In RE CitiGroup Inc. Securities Litigation![]()

[ipaper docId=43369450 access_key=key-1xh6fq0jmfhebnl0r7us height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.

Posted on 19 November 2010.

In RE CitiGroup Inc. Securities Litigation![]()

[ipaper docId=43369450 access_key=key-1xh6fq0jmfhebnl0r7us height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD2 Comments

Posted on 19 November 2010.

Excerpt from Daily Business Review:

Another 155 employees received pink slips Thursday from the Law Offices of David J. Stern and DJSP Enterprises, which processes home foreclosure cases for the Plantation-based law firm.

The layoffs came as Fannie Mae, which withdrew it business from the Stern firm after becoming one of its biggest clients, announced it had named eight law firms to handle foreclosure cases in Florida.

Here is the POA between FANNIE MAE and DJS 11.7.2008.

[ipaper docId=43372637 access_key=key-e4k2osxxhkg8hct1oz9 height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD0 Comments

![[READ] LEE COUNTY, FL SHERIFF CANDIDATE FORECLOSURE FRAUD LETTER TO CHIEF JUDGE CARY](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/Christian4x6_lessyellow_1.jpg&w=100&h=57&zc=1&q=90)

Posted on 19 November 2010.

Link to his site: Christian Meister

Just want to make it clear that no one from his office/party sent this to me.

[ipaper docId=43373487 access_key=key-1t11nhdq6z6u5z00k4p7 height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD1 Comment

Posted on 19 November 2010.

By Lorraine Woellert and Clea Benson – Nov 18, 2010 7:26 PM ET

U.S. homeowners are dropping out of the Obama administration’s foreclosure prevention program at a faster rate than they are joining it, according to figures released today by the U.S. Treasury Department.

Borrowers aided by the Home Affordable Modification Program grew to nearly 520,000 in October, up 23,750 from a month earlier, the Treasury said in its monthly report. The increase was less than five percent. A total of 36,300 borrowers have dropped out of the plan for failing to make their payments, an increase of 24 percent from a month earlier.

At a congressional hearing earlier in the day, lawmakers said HAMP, which pays lenders to modify loans and reduce monthly payments for struggling borrowers, isn’t doing enough to help homeowners falling behind on their mortgages amid high unemployment and depressed real estate values.

“It’s safe to say that HAMP isn’t meeting its goal of preventing foreclosures,” Representative Maxine Waters, a California Democrat, said at a House Financial Services subcommittee hearing after the Treasury provided a preview of the report.

The Treasury and the Department of Housing and Urban Development issue monthly progress reports on HAMP, a $50 billion program authorized by Congress in 2009. The program was targeted to reach more than 3 million homeowners by paying mortgage servicers $1,000 to rewrite loan terms and $1,000 annually as long as the borrower participates, up to three years.

![]()

Posted in STOP FORECLOSURE FRAUD1 Comment

Posted on 19 November 2010.

Via: Brian Davies

[ipaper docId=43321210 access_key=key-1q8ru668qzivy73w3hne height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD1 Comment

Posted on 18 November 2010.

Action Date: November 18, 2010

Location: WASHINGTON, DC

As the many problems (frauds) are exposed regarding documents used by mortgage-backed trusts in foreclosures, some revelations stand out. Literally millions of foreclosures by mortgage-backed trusts hinge on a Mortgage Assignment signed by an officer of Mortgage Electronic Registration Systems (“MERS”) showing that the mortgage in question was transferred to the trust by MERS. The “MERS officer” who signs the Mortgage Assignment is actually most often an employee of a mortgage servicing company that is paid by the trust.

MERS itself has only 50 employees and they are not involved in signing mortgage assignments to trusts. These servicing company employees sign as officers of MERS “as nominee for” a particular mortgage company or bank. They are not employees of the mortgage companies or employees of the original named lender, but their titles on the Mortgage Assignment belie this and typically read: “Linda Green, Vice President, Mortgage Electronic Registration Systems, Inc., as nominee for American Brokers Conduit.”

