Remarks of R.K. Arnold

President and CEO of MERSCORP, Inc.

Before the

Subcommittee on Housing and Community Opportunity

House Financial Services Committee

November 18, 201

Excerpts:

The MERS database is important to individual borrowers because it provides a free and

accessible resource where borrowers can locate their servicers, and in many cases, learn who

their note-owner is as they change over time.

<SNIP>

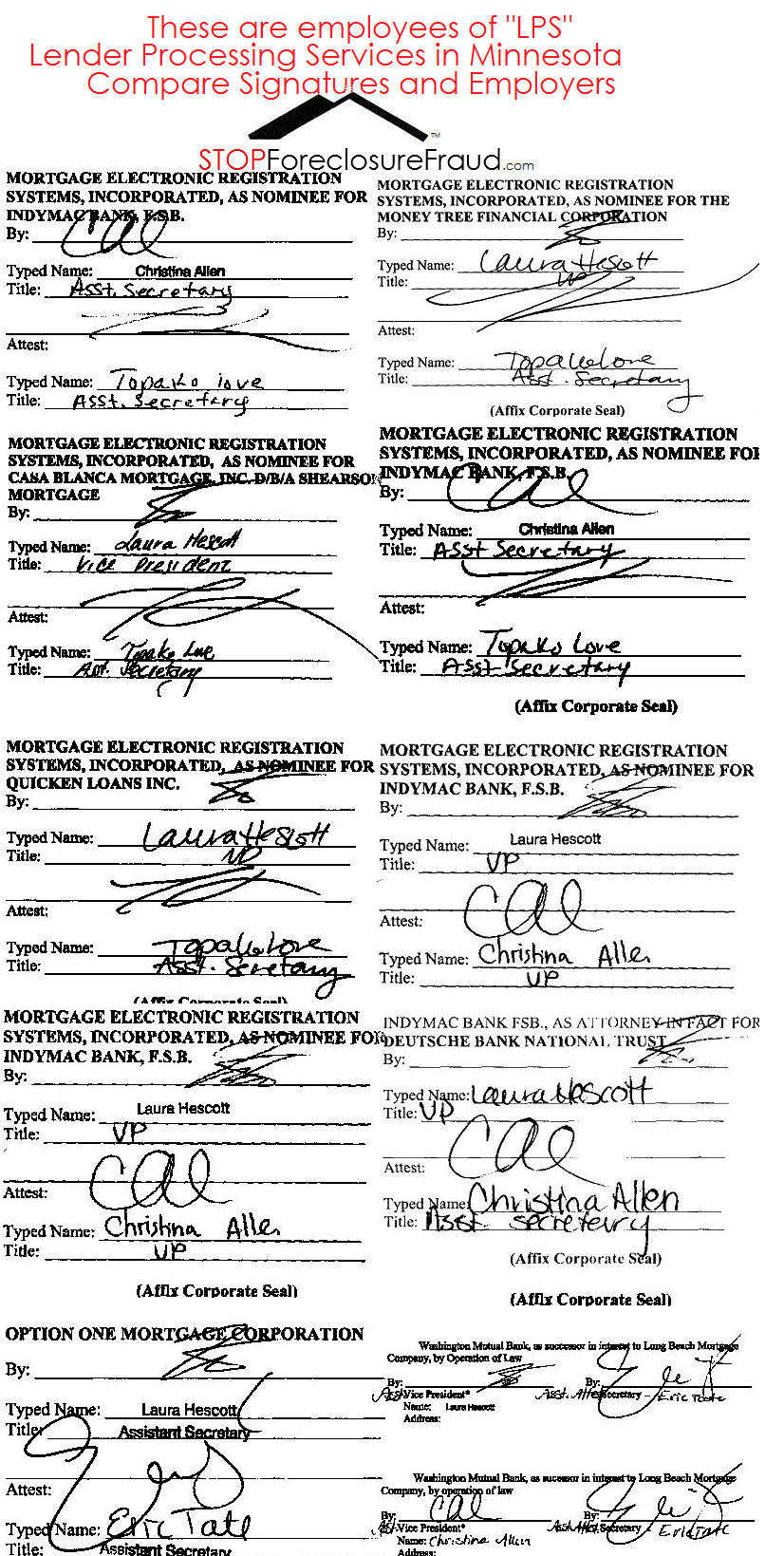

To do this, MERS relies on specially designated employees of its members, called

certifying officers, to handle the foreclosure. To be a MERS certifying officer, one must be an

officer of the member institution who is familiar with the functions to be performed, and who

has passed an examination administered by MERS. Generally, these are the same individuals

who would handle the foreclosure if the lender was involved without MERS.

In my opinion if this is a correct statement than without reading into the rest we have a problem because you see in the image below these are not designated employees or officer of the “member institution”…but were or are employees of LPS. Not to mention the obvious issues. I am not an attorney.

Testimony of Mr. R.K. Arnold, 11/16/2010

Senate Banking, Housing and Urban Affairs Committee

Excerpt:

Under the corporate law in Delaware (where MERS is incorporated), there is no requirement that an officer of a corporation also be an employee of that corporation. A corporation is allowed to appoint individuals to be officers without having to employ those individuals or even pay them. This concept is not limited to MERS. Corporations cannot operate without officers; they can and often do operate without employees. It is not uncommon for large organizations to have all its employees employed by an operating company and for those employees to be elected as officers of affiliated companies that are created for other purposes (all corporations are required by law to have officers to act for it). Even for loans where MERS is not the mortgagee, employees of the servicer are generally delegated the power to take actions (e.g., initiate foreclosures) and execute documents (e.g., lien releases and assignments) on behalf of the owner of the loan (and the servicer, in turn, may further delegate such authority to a third-party vendor).

