Edward J. DeMarco Acting Director Federal Housing Finance Agency

Before the U.S. Senate Committee on Banking, Housing, and Urban Affairs On the State of the U.S. Housing Market: Removing Barriers to Economic Recovery

If William K. Black and Janet would only team up to write a book?

HuffPO-

There were many factors that contributed to our recent financial bubble: deregulation, cheap money from the Fed, failure to enforce remaining regulations, crony capitalism, hubris, speculation, leverage, and fraud among other problems. While fraud wasn’t the only issue, it was and is a significant contributor to the credit bubble. Restraining fraud is a necessary but not sufficient condition for a sound financial system. Congressional investigations in recent years have put ample evidence of fraud in the public domain.

To illustrate just one type of malicious mischief, Senator Carl Levin (D. Mich.), Chairman of a senate investigative panel, issued a memo stating that Goldman ” magnified the impact of toxic mortgages.” The Wall Street Journal reviewed data showing that a $38 million subprime-mortgage bond created in June 2006 was referenced in more than 30 debt pool causing around$280 million in losses to investors by 2008. In other words, Goldman kept repackaging, reselling or protecting (buying credit default protection on) losers. It took the wrong kind of nerve for Goldman’s CEO to say he was doing “God’s work.”

New York prosecutors are widening their probe into the manner in which Goldman Sachs (GS.N) marketed certain mortgage-linked securities before the financial crisis, the Wall Street Journal reported, citing people familiar with the matter.

StopForeclosureFraud received a similar memo from Fannie to GMAC, but this one addressed to JPMorgan Chase [see below]

Feep.com

In early December, a senior executive at Fannie Mae assured members of the Senate Banking Committee in Washington that the mortgage giant was doing everything possible to address the foreclosure crisis.

“Preventing foreclosures is a top priority for Fannie Mae,” Terence Edwards, an executive vice president, told the panel. “Foreclosures hurt families and destabilize communities.”

Yes, this is the same Mr. Dimon who last month complained that various new rules facing Wall Street “would damage America.” And it is the same JPMorgan that (unsuccessfully) lobbied lawmakers to kill plans for an independent consumer financial agency.

(Reuters) – The White House is considering Federal Reserve Governor Sarah Raskin and former Michigan Gov. Jennifer Granholm to head a new agency charged with protecting consumers of financial products, a source aware of the process said on Tuesday.

The consumer protection body will have broad powers to rein in abuses in the financial industry and was created in response to the aggressive and sometimes predatory lending practices that contributed to one of the worst financial crises in U.S. history in 2007-2009.

However its creation has been tarnished by a months-old logjam over who should head the agency. Law professor Elizabeth Warren, an outspoken consumer advocate and harsh critic of industry practices who had championed the bureau’s establishment, had been a leading candidate to run it but was seen as too confrontational to industry to overcome objections from Senate Republicans.

In hours of congressional hearings last week, the nation’s banks were repeatedly condemned for dual-track loan modification systems that give hope to homeowners seeking lower monthly payments while at the same time foreclosing on their properties behind their backs.

“Unacceptable deficiencies,” is how the acting director of the Federal Housing Finance Agency put it. Failed oversight, ineffective practices and insufficient staffing were criticisms added by other top regulators and legislators.

Boca Raton resident James Strassburger could have told lawmakers all that. He just wishes they were listening this year when One West Bank sold his home at foreclosure auction during negotiations for a loan modification.

Strassburger, 56, and his wife, Deborah, 58, who lived in their home for 19 years, were ordered out in May, holding two yard sales so they could squeeze into a rented apartment.

But the real kick in the gut came in August, six months after the auction, when they got a letter congratulating them for earning a trial loan modification. It was followed by a note alerting them to a hearing that would essentially give them their home back. Their mortgage payment was due Sept. 1, the letter reminded.

“This all could have been avoided. We could have been living our lives,” said James Strassburger, a former business owner whose flooring jobs dropped off when the economy fell. “It’s not a good feeling. I don’t like seeing my wife cry.”