MERS president R.K. Arnold testified in Senate testimony earlier this week that there are over 20,000 MERS “certifying officers.” To become a MERS certifying officer, a mortgage servicing company employee need only complete an online form and pay $25.00. Because of the concealment of the actual employer on the Mortgage Assignments, it is easy enough for Courts, and homeowners, to believe that they are examining a document prepared by the lender that sold the mortgage to the trust, when, in fact, the signer was a servicing company clerk paid by the trust itself.

The representative of the GRANTOR is, in truth, a paid employee of the GRANTEE. In hundreds of thousands of cases, the authority is, therefore, misrepresented. It is now also coming to light that in tens of thousands of cases, the individuals signing these forms did not even sign their own names. The documents were made to look official because other mortgage servicing company employees signed as witnesses and then all four “signatures” were notarized by yet another mortgage servicing company employee. The titles were false, the signatures were forged, the “witnessing” was a lie, as was the notarization. Despite all of these false statements, the BIGGEST LIE on these documents is that the trust acquired the mortgage on the date stated plainly on the Mortgage Assignment. In truth, no such transfers ever took place as represented by these MERS certifying officers (or their stand-in forgers). The date chosen almost always corresponds not to an actual transfer, but to the date roughly corresponding to the time the loan went into default. The Mortgage Assignment was prepared only to provide “proof” that the trust owned the mortgage. Until courts require Trusts to come forward with actual proof that they acquired the mortgages in question, specifying whom they paid and how much they paid for each such trust-owned mortgage, the actual owner of these mortgages will never be known.

In response to the exposure of the widespread fraud in the securitization process, the American Bankers Association issued a statement essentially saying that Mortgage Assignments were unnecessary. Investors and regulators were told, however, that the trusts owned the mortgages and notes in each pool of mortgages and that valid Assignments of Mortgages had been obtained. Where the proof of ownership put forth by the trusts is a sworn statement by a MERS “certifying officer” who had no knowledge whatsoever of the transactions involved and did not even review documents related to the transactions, such proof of ownership should be deemed worthless by the Courts. Other litigants are not allowed to manufacture their own evidence and offer it as proof at trial – there should be no exception for mortgage-backed trusts.

In particular, where the “MERS Certifying Officer” is actually an employee of the law firm hired to handle the foreclosure, such documents should be stricken and sanctioned. “MERS Certifying Officers” should be the next group required to testify before Congress. Here are the statistics for one Florida county, Palm Beach County, regarding the number of Mortgage Assignments filed by Mortgage Electronic Registration Systems: January, 2009: 1,164; February, 2009: February, 2009: 1,230; March, 2009: March, 2009: 1,113. An examination of just one day’s (March 31, 2009) filed Mortgage Assignments reveals that the signers of these Assignments are the very same mortgage servicing company employees who signed the “no-actual knowledge” Affidavits that triggered the national scrutiny: Jeffrey Stephan from Ally, Erica Johnson-Seck from IndyMac, Crystal Moore from Nationwide Title Clearing, Liquenda Allotey from Lender Processing Services, Denise Bailey from Litton Loan Services, Noriko Colston, Krystal Hall, and other well-known professional signers from the mortgage servicing industry. The most frequent signers from that particular day were two lawyers, associates in the law firm representing the trusts, who signed as Assistant Secretary for Mortgage Electronic Registration Systems.

![]()

Posted in STOP FORECLOSURE FRAUD7 Comments

Posted on 18 November 2010.

Testimony of

Alan Jones

Operations Manager

Wells Fargo Home Mortgage Servicing

Before the

Subcommittee on Housing and Community Opportunity House Financial Services Committee

U.S. House of Representatives

November 18, 2010

As a company, Wells Fargo has followed three fundamental tenets:

Continue..

[ipaper docId=43160131 access_key=key-hhzo42k2ei0jk2kfh1l height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD1 Comment

Posted on 18 November 2010.

