Thousands of foreclosures across the city are in question because paperwork used to justify the seizure of homes is riddled with flaws, a Daily News probe has found.

Banks have suspended some 4,450 foreclosures in all five boroughs because of paperwork problems like missing and inaccurate documents, dubious signatures and banks trying to foreclose on mortgages they don’t even own.

The city’s not alone. All 50 states are investigating foreclosure paperwork, evicted homeowners are hiring lawyers and buyers of foreclosed homes are fretting over the legality of their purchases.

Last week, New York‘s top judge, Jonathan Lippman, began requiring all bank lawyers to sign a form vouching for the accuracy of their foreclosure paperwork.

That could have been a problem for one Long Island foreclosure that was being brought by GMAC Mortgage last year.

A sworn affidavit dated March 30 was signed by someone identified as Sherry Hall, vice president of a GMAC affiliate called Homecomings Financial Network.

Fifteen days later another sworn affidavit surfaced in another Suffolk County foreclosure, this time signed by a GMAC vice president named Sheri D. Hall.

Despite the difference in the names, the signatures were identical – and were vouched for by the same notary.

Suffolk Supreme Court Justice Peter Mayer refused to approve the foreclosure bearing the name Sherry Hall and ordered her, and the notary, to appear in court Nov. 17. GMAC officials did not return calls.

Today the Florida Attorney General issued Subpoenas Duces Tecum’s to both Lender Processing Services Inc. and to a subsidiary DOCX. This involves employees past or present, the four foreclosure firms currently being investigated.

Both Assistant AG’s “McCollum’s Angels” June Clarkson and Theresa Edwards are doing an outstanding job!

STATE OF FLORIDA

OFFICE OF THE ATTORNEY GENERAL

DEPARTMENT OF LEGAL AFFAIRS

______________________________________

ECONOMIC CRIMES

INVESTIGATIVE SUBPOENA DUCES TECUM

“You,” “Your” or “DOC X” as used herein means DOCX, L.L.c. and any ofthe respondents, their agents and employees or any “affiliate” of the aforementioned entities, as that term is herein defined. Your agents include but are not limited to your officers, directors, attorneys, accountants, CPA’s, advertising consultants, or advertising account representatives. Any document in the possession ofyou, your affiliates, your agents or your employees is deemed to be within your possession or control. You have the affirmative duty to contact your agents, affiliates and employees and to obtain documentation from them, if such documentation is responsive to this subpoena.

B. Unless otherwise indicated, documents to be produced pursuant to this subpoena should include all original documents prepared, sent, dated, received, in effect, or which otherwise came into existence at any time. If your “original” is a photocopy, then the photocopy would be and should be produced as the original.

C. This subpoena duces tecum calls for the production of all responsive documents in your possession, custody or control without regard to the physical location ofsaid documents.

D. “And” and “or” are used as terms of inclusion, not exclusion.

E. The documents to be produced pursuant to each request should be segregated and specifically identified to indicate clearly the particular numbered request to which they are responsIve.

F. In the event that you seek to withhold any document on the basis that is properly entitled to some privilege or limitation, please provide the following information:

1. A list identifying each document for which you believe a limitation exists;

2. The name of each author, writer, sender or initiator of such document or thing, if any;

3. The name of each recipient, addressee or party for whom such document or thing was intended, ifany;

4. The date of such document, if any, or an estimate thereof so indicated if no date appears on the document;

5. The general subject matter as described in such document, or, if no such description appears, then such other description sufficient to identify said document; and

6. The claimed grounds for withholding the document, including, but not limited to, the nature of any claimed privilege and grounds in support thereof.

G. For each request, or part thereof, which is not fully responded to pursuant to a privilege, the nature of the privilege and grounds in support thereof should be fully stated.

H. If you possess, control or have custody of no documents responsive to any of the numbered requests set forth below, state this fact in your response to said request.

1. For purposes of responding to this subpoena, the term “document” shall mean all writings or stored data or information ofany kind, in any form, including the originals and all nonidentical copies, whether different from the originals by reason of any notation(s) made on such copies or otherwise, including, without limitation: correspondence, notes, letters, telegrams, minutes, certificates, diplomas, contracts, franchise agreements and other agreements, brochures, pamphlets, forms, scripts, reports, studies, statistics, inter-office and intra-office communications, training materials, analyses, memoranda, statements, summaries, graphs, charts, tests, plans, arrangements, tabulations, bulletins, newsletters, advertisements, computer printouts, teletype, telefax, microfilm, e-mail, electronically stored data, price books and lists, invoices, receipts, inventories, regularly kept summaries or compilations of business records, notations of any type of conversations, meetings, telephone or other communications, audio and videotapes; electronic, mechanical or electrical records or representations of any kind (including without limitation tapes, cassettes, discs, magnetic tapes, hard drives and recordings to include each document translated, if necessary, through detection devices into reasonably usable form).

1. For purposes of responding to this subpoena, the term “affiliate” shall mean: a corporation, partnership, business trust, joint venture or other artificial entity which effectively controls, or is effectively controlled by you, or which is related to you as a parent or subsidiary or sibling entity. “Affiliate” shall also mean any entity in which there is a mutual identity of any officer or director. “Effectively controls” shall mean having the status of owner, investor (if 5% or more of voting stock), partner, member, officer, director, shareholder, manager, settlor, trustee, beneficiary or ultimate equitable owner as defined in Section 607.0505(11)(e), Florida Statutes.

K. The term “Florida affiliates” shall mean those of your affiliates which do business in Florida or which are licensed to do business in Florida.

L. If production of documents or other items required by this subpoena would be, in whole or in part, unduly burdensome, or if the response to an individual request for production may be aided by clarification of the request, contact the Assistant Attorney General who issued this subpoena to discuss possible amendments or modifications of the subpoena, within five (5) days of receipt ofsame.

