon for large organizations to have all its employees employed by an operating company and for those employees to be elected as officers of affiliated companies that are created for other purposes (all corporations are required by law to have officers to act for it). Even for loans where MERS is not the mortgagee, employees of the servicer are generally delegated the power to take actions (e.g., initiate foreclosures) and execute documents (e.g., lien releases and assignments) on behalf of the owner of the loan (and the servicer, in turn, may further delegate such authority to a third-party vendor).

<SNIP>

If the note-owner chooses to have Mortgage Electronic Registration Systems, Inc. foreclose, then the note-owner endorses the note in blank (if it has not already done so), making it bearer paper, and grants possession of the note to a MERS certifying officer. This makes MERS the noteholder. Since MERS is already the mortgagee in the land records, MERS is now able to legally begin the foreclosure process on behalf of the note-owner.

SFF is in search of “THE AGREEMENT” that might exist between “MERS” and “NOTE-OWNER”, might be an actual Trust or Trustee. But this is not in public records.

Sorry about the quality…had to go with what I had at the time.

NOTE: Mr Arnold said there is 20,000 who sign 7 documents but not in this clip.

Ms. Diane E. Thompson Counsel National Consumer Law Center

Mr. R. K. Arnold President and CEO Mortgage Electronic Registration Systems, Inc

I wish I could have recorded this on HD so everyone can witness some of the lies the Bank Reps were telling. They are really out of touch with reality.

At one point when JPMorgan’s David Lowman began to speak some attendees stood up and yelled, then escorted out the room after a brief pause.

__

__

<SNIP>

SHELBY: I CAN SEE WHO OWNS THE MORTGAGE?

ARNOLD: There is no assignment if MERS is the Mortgagee

![[VIDEO] NBC Discusses MERS, Counties Seek Millions From Mortgage Giant](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2011/03/money_house1.jpg&w=100&h=57&zc=1&q=90)

![[2] Testimony of R.K. Arnold President and CEO of MERSCORP, Inc. Before the Subcommittee 11/18/2010](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/strawman2.jpg&w=100&h=57&zc=1&q=90)

![[1] Testimony of R.K. Arnold President and CEO of MERSCORP, Inc. Before the Senate Committee 11/16/2010](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/strawman3.jpg&w=100&h=57&zc=1&q=90)

{kind=link}

Recent Comments