TESTIMONY OF

REBECCA MAIRONE

DEFAULT SERVICING EXECUTIVE

BANK OF AMERICA HOME LOANS

Before the

HOUSE FINANCIAL SERVICES

HOUSING AND COMMUNITY OPPORTUNITY SUBCOMMITTEE

WASHINGTON, DC

NOVEMBER 18, 2010

Excerpt:

When industry concerns arose with the foreclosure affidavit process, we took the step to stop foreclosure sales nationwide and launch a voluntary review of our foreclosure procedures. Thus far, we have confirmed the basis for our foreclosure decisions has been accurate. At the same time, however, we have not found a perfect process. There are areas where we clearly must improve, and we are committed to making needed changes.

We’ve also used this opportunity to further evaluate our modification program and identify additional enhancements we can make. We have done this based on feedback from you, our customers, community groups, investors, and from our regulators. We also are committed to a constructive dialogue with State Attorneys General, who have taken a leadership role on these issues.

Continue reading…

[ipaper docId=43162330 access_key=key-enbxztru4aybr6y0upd height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD2 Comments

Posted on 18 November 2010.

Testimony of Stephanie Mudick JPMorgan Chase Committee on Financial Services

Subcommittee on Housing and Community Opportunity United States House of Representatives November 18, 2010

Introduction

Chairwoman Waters, Ranking Member Capito, and Members of the Committee, thank you for inviting me to appear before you today. My name is Stephanie Mudick, and I am the head of the Office of Consumer Practices at JPMorgan Chase. I am grateful for the opportunity to discuss Chase’s loan servicing business, our wide-ranging efforts to enable borrowers to keep their homes and avoid foreclosure where possible, and the recent issues that have arisen relating to affidavits filed in connection with certain foreclosure proceedings.

JPMorgan Chase is committed to ensuring that all borrowers are treated fairly; that all appropriate measures short of foreclosure are considered; and that, if foreclosure is necessary, the foreclosure process complies with all applicable laws and regulations. As I will discuss in detail later in my testimony, we regret the errors that we have discovered in our processes, and we have worked hard to correct these processes so that we get them right. We take these issues very seriously.

Chase services about nine million mortgages across every state, representing over $1.2 trillion in loans to borrowers. In our role as servicer, we are responsible for administering loans on behalf of the owner of the loan, which sometimes is Chase itself, but more often is someone else – a government-sponsored enterprise (GSE), a government agency (such as the Federal Housing Administration or the Department of Veterans Affairs), a securitization trust, or another private investor.

I will first discuss Chase’s extensive efforts to help borrowers avoid foreclosure and then discuss the issues that led to our temporary halt to some foreclosures, as well as Chase’s enhanced procedures for the foreclosure process.

Continue reading…

[ipaper docId=43164317 access_key=key-sctpg7g3chhqynqn016 height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD0 Comments

Posted on 18 November 2010.

TESTIMONY OF

JOHN WALSH

ACTING COMPTROLLER OF THE CURRENCY

before the

SUBCOMMITTEE ON HOUSING AND COMMUNITY OPPORTUNITY

of the

COMMITTEE ON FINANCIAL SERVICES

U.S. HOUSE OF REPRESENTATIVES

November 18, 2010

Statement

Chairwoman Waters, Ranking Member Capito, and members of the Subcommittee, I appreciate this opportunity to discuss recently reported improprieties in the foreclosure processes used by several large mortgage servicers and actions that the Office of the Comptroller of the Currency (OCC) is taking to address these issues where they involve national banks. The occurrences of improperly executed documents and attestations raise concerns about the overall integrity of the foreclosure process and whether foreclosures may be inappropriately taking homes from their owners. These are serious matters that warrant the thorough investigation that is now underway by the OCC, other federal bank regulators, and other agencies.

<SNIP>

A key objective of theMERS examination is to assess MERS corporate governance, control systems,

and accuracy and timeliness of information maintained in the MERS system. Examiners assigned to MERS

will also visit on-site foreclosure examinations in process at the largest mortgage servicers to

determine how servicers are fulfilling their roles and responsibilities relative to MERS.