One West Bank said it was looking into the Strassburgers’ case, but did not respond to a request for comment for this story.

Washington lawmakers began paying earnest attention to the nation’s foreclosure nightmare this fall as banks pulled back on their home repossessions after acknowledging assembly line-like processing systems had potentially illegal shortcomings.

Hastily prepared court documents, as well as the dual-track foreclosure and loan modification process, were discussed Wednesday in a hearing of the Senate Committee on Banking, Housing and Urban Affairs, and Thursday in the House Judiciary Committee.

Wednesday, December 1, 2010

09:30 AM – 01:00 PM

538 Dirksen Senate Office Building

The witnesses for Panel I will be: Ms. Phyllis Caldwell, Chief, Homeownership Preservation Office, United States Department of the Treasury; The Honorable Sheila C. Bair, Chairman, Federal Deposit Insurance Corporation; The Honorable Daniel K. Tarullo, Governor, Board of Governors of the Federal Reserve System; Mr. John Walsh, Acting Comptroller of the Currency, Office of the Comptroller of the Currency; and Mr. Edward DeMarco, Acting Director, Federal Housing Finance Agency. The witnesses for Panel II will be: Mr. Terry Edwards, Executive Vice President, Credit Portfolio Management, Fannie Mae; Mr. Donald Bisenius, Executive Vice President, Freddie Mac; Mr. Tom Deutsch, Executive Director, American Securitization Forum; and Professor Kurt Eggert, Professor of Law, Chapman University School of Law.

Individuals with disabilities who require an auxiliary aid or service, including closed captioning service for webcast hearings, should contact the committee clerk at 202-224-7391 at least three business days in advance of the hearing date.

Remarks of R.K. Arnold

President and CEO of MERSCORP, Inc.

Before the

Subcommittee on Housing and Community Opportunity

House Financial Services Committee

November 18, 201

Excerpts:

The MERS database is important to individual borrowers because it provides a free and

accessible resource where borrowers can locate their servicers, and in many cases, learn who

their note-owner is as they change over time.

<SNIP>

To do this, MERS relies on specially designated employees of its members, called

certifying officers, to handle the foreclosure. To be a MERS certifying officer, one must be an

officer of the member institution who is familiar with the functions to be performed, and who

has passed an examination administered by MERS. Generally, these are the same individuals

who would handle the foreclosure if the lender was involved without MERS.