M. Documents maintained in electronic form must be produced in their native electronic form with all metadata intact. Data must be produced in the data format in which it is typically used and maintained. Moreover, to the extent that a responsive Document has been electronically scanned (for any purpose), that Document must be produced in an Optical Character Recognition (OCR) format and an opportunity provided to review the original Document. In addition, documents that have been electronically scanned must be in black and white and should be produced in a Group IV TIFF Format (TIF image format), with a Summation format load file (dii extension). DII Coded data should be received in a (Comma-Separated Values) CSV format with a pipe (I) used for multivalue fields. Images should be single page TIFFs, meaning one TIFF file for each page of the Document, not one .tifffor each Document. Ifthere is no text for a text file, the following should be inserted in that text file: “Page Intentionally Left Blank.”

Moreover, this Subpoena requires all objective coding for the production, to the extent it exists. For electronic mail systems using Microsoft Outlook or LotusNotes, provide all responsive emails and, if applicable, email attachments and any related Documents, in their native file format (i.e., .pst for Outlook personal folder, .nsf for LotusNotes). For all other email systems, provide all responsive emails and, if applicable, email attachments and any related Documents in OCR and TIFF formats as described above.

P. The relevant time period for the present request shall be from January 1, 2006 to present unless otherwise specifically stated. YOU ARE HEREBY COMMANDED to produce at said time and place all documents, as defined above, relating to the following subjects:

1. Copies ofall “Network Agreements” between DOCX and any law firm with offices located in the State of Florida.

2. Copies of any and all underlying documentation that allows for your employee or ex-employee, Linda Green to sign documents in the following capacities:

a. Vice President of Loan Documentation, Wells Fargo Bank, N.A. successor by merger to Wells Fargo Home Mortgage, Inc.; ;

b. Vice President, Mortgage Electronic Registration Systems, Inc. as nominee for American Home Mortgage Acceptance, Inc.;

c. Vice President, American Home Mortgage Servicing as successor-in-interest to Option One Mortgage Corporation;

d. Vice President, Mortgage Electronic Registration Systems, Inc. as nominee for American Brokers Conduit;

e. Vice President & Asst. Secretary, American Home Mortgage Servicing, Inc., as servicer for Ameriquest Mortgage Corporation;

f. Vice President, Option One Mortgage Corporation;

g. Vice President, Mortgage Electronic Registration Systems, Inc. as nominee for HLB Mortgage;

h. Vice President, American Home Mortgage Servicing, Inc.;

1. Vice President, Mortgage Electronic Registration Systems, Inc. as nominee for Family Lending Services, Inc.;

J. Vice President, American Home Mortgage Servicing, Inc. as Successor -ininterest to Option One Mortgage Corporation;

k. Vice President, Argent Mortgage Company, LLC by Citi Residential Lending, Inc., attorney-in-fact;

m. Vice President, Amtrust Funsing (sic) Services, Inc., by American Home Mortgage Servicing, Inc., as Attorney-in -fact;

n. Vice President, Seattle Mortgage Company.

3. Copies of every document signed in any capacity by Linda Green.

4. Copies of any and all underlying documentation that allows for your employee or ex-employee, Korell Harp to sign documents in any capacity for any lender and/or servicing company.

5. Copies of any and all underlying documentation that allows for your employee or ex-employee, Jessica Ohde to sign documents in any capacity for any lender and/or servicing company.

6. Copies of any and all underlying documentation that allows for your employee or ex-employee, Pat Kingston to sign documents in any capacity for any lender and/or servicing company.

7. Copies of any and all underlying documentation that allows for your employee or ex-employee, Christina Huang to sign documents in any capacity for any lender and/or servicing company.

8. Copies of any and all underlying documentation that allows for your employee or ex-employee, Tywanna Thomas to sign documents in any capacity for any lender and/or servicing company.

9. All policy and procedure manuals and/or training materials regarding the methods and timing that DOCX uses, including without limitation relating to the drafting and/or execution of foreclosure and mortgage related documents, including but not limited to Assignments of Mortgage, Satisfactions ofMortgage and Affidavits ofany and all kind.

10. A list ofall employees, dates ofhire and termination, and their duties, including whether or not they provide any notary services for DOCX.

11. All documents in your possession regarding any contracts with Florida Default Law Group, P.L., The Law Offices of David J. Stem, P.A., Shapiro & Fishman, L.L.P. and The Law Offices of Marshall C. Watson, P.A., including contracts regarding payments to or from any of those entities.

12. Documents relating to the relationship between DOCX and NewTrac and/or NewInvoice, including but not limited to, documents relating to the types ofdocuments that are or can be generated or are requested to be generated.

13. Any price lists published in any manner to prospective customers, whether by printed or electronic means.

14. All communications between DOCX and Florida Default Law Group, P.L., The Law Offices of David J. Stem, P.A., Shapiro & Fishman, L.L.P. or The Law Offices ofMarshall C. Watson, P.A. relating to procedures, policies, instructions or performance ofthe creation, backdating, modification, amendment, or other alteration ofany real property-related transactional document or records, including assignments, satisfactions ofmortgage, affidavits, notes, allonges, or other documents filed in any court.

15. Ledgers ofall financial transactions between DOCX and Florida Default Law Group, P.L., The Law Offices of David J. Stem, P.A., Shapiro & Fishman, L.L.P. or The Law Offices of Marshall C. Watson, P .A.

16. Ledgers ofall financial transactions between DOCX and any title company, recording service, process server, or any other entity that provides payments to DOCX in connection with any services rendered in connection with any residential foreclosure.

17. Ledgers ofall financial transactions between DOCX and any title company, recording service, process server, or any other entity to whom DOCX provides payment(s) in connection with any services rendered in connection with any residential foreclosure.

WITNESS the FLORIDA OFFICE OF THE ATTORNEY GENERAL in Fort Lauderdale, Florida, this 13th day of October, 2010.