We are also participating in an examination being led by the FRB of Lender

Processing Services, Inc., which provides third-party foreclosure services to banks.

We expect to have most of our on-site examination work completed by mid to late

December. We then plan to aggregate and analyze the data and information from each of

these examinations to determine whether or what additional supervisory and regulatory

actions may be needed. We are targeting to have our analysis completed by the end of

January.

We recognize that the problems associated with foreclosure processes and

documentation have raised broader questions about the potential effect on the mortgage

market in general and the financial impact on individual institutions that may result from

litigation or other actions by borrowers and investors.

Continue below…

[ipaper docId=43153024 access_key=key-botkxuxnkfpspwwh724 height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD1 Comment

![[2] Testimony of R.K. Arnold President and CEO of MERSCORP, Inc. Before the Subcommittee 11/18/2010](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/strawman2.jpg&w=100&h=57&zc=1&q=90)

Posted on 18 November 2010.

Remarks of R.K. Arnold

President and CEO of MERSCORP, Inc.

Before the

Subcommittee on Housing and Community Opportunity

House Financial Services Committee

November 18, 201

Excerpts:

The MERS database is important to individual borrowers because it provides a free and

accessible resource where borrowers can locate their servicers, and in many cases, learn who

their note-owner is as they change over time.

<SNIP>

To do this, MERS relies on specially designated employees of its members, called

certifying officers, to handle the foreclosure. To be a MERS certifying officer, one must be an

officer of the member institution who is familiar with the functions to be performed, and who

has passed an examination administered by MERS. Generally, these are the same individuals

who would handle the foreclosure if the lender was involved without MERS.