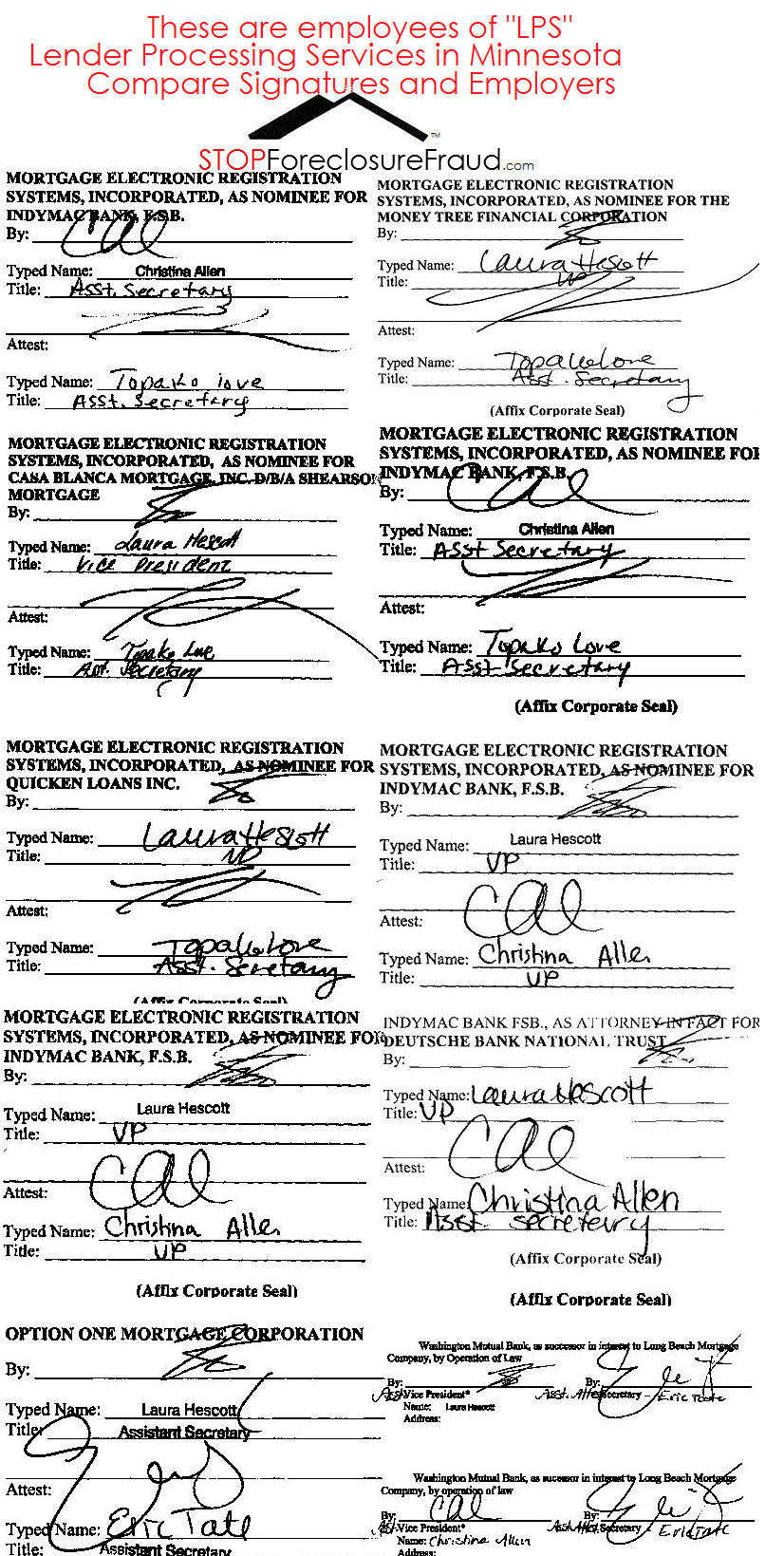

In my opinion if this is a correct statement than without reading into the rest we have a problem because you see in the image below these are not designated employees or officer of the “member institution”…but were or are employees of LPS. Not to mention the obvious issues. I am not an attorney.

Testimony of Mr. R.K. Arnold, 11/16/2010

Senate Banking, Housing and Urban Affairs Committee

Excerpt:

Under the corporate law in Delaware (where MERS is incorporated), there is no requirement that an officer of a corporation also be an employee of that corporation. A corporation is allowed to appoint individuals to be officers without having to employ those individuals or even pay them. This concept is not limited to MERS. Corporations cannot operate without officers; they can and often do operate without employees. It is not uncommon for large organizations to have all its employees employed by an operating company and for those employees to be elected as officers of affiliated companies that are created for other purposes (all corporations are required by law to have officers to act for it). Even for loans where MERS is not the mortgagee, employees of the servicer are generally delegated the power to take actions (e.g., initiate foreclosures) and execute documents (e.g., lien releases and assignments) on behalf of the owner of the loan (and the servicer, in turn, may further delegate such authority to a third-party vendor).

<SNIP>

If the note-owner chooses to have Mortgage Electronic Registration Systems, Inc. foreclose, then the note-owner endorses the note in blank (if it has not already done so), making it bearer paper, and grants possession of the note to a MERS certifying officer. This makes MERS the noteholder. Since MERS is already the mortgagee in the land records, MERS is now able to legally begin the foreclosure process on behalf of the note-owner.