June M. Clarkson

Assistant Attorney General

Florida Bar Number: 785709

OFFICE OF THE ATTORNEY GENERAL 110 S.E. 6th Street, 10th Floor

Fort Lauderdale, Florida 33301

Telephone: 954-712-4600

Facsimile: 954-712-4658

Theresa B. Edwards

Assistant Attorney General

Florida Bar Number: 252794

NOTE: In accordance with the Americans with Disabilities Act of 1990, persons needing a special accommodation to participate in this proceeding should contact George Rudd, Assistant Attorney General at (954) 712-4600 no later than seven days prior to the proceedings. Ifhearing impaired, contact the Florida Relay Service 1-800-955-8771 (TDD); or 1-800-955-8770 (Voice), for assistance.

AUTHORITY

Florida Statute 501.206

501.206 Investigative powers of enforcing authority.(

1) If, by his own inquiry or as a result ofcomplaints, the enforcing authority has reason to believe that a person has engaged in, or is engaging in, an act or practice that violates this part, he may administer oaths and affinnations, subpoena witnesses or matter, and collect evidence. Within 5 days excluding weekends and legal holidays, after the service ofa subpoena or at any time before the return date specified therein, whichever is longer, the party served may file in the circuit court in the county in which he resides or in which he transacts business and serve upon the enforcing authority a petition for an order modifying or setting aside the subpoena. The petitioner may raise any objection or privilege which would be available under this chapter or upon service of such subpoena in a civil action. The subpoena shall infonn the party served of his rights under this subsection.

(2) If matter that the enforcing authority seeks to obtain by subpoena is located outside the state, the person subpoenaed may make it available to the enforcing authority or his representative to examine the matter at the place where it is located. The enforcing authority may designate representatives, including officials ofthe state in which the matter is located, to inspect the matter on his behalf, and he may respond to similar requests from officials ofother states.

(3) Upon failure ofa person without lawful excuse to obey a subpoena and upon reasonable notice to all persons affected, the enforcing authority may apply to the circuit court for an order compelling compliance.

(4) The enforcing authority may request that the individual who refuses to comply with a subpoena on the ground that testimony or matter may incriminate him be ordered by the court to provide the testimony or matter. Except in a prosecution for perjury, an individual who complies with a court order to provide testimony or matter after asserting a privilege against selfincrimination to which he is entitled by law shall not have the testimony or matter so provided, or evidence derived there from, received against him in any criminal investigation proceeding.

(5) Any person upon whom a subpoena is served pursuant to this section shall comply with the tenns thereof unless otherwise provided by order of the court. Any person who fails to appear with the intent to avoid, evade, or prevent compliance in whole or in part with any investigation under this part or who removes, destroys, or by any other means falsifies any documentary material in the possession, custody, or control of any person subject to any such subpoena, or knowingly conceals any relevant infonnation with the intent to avoid, evade, or prevent compliance shall be liable for a civil penalty of not more than $5,000, reasonable attorney’s fees, and costs.

This is without question the most important decision so far in the war against the unlawful and fraudulent conduct of the originators, securitizers, out-source-providers, default servicers, and their so-called lawyers! The Judge articulates the business models we are dealing with better than anyone has done in any opinion, article or brief. I am sure your work contributed greatly to the education of the court and for that you should be highly commended. This Judge really and truly got it! It is the perfect outline of the transactional requirements and debunks every bogus argument that the other side has been advancing for year”.

O. MAX GARNDER III-

Dear Damian,

I have attached a sampling from my Amicus Brief filed on Friday, October 1, 2010 with the Massachusetts Supreme Judicial Court in the landmark cases that are presently on appeal from the Massachusetts Land Court styled: U.S. Bank v. Ibanez and its companion case, Wells Fargo Bank v. LaRace.

My brief reveals groundbreaking evidence that Antonio Ibanez’s loan was most likely securitized twice – a hidden fact unknown until now.

Moreover, the Assignment of Mortgage allegedly conveying the Ibanez loan to U.S. Bank, executed by “robo-signer” Linda Green, violated the Pooling and Servicing Agreement and other Trust documents.

Finally I expose the fact that U.S. Bank, who bought the Ibanez property at foreclosure for $94,350, sold it on December 15, 2008 for $0.00. That’s right, they foreclosed on Ibanez’s property so that they could give it away!

With respect to Mark and Tammy LaRace, I am happy to report that through the efforts of Attorney Glenn F. Russell, Jr. and myself, the LaRaces moved back into their home in January of this year, two and a half years post-foreclosure!

My Amicus Brief reveals that Wells Fargo Bank’s own documents prove that they did not have the authority to foreclose on the LaRaces. Therefore, the Assignment of Mortgage, Power of Attorney, Affidavit, and Foreclosure Deed executed by “robo-signer” Cindi Ellis were all unauthorized.

Wells Fargo Bank’s recent statement that it does not have the same “document” problem that GMAC, JPMorgan Chase, and Bank of America have admitted to is simply not true. I have audited many, many foreclosure files where Wells Fargo Bank employees and their agents have manufactured false documents to prosecute wrongful foreclosures such as in the LaRaces’ case.

DEUTSCHE BANK TRUST COMPANY AMERICAS AS TRUSTEE, Plaintiff(s),

v.

DEREK McCOY; EDYTA McCOY; MORTGAGE ELECTRONIC REGISTRATION SYSTEMS, INC. AS NOMINEE FOR HOMECOMINGS FINANCIAL, LLC, (F/K/A HOMECOMINGS FINANCIAL NETWORK, INC.) BOARD OF MANAGERS OF THE SILVER CHASE CONDOMINIUM; “JOHN DOE #1-5 AND “JANE DOE #1-5” SAID NAMES BEING FICTITIOUS, IT BEING THE INTENTION OF Plaintiff TO DESIGNATE ANY AND ALL OCCUPANTS, TENANTS, PERSONS OR CORPORATIONS, IF ANY, HAVING OR CLAIMING AN INTEREST IN OR LIEN UPON THE PREMISES BEING FORECLOSED HEREIN, Defendant(s).

7782-2008. Supreme Court, Suffolk County.

Decided September 21, 2010. Fein, Such & Crane, LLP, 747 Chestnut Ridge Road, Chestnut Ridge, New York 10977-6216, Attorneys for Plaintiff.

Derek McCoy, Edyta McCoy, 35 Gibbs Road, Coram, New York 11727, Defendants Pro Se.