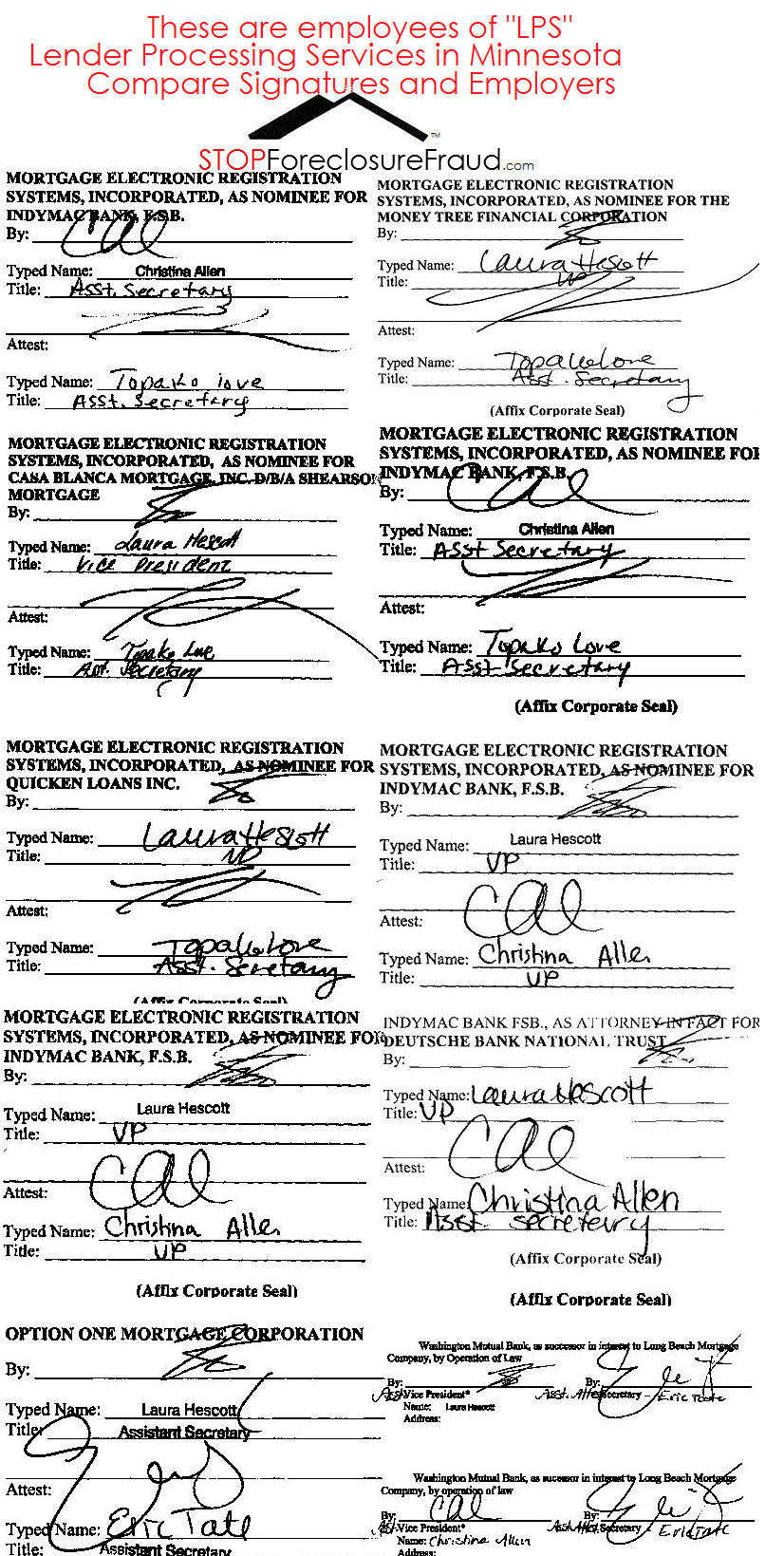

In my opinion if this is a correct statement than without reading into the rest we have a problem because you see in the image below these are not designated employees or officer of the “member institution”…but were or are employees of LPS. Not to mention the obvious issues. I am not an attorney.

continue reading…

[ipaper docId=43150268 access_key=key-so7aqstunj2ovylpk4q height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD0 Comments

![[1] Testimony of R.K. Arnold President and CEO of MERSCORP, Inc. Before the Senate Committee 11/16/2010](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/11/strawman3.jpg&w=100&h=57&zc=1&q=90)

Posted on 18 November 2010.

Testimony of Mr. R.K. Arnold, 11/16/2010

Senate Banking, Housing and Urban Affairs Committee

Excerpt:

Under the corporate law in Delaware (where MERS is incorporated), there is no requirement that an officer of a corporation also be an employee of that corporation. A corporation is allowed to appoint individuals to be officers without having to employ those individuals or even pay them. This concept is not limited to MERS. Corporations cannot operate without officers; they can and often do operate without employees. It is not uncommon for large organizations to have all its employees employed by an operating company and for those employees to be elected as officers of affiliated companies that are created for other purposes (all corporations are required by law to have officers to act for it). Even for loans where MERS is not the mortgagee, employees of the servicer are generally delegated the power to take actions (e.g., initiate foreclosures) and execute documents (e.g., lien releases and assignments) on behalf of the owner of the loan (and the servicer, in turn, may further delegate such authority to a third-party vendor).

<SNIP>

If the note-owner chooses to have Mortgage Electronic Registration Systems, Inc. foreclose, then the note-owner endorses the note in blank (if it has not already done so), making it bearer paper, and grants possession of the note to a MERS certifying officer. This makes MERS the noteholder. Since MERS is already the mortgagee in the land records, MERS is now able to legally begin the foreclosure process on behalf of the note-owner.

SFF is in search of “THE AGREEMENT” that might exist between “MERS” and “NOTE-OWNER”, might be an actual Trust or Trustee. But this is not in public records.

[ipaper docId=43143773 access_key=key-nawp01jx313c77qeisq height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD1 Comment

Posted on 18 November 2010.

Excerpt:

As an additional quality control measure, Citi is currently reviewing approximately 10,000 affidavits that were executed in pending judicial foreclosures initiated prior to February 2010 to assure that these affidavits are substantively correct and properly executed. Citi expects that affidavits executed prior to the fall of 2009 will need to be re-filed.