SFF is in search of “THE AGREEMENT” that might exist between “MERS” and “NOTE-OWNER”, might be an actual Trust or Trustee. But this is not in public records.

I was impressed with Mrs. Thompson and her knowledge. Excellent read with Mr. Levitin’s testimony.

Excerpts:

What robo-signing reveals is the contempt that servicers have long exhibited for rules, whether

the rules of court procedure flouted in the robo-signing scandal or the contract rules breached in

the common misapplication of payments or the rules for HAMP modifications, honored more

often in the breach than in reality. Servicers do not believe that the rules that apply to everyone

else apply to them. This lawless attitude, supported by financial incentives and too-often

tolerated by regulators, is the root cause of the robo-signing scandal, the failure of HAMP, and

the wrongful foreclosure of countless American families.

The falsification of judicial foreclosure documents is closely and directly tied to widespread

errors and maladministration of HAMP and non-HAMP modification programs, and the forcedplaced

insurance and escrow issues. Homeowners for decades have complained about servicer

abuses that pushed them into foreclosure without cause, stripped equity, and resulted, all too

often, in wrongful foreclosure. In recent months, investors have come to realize that servicers’

abuses strip wealth from investors as well.3 Unless and until servicers are held to account for

their behavior, we will continue to see fundamental flaws in mortgage servicing, with cascading

costs throughout our society. The lack of restraint on servicer abuses has created a moral hazard

juggernaut that at best prolongs and deepens the current foreclosure crisis and at worst threatens

our global economic security.

The current robo-signing scandal is a symptom of the flagrant disregard adopted by servicers as

to the basic legal and business conventions that govern most transactions. This flagrant

disregard has been carried through every aspect of servicer’s business model. Servicers rely on

extracting payments from borrowers as quickly and cheaply as possible; this model is at odds

with notions of due process, judicial integrity, or transparent financial accounting. The current

foreclosure crisis has exposed these inherent contradictions, but the failures and abuses are

neither new nor isolated. Solutions must include but go beyond addressing the affidavit and

ownership issues raised most recently. Those issues are merely symptoms of the core problem:

servicers’ failure to service loans, account for payments, limit fees to reasonable and necessary

ones, and provide loan modifications where appropriate and necessary to restore loans to

performing status.

Diane E. Thompson has represented low-income homeowners since 1994. She currently works of counsel for the National Consumer Law Center. From 1994 to 2007, Ms. Thompson represented individual low-income homeowners in East St. Louis at Land of Lincoln Legal Assistance Foundation. While at Land of Lincoln Legal Assistance, Ms. Thompson served as the Homeownership Specialist, providing assistance to casehandlers representing homeowners in 65 counties in downstate Illinois, and the Supervising Attorney of the Housing and Consumer unit of the East St. Louis office. She has served on the boards of the National Community Reinvestment Coalition and the Metropolitan St. Louis Equal Housing Opportunity Council. She was a member of the Consumer Advisory Council of the Federal Reserve Board from 2003-2005. Between 1995 and 2001, Ms. Thompson served as corporate counsel to the largest private nonprofit affordable housing provider in the East St. Louis metropolitan area. She received her B.A. from Cornell University and her J.D. from New York University.

Watched the hearing yesterday and Mr. Levitin was extremely impressive!

Please watch the video for explosive info regarding securitization, “Nothing-Backed Securities”…transfers are void!

Sorry for the quality but was the best I could do.

.

———————————————————————–

.

Written Testimony of

Adam J. Levitin

Associate Professor of Law

Georgetown University Law Center

Before the

Senate Committee on Banking, Housing, and Urban Affairs

“Problems in Mortgage Servicing from Modification to Foreclosure”

November 16, 2010

2:30 pm

Excerpts:

A number of events over the past several months have roiled the mortgage world, raising

questions about:

(1) Whether there is widespread fraud in the foreclosure process;

(2) Securitization chain of title, namely whether the transfer of mortgages in the

securitization process was defective, rendering mortgage-backed securities into non-mortgagebacked

securities;

(3) Whether the use of the Mortgage Electronic Registration System (MERS) creates

legal defects in either the secured status of a mortgage loan or in mortgage assignments;

(4) Whether mortgage servicers’ have defaulted on their servicing contracts by charging

predatory fees to borrowers that are ultimately paid by investors;

(5) Whether investors will be able to “putback” to banks securitized mortgages on the

basis of breaches of representations and warranties about the quality of the mortgages.