PETER H. MAYER, J.

UPON DUE DELIBERATION AND CONSIDERATION BY THE COURT of the foregoing papers, the motion is decided as follows: it is

ORDERED that plaintiff’s resubmitted application (seq. # 002) for an order of reference in this foreclosure action is considered under 2009 NY Laws, Ch. 507, enacted December 15, 2009, and 2008 NY Laws, Ch. 472, enacted August 5, 2008 (as amended), as well as the related statutes and case law, and is hereby denied without prejudice, and with leave to resubmit upon proper papers, for the reasons set forth herein; and it is further

ORDERED that, inasmuch as the plaintiff has failed to properly show that the homeowner-defendants are not entitled to a foreclosure settlement conference, pursuant to CPLR 3408 such conference is hereby scheduled for November 17, 2010, 9:30 a.m., in the courtroom of the undersigned, located at Room A-259, Part 17, One Court Street, Riverhead, NY 11901 (XXX-XXX-XXXX), for the purpose of holding settlement discussions pertaining to the rights and obligations of the parties under the mortgage loan documents, including but not limited to, determining whether the parties can reach a mutually agreeable resolution to help the defendant avoid losing their home, and evaluating the potential for a resolution in which payment schedules or amounts may be modified or other workout options may be agreed to, and for whatever other purposes the Court deems appropriate; and it is further

ORDERED that “Sherry Hall,” who purports, in this particular case, to be the Vice President of Homecomings Financial Network, Inc., the purported attorney-in-fact for the plaintiff, shall appear at the November 17, 2010 Foreclosure Settlement Conference; and it is further

ORDERED that “Nikole Shelton,” the individual who purportedly notarized Ms. Hall’s signature in this particular action, as well as in the action entitled GMAC Mortgage, LLC v Ingoglia, under Suffolk County Index Number XXXX-XXXX, shall appear at the November 17, 2010 Conference; and it is further

ORDERED that any attorney appearing at the conference on behalf of the plaintiff (including a per diem attorney) shall, pursuant to CPLR 3408, be fully authorized to dispose of the case; and it is further

ORDERED that the plaintiff shall bring to all future conferences all documents necessary for evaluating the potential settlement, modification, or other workout options which may be appropriate, including but not limited to the payment history, an itemization of the amounts needed to cure the default and satisfy the loan, and the mortgage and note; if the plaintiff is not the owner of the mortgage and note, the plaintiff shall provide the name, address and telephone number of the legal owner of the mortgage and note; and it is further

ORDERED that the plaintiff shall promptly serve, via first class mail, a copy of this Order upon the homeowner-defendants at all known addresses (or upon their attorney if represented by counsel), as well as upon all other appearing parties, and shall provide the affidavit(s) of such service to the Court at the time of the scheduled conference, and annex a copy of this Order and the affidavit(s) of service as exhibits to any future applications submitted to the Court; and it is further

ORDERED that in the event any scheduled court conference is adjourned for any reason, the plaintiff shall promptly send, via first class mail, written notice of the adjourn date to the homeowner-defendants at all known addresses (or upon their attorney if represented by counsel), as well as upon all other appearing parties, and shall provide the affidavit(s) of such service to the Court at the time of the subsequent conference, and annex a copy of this Order and the affidavit(s) of service as exhibits to any future applications submitted to the Court; and it is further

ORDERED that with regard to any future applications submitted to the Court, the moving party(ies) must clearly state, in an initial paragraph of the attorney’s affirmation, whether or not the statutorily required foreclosure conference has been held and, if so, when such conference was conducted; and it is further

ORDERED that with regard to any scheduled court conferences or future applications by the parties, if the Court determines that such conferences have been attended, or such applications have been submitted, without proper regard for the applicable statutory and case law, or without regard for the required proofs delineated herein, the Court may, in its discretion, strike the non-compliant party’s pleadings or deny such applications with prejudice and/or impose sanctions pursuant to 22 NYCRR §130-1, and may deny those costs and attorneys fees attendant with the filing of such future applications.

In this foreclosure action, the plaintiff filed a summons and complaint on February 26, 2008. The complaint essentially alleges that the homeowner-defendants, Derek McCoy and Edyta McCoy, defaulted in payments with regard to a December 8, 2006 mortgage in the principal amount of $288,000.00 for the premises located at 35-34 Gibbs Road, Coram, New York 11727. The original lender, Homecomings Financial, LLC, had the mortgage assigned to the plaintiff by assignment dated February 28, 2008, two days after the commencement of the action. According to the court’s database, a foreclosure settlement conference has not yet been held. The plaintiff’s application seeks a default order of reference and requests amendment of the caption to remove the “Doe” defendants as parties. Plaintiff’s counsel contends that the “present application corrects the specified defects articulated in the [December 4, 2008]Short Form Order.” Notwithstanding counsel’s contention, plaintiff’s current application fails to correct several defects, and presents other grounds which preclude an order of reference in favor of the plaintiff.

By Order dated December 4, 2008, the plaintiff’s prior application for the same relief was denied without prejudice, and with leave to resubmit upon proper papers, to allow the plaintiff to properly show whether or not the subject loan is a “subprime home loan” or a “high-cost home loan” as defined by statute, thereby entitling the defendants to a foreclosure settlement conference pursuant to the then-applicable 2008 NY Laws, Chapter 472. In this regard, the plaintiff’s attorney has submitted a letter in which he claims that it is his “belief that the mortgage being foreclosed is not a sub-prime home loan and is not subject to the [foreclosure conference] requirements.” Counsel also submits an Affirmation of Compliance with CPLR 3408, which states that “[w]e have determined that this loan is not subprime,” and that the defendants “are not entitled to a court conference” (emphasis in original).