<SNIP>

If the note-owner chooses to have Mortgage Electronic Registration Systems, Inc. foreclose, then the note-owner endorses the note in blank (if it has not already done so), making it bearer paper, and grants possession of the note to a MERS certifying officer. This makes MERS the noteholder. Since MERS is already the mortgagee in the land records, MERS is now able to legally begin the foreclosure process on behalf of the note-owner.

SFF is in search of “THE AGREEMENT” that might exist between “MERS” and “NOTE-OWNER”, might be an actual Trust or Trustee. But this is not in public records.

I was impressed with Mrs. Thompson and her knowledge. Excellent read with Mr. Levitin’s testimony.

Excerpts:

What robo-signing reveals is the contempt that servicers have long exhibited for rules, whether

the rules of court procedure flouted in the robo-signing scandal or the contract rules breached in

the common misapplication of payments or the rules for HAMP modifications, honored more

often in the breach than in reality. Servicers do not believe that the rules that apply to everyone

else apply to them. This lawless attitude, supported by financial incentives and too-often

tolerated by regulators, is the root cause of the robo-signing scandal, the failure of HAMP, and

the wrongful foreclosure of countless American families.

The falsification of judicial foreclosure documents is closely and directly tied to widespread

errors and maladministration of HAMP and non-HAMP modification programs, and the forcedplaced

insurance and escrow issues. Homeowners for decades have complained about servicer

abuses that pushed them into foreclosure without cause, stripped equity, and resulted, all too

often, in wrongful foreclosure. In recent months, investors have come to realize that servicers’

abuses strip wealth from investors as well.3 Unless and until servicers are held to account for

their behavior, we will continue to see fundamental flaws in mortgage servicing, with cascading

costs throughout our society. The lack of restraint on servicer abuses has created a moral hazard

juggernaut that at best prolongs and deepens the current foreclosure crisis and at worst threatens

our global economic security.

The current robo-signing scandal is a symptom of the flagrant disregard adopted by servicers as

to the basic legal and business conventions that govern most transactions. This flagrant

disregard has been carried through every aspect of servicer’s business model. Servicers rely on

extracting payments from borrowers as quickly and cheaply as possible; this model is at odds

with notions of due process, judicial integrity, or transparent financial accounting. The current

foreclosure crisis has exposed these inherent contradictions, but the failures and abuses are

neither new nor isolated. Solutions must include but go beyond addressing the affidavit and

ownership issues raised most recently. Those issues are merely symptoms of the core problem:

servicers’ failure to service loans, account for payments, limit fees to reasonable and necessary

ones, and provide loan modifications where appropriate and necessary to restore loans to

performing status.

Diane E. Thompson has represented low-income homeowners since 1994. She currently works of counsel for the National Consumer Law Center. From 1994 to 2007, Ms. Thompson represented individual low-income homeowners in East St. Louis at Land of Lincoln Legal Assistance Foundation. While at Land of Lincoln Legal Assistance, Ms. Thompson served as the Homeownership Specialist, providing assistance to casehandlers representing homeowners in 65 counties in downstate Illinois, and the Supervising Attorney of the Housing and Consumer unit of the East St. Louis office. She has served on the boards of the National Community Reinvestment Coalition and the Metropolitan St. Louis Equal Housing Opportunity Council. She was a member of the Consumer Advisory Council of the Federal Reserve Board from 2003-2005. Between 1995 and 2001, Ms. Thompson served as corporate counsel to the largest private nonprofit affordable housing provider in the East St. Louis metropolitan area. She received her B.A. from Cornell University and her J.D. from New York University.

Sorry about the quality…had to go with what I had at the time.

NOTE: Mr Arnold said there is 20,000 who sign 7 documents but not in this clip.

Ms. Diane E. Thompson Counsel National Consumer Law Center

Mr. R. K. Arnold President and CEO Mortgage Electronic Registration Systems, Inc

I wish I could have recorded this on HD so everyone can witness some of the lies the Bank Reps were telling. They are really out of touch with reality.

At one point when JPMorgan’s David Lowman began to speak some attendees stood up and yelled, then escorted out the room after a brief pause.

__

__

<SNIP>

SHELBY: I CAN SEE WHO OWNS THE MORTGAGE?

ARNOLD: There is no assignment if MERS is the Mortgagee

Problems in Mortgage Servicing From Modification to Foreclosure

Tuesday, November 16, 2010

02:30 PM – 05:00 PM

538 Dirksen Senate Office Building

The witnesses will be: The Honorable Tom Miller, Attorney General,State of Iowa; Ms. Barbara J. Desoer, President, Bank of America HomeLoans; Mr. David Lowman, CEO, Chase Home Lending; Mr. Adam J. Levitin,Associate Professor of Law, Georgetown University Law Center; and Ms.Diane Thompson, Counsel, National Consumer Law Center. Additional witnesses may be announced at a later date.

![[2] Testimony of R.K. Arnold President and CEO of MERSCORP, Inc. Before the Subcommittee 11/18/2010](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/strawman2.jpg&w=100&h=57&zc=1&q=90)

In my opinion if this is a correct statement than without reading into the rest we have a problem because you see in the image below these are not designated employees or officer of the “member institution”…but were or are employees of LPS. Not to mention the obvious issues. I am not an attorney.

![[1] Testimony of R.K. Arnold President and CEO of MERSCORP, Inc. Before the Senate Committee 11/16/2010](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/strawman3.jpg&w=100&h=57&zc=1&q=90)

![[UPDATE 3:15pm] R.K ARNOLD MERS CEO TO BE PRESENT Senate Banking Committee Hearing today, 11/16/2010 (Will be webcast)](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/video.jpg&w=100&h=57&zc=1&q=90)

{kind=link}

Recent Comments