Separately, Citi is also reviewing approximately 4,000 pending foreclosure affidavits in judicial states that were executed at our Dallas processing center and may not have been signed in the presence of a notary, to assure that these affidavits are substantively correct and properly executed. Citi expects that it will re-file these affidavits.

Lastly, as previously announced, Citi stopped referring new matters to the Florida law firm David Stern in September of 2010 and has since withdrawn all pending matters from that firm. As an added precaution and quality-control measure, Citi is transferring approximately 8,500 pending foreclosure files from the Stern law firm to new counsel. New affidavits for these cases will be prepared and re-filed by new counsel under Citi’s current procedures.

Continue reading…

[ipaper docId=43133403 access_key=key-1dw6rv14xg9w76xg6k83 height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD1 Comment

Posted on 18 November 2010.

Excerpt:

The Court quiets title in favor of the plaintiff and against Diversified U.S. Holdings of Washington, LLC, Diversified Financial, Inc. and Northwest Commercial Bank […]

<SNIP>

Based upon the findings and conclusions , Plaintiff is granted a net JUDGMENT for $110, 923, plus interest thereonof judgment at the rate of the loan documents of 18.9%. from the date

[ipaper docId=43059595 access_key=key-26nipxiv758aqevmtyra height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD2 Comments

Posted on 17 November 2010.

By Alan Zibel, Of DOW JONES NEWSWIRES

WASHINGTON -(Dow Jones)- Federal bank regulators are conducting examinations of two companies that banks use to process foreclosures, amid concerns that banks cut corners on thousands of foreclosure documents, Acting Comptroller of the Currency John Walsh said Wednesday.

Walsh, in remarks prepared for delivery Thursday, said his agency is examining Reston, Va.-based Mortgage Electronic Registration Systems in conjunction with the Federal Reserve, the Federal Deposit Insurance Corp. and the Federal Housing Finance Agency.

That company, known as MERS, lets lenders package and sell mortgages without recording each transaction with county property offices.

It has come under fire from critics, who say MERS doesn’t have the right to act as the legal representative of the mortgage owner in foreclosure cases.

![]()

Posted in STOP FORECLOSURE FRAUD3 Comments

Posted on 17 November 2010.

AMI has consistently supported federal remedial programs to offer eligible, distressed, homeowners relief from foreclosure through modifications through HAMP and 2MP. Additionally, we support principal forgiveness and total debt realignment. No first lien modification will be sustainable without properly addressing a borrower’s total mortgage debt. Regrettably, these programs have often proven unsuccessful due to the servicers, who invariably are the second lien holders, and who continue to inhibit sustainable modifications. Mortgage investors have no control over the modification process, and therefore share many of the frustrations that homeowners and state Attorneys General are experiencing when dealing with mortgage servicers.

“All too often, homeowners are being victimized by the servicers’ past and ongoing actions. The time is now for a permanent solution to America’s housing crisis,” continued Katopis.

[ipaper docId=43010181 access_key=key-s8nvqyfv3r1sacetcwf height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD1 Comment

Posted on 17 November 2010.

“Our company’s process for preparing foreclosure affidavits was flawed”

“There were affidavits signed outside the immediate physical presence of a notary and without direct personal knowledge of the information in the affidavit”

“These flaws are entirely unacceptable to me”

[ipaper docId=43009585 access_key=key-15r3zmuzvsk1rrbsdz6k height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD1 Comment

Posted on 17 November 2010.

So lets recap a few important events that happened in the past and just recently:

9/4 FL AG confident there is a great deal of fraud

10/18 Moving Files via 18 Wheeler (Deposition of Kelly Scott)

11/2 Fannie and Freddie “remove” files from a Foreclosure Firm

Freddie’s spokeswoman said an internal review raised “concerns about some of the practices at the Stern firm.”

11/4 Law Firm announces cut backs

11/4 Document and Shredding Service

So exactly who is keeping track of documents going, going and gone?

Posted in STOP FORECLOSURE FRAUD4 Comments

Posted on 17 November 2010.