Despite counsel’s assertions, the plaintiff’s own affidavit of merit states that “[w]e have determined that this loan is subprime” and that “the defendants are entitled to court conference” (emphasis added). The direct contradiction between counsel’s “belief” and the assessment of one whose affidavit states, as in this case, that she has “first-hand knowledge of the facts and circumstances surrounding this action,” validates this Court’s approach in refusing to accept counsel’s assertions as fact in any given foreclosure action. The mistaken “belief” of an attorney who has no personal knowledge of the facts, yet opines in court documents that a homeowner-defendant is not entitled to a statutorily required court conference, may prejudice the homeowner’s rights while subjecting the attorney to otherwise avoidable court sanctions. Since the plaintiff has failed to adequately show that the homeowner-defendants are not entitled to a foreclosure settlement conference, such conference shall be held on November 17, 2010, 9:30 a.m.

The Court’s December 4, 2008 Order also specifically stated that “[w]ith regard to any future applications … plaintiff’s papers shall include … evidentiary proof of compliance with the requirements of CPLR §3215(f), including but not limited to a proper affidavit of facts by the plaintiff [or by plaintiff’s agent, provided there is proper proof in evidentiary form of such agency relationship], or a complaint verified by the plaintiff and not merely by an attorney or non-party, such as a servicer, with no personal knowledge.”

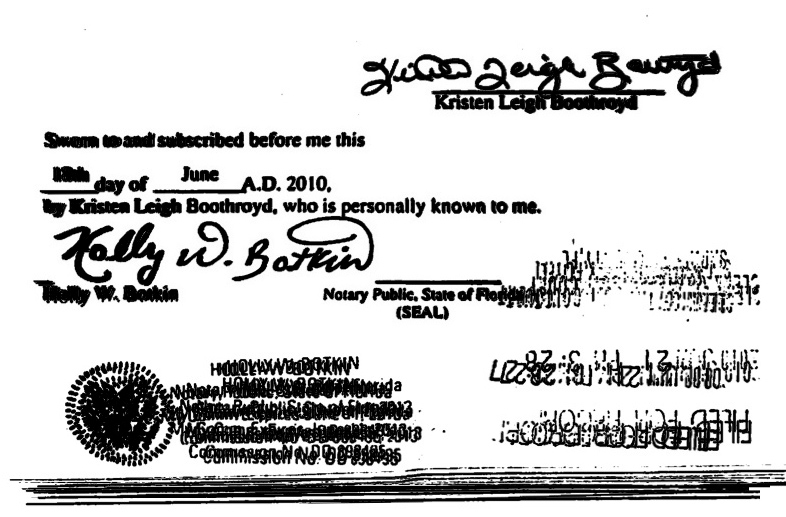

In an apparent effort to satisfy the requirements of CPLR §3215(f), the plaintiff submits an affidavit of merit from “Sherry Hall,” who purports in this particular case to be the Vice President of Homecomings Financial Network, Inc. (“Homecomings”), the purported attorney-in-fact for the plaintiff. The Limited Power of Attorney annexed to the affidavit, however, does not name Homecomings as the attorney-in-fact. Instead, it names Residential Funding Company, LLC. Therefore, the Court cannot conclude that the affidavit was “made by the party” as required by CPLR §3215(f) (emphasis added). Notably, the instructions on the power-of-attorney form also require the form to be recorded and returned not to the plaintiff bank, nor to Homecomings as the purported attorney-in-fact, but rather to “GMAC ResCap.” This raises certain concerns, particularly given the nature of the affidavit of merit submitted in this case, as compared to the affidavit of merit submitted to the Court by the same attorneys in an unrelated foreclosure matter, GMAC Mortgage, LLC v Ingoglia, under Suffolk County Index Number XXXX-XXXX.

In the Ingoglia case (which was recently discontinued), counsel submitted an affidavit of merit from “Sheri D. Hall” in her purported capacity as Vice President of GMAC Mortgage, LLC. That affidavit was notarized by Nikole Shelton on April 14, 2009. Just weeks earlier, on March 25, 2009, Ms. Shelton notarized an affidavit of merit from “Sherry Hall” in this case, in which Ms. Hall purports to be Vice President of Homecomings. It would appear, therefore, that Ms. Hall purports to be the Vice President of two different banks almost simultaneously. Furthermore, although the affidavit in this case appears to have been notarized by Ms. Shelton on March 25, 2009, it appears to have been signed by Ms. Hall five (5) days later, on March 30, 2009, after it was notarized.

The “Hall” affidavit in each case is accompanied by a Certificate of Acknowledgment notarized by “Nikole Shelton” in Montgomery County, Pennsylvania. Both Certificates state that the individual executing the affidavits “personally appeared” before Nikole Shelton. Both state that the affiant was “personally known to [Nikole Shelton] or proved to [Nikole Shelton] on the basis of satisfactory evidence to be the individual whose name is subscribed to the [affidavit].” Notwithstanding these assertions by Ms. Shelton in both cases, the affidavit submitted to the Court in Ingoglia was executed by one who printed and signed her name as “Sheri D. Hall,” while the affidavit submitted in this case was executed by one who printed and signed her name as “Sherry Hall.” Although the Court cannot function as a handwriting expert, the signatures in both affidavits appear virtually identical, despite the difference in the two names.

These facts raise questions concerning the true identity and veracity of the person signing the affidavits of merit, who swears to be the Vice President of two different banks almost simultaneously, as well as the veracity of Nikole Shelton, in notarizing both signatures. Accordingly, “Sherry Hall,” who submitted the affidavit of merit in this case, and “Nikole Shelton,” who purportedly notarized Ms. Hall’s signature in this case and purportedly notarized the signature of “Sheri D. Hall” in the Ingoglia case, shall appear at the November 17, 2010 conference, so the Court may determine whether or not it must conduct an evidentiary hearing on these issues.

Concerning assignment of the subject mortgage, this Court’s December 4, 2008 Order specifically required any resubmitted motion to include “evidentiary proof, including an affidavit from one with personal knowledge, of proper and timely assignments of the subject mortgage, if any, sufficient to establish the plaintiff’s ownership of the subject note and mortgage at the time the action was commenced, and that the assignment is not merely an invalid assignment or an assignment with an ineffectual retroactive date” (emphasis added). Despite this specific instruction, the plaintiff’s affidavit of merit merely states that the plaintiff “is still the holder of record of the … mortgage.” This statement fails to show that the plaintiff was the holder of the note and mortgage when the plaintiff commenced the action. The plaintiff filed the summons and complaint on February 26, 2008; however, the assignment of the mortgage to the plaintiff from the original lender, Homecomings Financial, LLC, is dated February 28, 2008, two days after the commencement of the action.