These issues are seemingly disparate and unconnected, other than that they all involve

mortgages. They are, however, connected by two common threads: the necessity of proving

standing in order to maintain a foreclosure action and the severe conflicts of interests between

mortgage servicers and MBS investors.

It is axiomatic that in order to bring a suit, like a foreclosure action, the plaintiff must

have legal standing, meaning it must have a direct interest in the outcome of the legislation. In

the case of a mortgage foreclosure, only the mortgagee has such an interest and thus standing.

Many of the issues relating to foreclosure fraud by mortgage servicers, ranging from more minor

procedural defects up to outright counterfeiting relate to the need to show standing. Thus

problems like false affidavits of indebtedness, false lost note affidavits, and false lost summons

affidavits, as well as backdated mortgage assignments, and wholly counterfeited notes,

mortgages, and assignments all relate to the evidentiary need to show that the entity bringing the

foreclosure action has standing to foreclose.

Concerns about securitization chain of title also go to the standing question; if the

mortgages were not properly transferred in the securitization process (including through the use

of MERS to record the mortgages), then the party bringing the foreclosure does not in fact own

the mortgage and therefore lacks standing to foreclose. If the mortgage was not properly

transferred, there are profound implications too for investors, as the mortgage-backed securities

they believed they had purchased would, in fact be non-mortgage-backed securities, which

would almost assuredly lead investors to demand that their investment contracts be rescinded,

thereby exacerbating the scale of mortgage putback claims.

Sorry about the quality…had to go with what I had at the time.

NOTE: Mr Arnold said there is 20,000 who sign 7 documents but not in this clip.

Ms. Diane E. Thompson Counsel National Consumer Law Center

Mr. R. K. Arnold President and CEO Mortgage Electronic Registration Systems, Inc

I wish I could have recorded this on HD so everyone can witness some of the lies the Bank Reps were telling. They are really out of touch with reality.

At one point when JPMorgan’s David Lowman began to speak some attendees stood up and yelled, then escorted out the room after a brief pause.

__

__

<SNIP>

SHELBY: I CAN SEE WHO OWNS THE MORTGAGE?

ARNOLD: There is no assignment if MERS is the Mortgagee

Problems in Mortgage Servicing From Modification to Foreclosure

Tuesday, November 16, 2010

02:30 PM – 05:00 PM

538 Dirksen Senate Office Building

The witnesses will be: The Honorable Tom Miller, Attorney General,State of Iowa; Ms. Barbara J. Desoer, President, Bank of America HomeLoans; Mr. David Lowman, CEO, Chase Home Lending; Mr. Adam J. Levitin,Associate Professor of Law, Georgetown University Law Center; and Ms.Diane Thompson, Counsel, National Consumer Law Center. Additional witnesses may be announced at a later date.

![[2] Testimony of R.K. Arnold President and CEO of MERSCORP, Inc. Before the Subcommittee 11/18/2010](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/strawman2.jpg&w=100&h=57&zc=1&q=90)

![[1] Testimony of R.K. Arnold President and CEO of MERSCORP, Inc. Before the Senate Committee 11/16/2010](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/strawman3.jpg&w=100&h=57&zc=1&q=90)

![[UPDATE 3:15pm] R.K ARNOLD MERS CEO TO BE PRESENT Senate Banking Committee Hearing today, 11/16/2010 (Will be webcast)](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/video.jpg&w=100&h=57&zc=1&q=90)

{kind=link}

Recent Comments