Highlights:

Check it out below:

NOTE: Not saying this is an actual machine used, for demonstration only of amazing technology today!

Here is the work of Robo-Scanners “signing” Satisfaction of Mortgages/ Discharges below…no different!

Only that the above uses a “real pen” that a real human can use.

I also included MERS exec. sigs at the end…

[ipaper docId=42947649 access_key=key-1khopfb5zy15wihne1na height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD2 Comments

Posted on 17 November 2010.

I was impressed with Mrs. Thompson and her knowledge. Excellent read with Mr. Levitin’s testimony.

Excerpts:

What robo-signing reveals is the contempt that servicers have long exhibited for rules, whether

the rules of court procedure flouted in the robo-signing scandal or the contract rules breached in

the common misapplication of payments or the rules for HAMP modifications, honored more

often in the breach than in reality. Servicers do not believe that the rules that apply to everyone

else apply to them. This lawless attitude, supported by financial incentives and too-often

tolerated by regulators, is the root cause of the robo-signing scandal, the failure of HAMP, and

the wrongful foreclosure of countless American families.

The falsification of judicial foreclosure documents is closely and directly tied to widespread

errors and maladministration of HAMP and non-HAMP modification programs, and the forcedplaced

insurance and escrow issues. Homeowners for decades have complained about servicer

abuses that pushed them into foreclosure without cause, stripped equity, and resulted, all too

often, in wrongful foreclosure. In recent months, investors have come to realize that servicers’

abuses strip wealth from investors as well.3 Unless and until servicers are held to account for

their behavior, we will continue to see fundamental flaws in mortgage servicing, with cascading

costs throughout our society. The lack of restraint on servicer abuses has created a moral hazard

juggernaut that at best prolongs and deepens the current foreclosure crisis and at worst threatens

our global economic security.

The current robo-signing scandal is a symptom of the flagrant disregard adopted by servicers as

to the basic legal and business conventions that govern most transactions. This flagrant

disregard has been carried through every aspect of servicer’s business model. Servicers rely on

extracting payments from borrowers as quickly and cheaply as possible; this model is at odds

with notions of due process, judicial integrity, or transparent financial accounting. The current

foreclosure crisis has exposed these inherent contradictions, but the failures and abuses are

neither new nor isolated. Solutions must include but go beyond addressing the affidavit and

ownership issues raised most recently. Those issues are merely symptoms of the core problem:

servicers’ failure to service loans, account for payments, limit fees to reasonable and necessary

ones, and provide loan modifications where appropriate and necessary to restore loans to

performing status.

Continue to the testimony below…

[ipaper docId=42936886 access_key=key-1uwm2jv8el3gfezslrfk height=600 width=600 /]

Diane E. Thompson, Of Counsel

Diane E. Thompson has represented low-income homeowners since 1994. She currently works of counsel for the National Consumer Law Center. From 1994 to 2007, Ms. Thompson represented individual low-income homeowners in East St. Louis at Land of Lincoln Legal Assistance Foundation. While at Land of Lincoln Legal Assistance, Ms. Thompson served as the Homeownership Specialist, providing assistance to casehandlers representing homeowners in 65 counties in downstate Illinois, and the Supervising Attorney of the Housing and Consumer unit of the East St. Louis office. She has served on the boards of the National Community Reinvestment Coalition and the Metropolitan St. Louis Equal Housing Opportunity Council. She was a member of the Consumer Advisory Council of the Federal Reserve Board from 2003-2005. Between 1995 and 2001, Ms. Thompson served as corporate counsel to the largest private nonprofit affordable housing provider in the East St. Louis metropolitan area. She received her B.A. from Cornell University and her J.D. from New York University.

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD1 Comment

Posted on 17 November 2010.

Via: Foreclosure Blues

(735 ILCS 5/15-1504) (from Ch. 110, par. 15-1504)

Sec. 15-1504.

Pleadings and service.