Only where the plaintiff is the assignee of the mortgage and the underlying note at the time the foreclosure action was commenced does the plaintiff have standing to maintain the action (U.S. Bank, N.A. v Collymore, 68 AD3d 752, 890 NYS2d 578 [2d Dept 2009]; Federal Natl. Mtge. Assn. v Youkelsone, 303 AD2d 546, 755 NYS2d 730 [2d Dept 2003]; Wells Fargo Bank, N.A. v Marchione, 69 AD3d 204, 887 NYS2d 615 [2d Dept 2009]; First Trust Natl. Assn. v Meisels, 234 AD2d 414, 651 NYS2d 121 [2d Dept 1996]). An assignment executed after the commencement of an action, which states that it is effective as of a date preceding the commencement date, is valid where the defaulting defendant appears but fails to interpose an answer or file a timely pre-answer motion that asserts the defense of standing, thereby waiving such defense pursuant to CPLR 3211[e] (see, HSBC Bank, USA v Dammond, 59 AD3d 679, 875 NYS2d 490 1445 [2d Dept 2009]). It remains settled, however, that foreclosure of a mortgage may not be brought by one who has no title to it and absent transfer of the debt, the assignment of the mortgage is a nullity (U.S. Bank, N.A. v Collymore, 68 AD3d 752, 890 NYS2d 578 [2d Dept 2009]; Kluge v Fugazy, 145 AD2d 537, 536 NYS2d 92 [2d Dept 1988]).

Although the February 28, 2008 assignment states it is “effective January 19, 2008,” such attempt at retroactivity is ineffectual. If an assignment is in writing, the execution date is generally controlling and a written assignment claiming an earlier effective date is deficient, unless it is accompanied by proof that the physical delivery of the note and mortgage was, in fact, previously effectuated (see, Bankers Trust Co. v Hoovis, 263 AD2d 937, 938, 694 NYS2d 245 [1999]). A retroactive assignment cannot be used to confer standing upon the assignee in a foreclosure action commenced prior to the execution of the assignment (Countrywide Home Loans, Inc. v Gress, 68 AD3d 709, 888 NYS2d 914 [2d Dept 2009]; Wells Fargo Bank, N.A. v Marchione, 69 AD3d 204, 887 NYS2d 615 [2d Dept 2009]). Plaintiff’s failure to submit proper proof, including an affidavit from one with personal knowledge, that the plaintiff was the holder of the note and mortgage at the time the action was commenced, requires denial of the plaintiff’s application for an order of reference.

In its prior Order, the Court also gave specific directives concerning proof of compliance with RPAPL §1303 and § 1320 for any resubmitted motions. In this regard, the prior Order required “evidentiary proof, including an attorney’s affirmation, of compliance with the form, type size, type face, paper color and content requirements of RPAPL §1303 regarding foreclosure notices, as well as an affidavit of proper service of such notice,” as well as “evidentiary proof, including an attorney affirmation, of compliance with the form, content, type size, and type face requirements of RPAPL §1320 regarding special summonses in residential foreclosure actions, and proof of proper service of said special summons” (emphasis supplied). Despite these very specific directives, the attorney’s affirmation in support of this resubmitted motion fails to address those sections. While the affidavit of service does state that the summons and complaint were served with a Section 1303 notice on colored paper and a Section 1320 notice, such information, by itself, is not proper proof that those notices were compliant with the specific form, content, type size, and type face requirements set forth in those statutes.

Lastly, the Court notes that although service of process was made upon defendant Derek McCoy by substitute service pursuant to CPLR 308(2), the additional mailing required for such service was never completed. Instead, the process server sent the additional mailing to defendant Edyte McCoy who is alleged to have received a copy of the summons and complaint by personal service pursuant to CPLR 308(1). Such personal service does not require an additional mailing to complete service. Based on the foregoing, the plaintiff has established neither completion of service upon the defendant, Derek McCoy, nor jurisdiction of this Court over that defendant.

Based upon the foregoing, the plaintiff’s motion is denied.

This constitutes the Decision and Order of the Court.

Please send me any Corporate Resolutions or Signing Agreements you may have. These were provided mainly to Vendors/ Foreclosure Mills. Not easy to get but also not impossible.

Be it Resolved that the attached list of candidates are employees of (Insert Name of MERS Member), a Member of Mortgage Electronic Registration Systems, Inc. (MERS), and are hereby appointed as assistant secretaries and vice presidents of MERS, and, as such, are authorized to:

(1) Release the lien of any mortgage loan registered on the MERS® System that is shown to be registered to the Member;

(2) Assign the lien of any mortgage loan naming MERS as the mortgagee when the Member is also the current promissory note-holder, or if the mortgage loan is registered on the MERS® System, is shown to be registered to the Member;

(3) Execute any and all documents necessary to foreclose upon the property securing any mortgage loan registered on the MERS® System that is shown to be registered to the Member, including but not limited to (a) substitution of trustee on Deeds of Trust, (b) Trustee’s Deeds upon sale on behalf of MERS, (c) Affidavits of Non-military Status, (d) Affidavits of Judgment, (e) Affidavits of Debt, (f) quitclaim deeds, (g) Affidavits

regarding lost promissory notes, and (h) endorsements of promissory notes to VA or HUD on behalf of MERS as a required part of the claims process;

(4) Take any and all actions and execute all documents necessary to protect the interest of the Member, the beneficial owner of such mortgage loan, or MERS in any bankruptcy proceeding regarding a loan registered on the MERS® System that is shown to be registered to the Member, including but not limited to: (a) executing Proofs of Claim and Affidavits of Movant under 11 U.S.C. Sec. 501-502, Bankruptcy Rule 3001-3003, and applicable local bankruptcy rules, (b) entering a Notice of Appearance, (c) vote for a trustee of the estate of the debtor, (d) vote for a committee of creditors, (e) attend the meeting of creditors of the debtor, or any adjournment thereof, and vote on behalf of the Member, the beneficial owner of such mortgage loan, or MERS, on any question that may be lawfully submitted before creditors in such a meeting, (f) complete, execute, and return a ballot accepting or rejecting a plan, and (g) execute reaffirmation agreements;

(5) Take any and all actions and execute all documents necessary to refinance, subordinate, amend or modify any mortgage loan registered on the MERS® System that is shown to be registered to the Member.

(6) Endorse checks made payable to Mortgage Electronic Registration Systems, Inc. to the Member that are received by the Member for payment on any mortgage loan registered on the MERS® System that is shown to be registered to the Member;

(7) Take any such actions and execute such documents as may be necessary to fulfill the Member’s servicing obligations to the beneficial owner of such mortgage loan (including mortgage loans that are removed from the MERS® System as a result of the transfer thereof to a non-member of MERS).

I, William C. Hultman, being the Corporate Secretary of Mortgage Electronic Registration Systems, Inc., hereby certify that the foregoing is a true copy of a Resolution duly adopted by the Board of Directors of said corporation effective as of the day of , which is in full force and effect on this date and does not conflict with the Certificate of Incorporation or By-Laws of said corporation.

____________________________________

William C. Hultman, Secretary

Excellent resource on MERS below from the law department:

Erika Herrera CA Notary Public No. 1290845 Revocation Cert 9-29-10,

If Erika Herrera Notarized your foreclosure documents the foreclosure is illegal!!

Employed by Washington Mutual and acting as a Notary was not a legal Notary in California where she worked and notarized thousands of foreclosure documents. Please see attached and inform all of your members nationwide!

She has notarized documents including affidavits and assignments.

By The Palm Beach Post

Updated: 7:45 p.m. Thursday, Sept. 23, 2010

Posted: 7:33 p.m. Thursday, Sept. 23, 2010

Last month, Palm Beach County Senior Judge Roger Colton opened his afternoon foreclosure session by telling homeowners that he’d heard all their stories before, and he would give them a maximum of five months before letting lenders take their homes.

“I know all about the Chinese drywall problems. I know all about sickness,” Judge Colton said. “I know all about divorce. I know all about anything else as to why we find ourselves in this position today.”

In the first case, Judge Colton signed a final summary judgment giving Everhome Mortgage Co. the right to foreclose on a Lake Worth couple’s home despite their attorney’s objections that Everhome had failed to prove that it owns the note. Foreclosure defense lawyers cite the case as an egregious example of Florida’s so-called “rocket docket,” the process of expediting foreclosure cases through the courts by siding with lenders.

That was not the intent of state legislators this year when they appropriated $9.6 million to reduce the foreclosure backlog. Though the state has set a goal of reducing the more than 500,000 cases by 62 percent within a year, that goal should be met by handling each case based on its merit and not by watching the clock. That’s particularly important given the fraud perpetrated by lenders – many of which knowingly issued loans to buyers who couldn’t afford them – and their attorneys.

Tampa-based Florida Default Law Group has been withdrawing legal affidavits in its GMAC Mortgage foreclosure cases, acknowledging that information it gave to courts may have been inaccurate. The affidavits supposedly attest to the validity of documents submitted to verify that a lender has the right to foreclose. Florida law requires that lenders prove ownership of the note underlying the mortgage.

In the case before Judge Colton, attorney Loretta Bangor questioned the validity of affidavits submitted by Everhome’s attorney, a lawyer with Shapiro & Fishman, one of three firms under investigation by the Florida attorney general for “unfair and deceptive actions” in foreclosure cases. Judge Colton, one of two retired judges hired to handle foreclosures under the new state program, did not ask to see the documents. Nor did he question Shapiro & Fishman about the validity of the documents.

In 2006 MERS released a mortgage belonging to the Velez’s. MERS Vice President name is Merhl Gibson and the notary is Jane Eyler. Both from Maryland. It appears that the same individual signed the entire document. See exhibit below.

Now these same individuals are signing this document below as Vice President and Notary for CitiMortgage. But take a close look and compare the signatures to the release above.Both of these are about a few weeks apart. Merhl’s stamp is from New York.

“On 8/30, I had a Summary Judgment Foreclosure hearing on Palm Beach County’s “Rocket Docket”. The judge spoke for 14 minutes to the crowd, of mostly pro se defendants, about how they should just agree to the summary judgment and the plaintiffs, (whose attorneys (Shapiro & Fishman had a dedicated courtroom and to whom he referred to as “my attorneys”) would be gracious (Ha!) enough to allow them to stay in their homes for 120 days if needed (even though the statute says he only has to give them 30). When it came to hearing arguments which were fully briefed and provided to the court (pursuant to the instructions of the Divisions head judge) he only allowed 30-60 seconds for argument, failed to read any of the papers, failed to review the plaintiff’s foreclosure package,flatly ignored the Affidavit filed in Opposition, ignored my plea for a trial, signed the judgment and dismissed me. I never was permitted to even read the proposed judgment or to examine the “newly discovered” allonge which Shapiro’s counsel said I had no right to see. Thank God I had a court reporter!”

Well it just happens to be that Lori is an Attorney and got a transcript of what went down…

Financial giants have figured out yet another way to profit from fraud. After devastating communities across the country with shady subprime loans, the mortgage industry has launched a new assault on America’s neighborhoods. Big banks are now outsourcing their foreclosure processing to shady law firms with a history of breaking the law for a quick buck. These foreclosure scammers forge documents, backdate signatures, slap families with thousands of dollars in illegal fees and even foreclosure on borrowers who haven’t missed a payment.