(a) Foundational requirements for affidavits. Every

affidavit filed in a foreclosure proceeding shall include a

detailed description of the basis of the affiant’s claimed

personal knowledge of the facts set forth in the affidavit,

including:

(1) a statement of which specific data systems the

affiant queried in preparing the affidavit, if the affiant

queried data systems in preparing the affidavit;

(2) a detailed factual statement of the basis of the

affiant’s belief that each data system identified

contained accurate information; and

(3) if applicable, a detailed description of the basis

of the affiant’s statement that the attached mortgage and

note are true and correct.

(b) Lost note affidavit. A copy of the mortgage and note

secured thereby shall be attached to the foreclosure complaint.

If any note required to be attached to a complaint filed

pursuant to this subsection (b) cannot be located for filing as

an exhibit, the moving party shall file an affidavit stating

the following:

…Continue reading

[ipaper docId=42890168 access_key=key-1evhfznhq9n2i4nmv45j height=600 width=600 /]

© 2010-19 FORECLOSURE FRAUD | by DinSFLA. All rights reserved.Posted in STOP FORECLOSURE FRAUD0 Comments

Posted on 17 November 2010.

Watched the hearing yesterday and Mr. Levitin was extremely impressive!

Please watch the video for explosive info regarding securitization, “Nothing-Backed Securities”…transfers are void!

Sorry for the quality but was the best I could do.

———————————————————————–

.

Georgetown University Law Center

Before the

Senate Committee on Banking, Housing, and Urban Affairs

“Problems in Mortgage Servicing from Modification to Foreclosure”

November 16, 2010

2:30 pm

Excerpts:

A number of events over the past several months have roiled the mortgage world, raising

questions about:

(1) Whether there is widespread fraud in the foreclosure process;

(2) Securitization chain of title, namely whether the transfer of mortgages in the

securitization process was defective, rendering mortgage-backed securities into non-mortgagebacked

securities;

(3) Whether the use of the Mortgage Electronic Registration System (MERS) creates

legal defects in either the secured status of a mortgage loan or in mortgage assignments;

(4) Whether mortgage servicers’ have defaulted on their servicing contracts by charging

predatory fees to borrowers that are ultimately paid by investors;

(5) Whether investors will be able to “putback” to banks securitized mortgages on the

basis of breaches of representations and warranties about the quality of the mortgages.

These issues are seemingly disparate and unconnected, other than that they all involve

mortgages. They are, however, connected by two common threads: the necessity of proving

standing in order to maintain a foreclosure action and the severe conflicts of interests between

mortgage servicers and MBS investors.

It is axiomatic that in order to bring a suit, like a foreclosure action, the plaintiff must

have legal standing, meaning it must have a direct interest in the outcome of the legislation. In

the case of a mortgage foreclosure, only the mortgagee has such an interest and thus standing.

Many of the issues relating to foreclosure fraud by mortgage servicers, ranging from more minor

procedural defects up to outright counterfeiting relate to the need to show standing. Thus

problems like false affidavits of indebtedness, false lost note affidavits, and false lost summons

affidavits, as well as backdated mortgage assignments, and wholly counterfeited notes,

mortgages, and assignments all relate to the evidentiary need to show that the entity bringing the

foreclosure action has standing to foreclose.

Concerns about securitization chain of title also go to the standing question; if the

mortgages were not properly transferred in the securitization process (including through the use

of MERS to record the mortgages), then the party bringing the foreclosure does not in fact own

the mortgage and therefore lacks standing to foreclose. If the mortgage was not properly

transferred, there are profound implications too for investors, as the mortgage-backed securities

they believed they had purchased would, in fact be non-mortgage-backed securities, which

would almost assuredly lead investors to demand that their investment contracts be rescinded,

thereby exacerbating the scale of mortgage putback claims.

Pay Close Attention To What He Says

[ipaper docId=42884106 access_key=key-4dwbkeca3hxlgeiw15x height=600 width=600 /]

Posted in STOP FORECLOSURE FRAUD4 Comments

© 2010-20 FORECLOSURE FRAUD | Managed by INNZES SOLUTIONS.

{kind=link}

Recent Comments