Andy Kroll lays out the insanity in a terrific piece for Mother Jones. “Foreclosure mills,” as they are known, have been around for years, but they’ve become a much bigger problem as the mortgage crisis has deepened. Fannie Mae and Freddie Mac spurred the creation of these social beasts decades ago to help them process large volumes of foreclosures quickly and cheaply. Pretty soon big banks wanted in on the action, and bailout barons at Wells Fargo, Citigroup and Bank of America starting sending foreclosures to these scummy law firms by the thousands.

Banks opt to outsource dirty work like this for a reason. It takes weeks to process the legal work necessary to kick somebody out of their home, since cops and judges don’t want to give borrowers the boot without proof. If you can cut down that processing time, you can save a lot of money on legal bills. Foreclosure mills cut costs for banks by cutting corners—when they can’t compile the documentation needed to push families out of their homes right now, they simply fabricate the documents. Still worse, these guys illegally withhold documentation from borrowers seeking to negotiate loan modifications with their banks—effectively forcing borrowers out of their homes instead of allowing them to cut a deal with the bank. When borrowers actually do straighten things out with foreclosure mills, the scumbags slap them with huge illegal fees. Kroll details a foreclosure mill that erroneously tried to evict a Florida couple who had been paying their mortgage on time. When it became clear that the couple could not be kicked out of their home, the foreclosure mill tried to charge them $18,500 in fees for mistakes committed by the foreclosure mill and the bank. The foreclosure mill even invented two new people who it said lived in the home in order to demand four sets of legal processing fees instead of two.

If nobody holds you accountable, then lying, cheating and stealing are very profitable business models. That’s one reason why banks love sending this kind of work to foreclosure mills. While the foreclosure mills and their lawyers have been bombarded with lawsuits for their trickery, the banks are not directly involved in the funny business. So Citi, BofA, Fannie and Freddie get to cut their costs with shady practices, but they don’t have to shoulder the legal liability for them, even though they must surely know what goes on (if they don’t know, they’re being astonishingly negligent, and should be held responsible).

The foreclosure mill scandal is very similar to a game the banks played in the craziest days of the housing bubble. A few years back, banks outsourced much of the work that goes into issuing mortgages to third-party mortgage brokers. Banks knew that many of these brokers were up to no good, and routinely trained brokers how to steer borrowers into unaffordable subprime loans. Banks also lobbied regulators aggressively for the right to look the other way when brokers abused borrowers or committed fraud. For a few years, banks made big bucks as mortgage brokers turned out fraudulent loans by the truckload. When those loans started defaulting, the banks pleaded innocence and blamed the brokers for the social and economic fallout.

AT NO TIME IN HISTORY was crime more rampant than it is today. White-collar crime accounts for more than $140 billion in losses annually. Nearly $20 billion worth of check fraud occurs annually. More than $2 million of worthless checks are passed daily. Telemarketing accounts for $48 billion in fraud, while according to the FBI, Internet fraud as of 2009 had topped $264 million in online losses. A crime wave of this proportion has put the services of competent investigators and certified forensic-document examiners in high demand.

This article is intended to educate and assist attorneys or investigators when they are speaking with attorneys, judges, or clients about cases that involve questioned documents. There are numerous types of cases where a document or handwriting evidence may be involved as a result of being found either at the crime scene or at the center of a civil suit.

A competent investigator is cognizant of all the clues at a crime scene. Items such as credit-card receipts, legal papers, canceled checks, personal notes, leases, and other types of documents and writing may hold the clues to the motive. The observant investigator will call attention to these documents. An investigator who does not think along those lines may miss the subtle clues that could be found on even the smallest scrap of paper, on a blank writing pad (that might reveal “invisible” indented writing), or among the personal belongings of a victim.

Crimes involving fraud, larceny, forged wills, death threats, identity theft, ransom notes, poison-pen letters, “other-hand” disguised writing, traced signatures, assisted deathbed signatures, altered medical records, fingerprint examination, ink and paper analysis, watermarks, contrived faxes, “cut-and-pasted” signatures on legal documents, anachronisms (chronological errors, such as paper or ink that did not exist simultaneously), disputed pre- and post-nuptial agreements, and auto-pen signatures are examples of the types of cases that are filed in our courts every day. An investigator should be aware of the fact that any documents or written material found at the crime scene may hold clues to solving the case, whether it is written on paper, walls, a car door, or a mirror. Questioned documents or writing can be typed, written in blood, lipstick, ink, pencil, or body fluids.

Most documents are written with non-violent, white-collar criminal intent. Others are written with darker purposes in mind: murder, stalking, kidnapping, and suicide. In questioned-document investigations—as in any investigation—it is the duty of the document examiner to remove the shadow of doubt. The examiner, if possible, will determine—without prejudice—if the document is authentic or forged, original or altered. The document examiner is an advocate of the courts. Examiners do not have clients; they represent the justice system. As a result, the examiner cannot become emotionally involved or empathetic. Upon initial contact, the examiner must disclose a non-fiduciary relationship to the person who retains the examiner’s services.

A well-trained document examiner knows to examine all the physical features of a questioned document, not just the questioned signature. There are dozens of components to consider when examining a signature or a document. Characteristics to consider include the writing medium used and the surface it is written upon, the age of the paper or ink, and watermarks.

There are deletions, alterations, inclusions, and other aspects that must be considered, as well. The evaluation of letter formations, pen strokes, pen pressure, spacing, letter height, relation to the baseline, and slant are all part of the evaluation process.

When a document is typewritten, there are other problems to consider. Was a page added after the fact? Is the page a copy? Did someone possibly apply “white out” on the original, type over it, and then make a copy so that it looks like an original? Was another typewriter used to make the forgery or the added page? And what about a computer-generated document? Are the pages all from the same ream of paper? With technology such as infrared and ultraviolet light sources, these questions can be answered.

On a daily basis, document examiners are faced with a multitude of questioned-document problems. The most common cases, for example, involve forged checks, forged wills, graffiti, credit-card fraud, leases, deeds, contracts to purchase items—including homes, cars, and businesses—mortgage fraud, disguised writing, and poison-pen letters (hate letters). With the improved technology of printers and copiers, forging and counterfeiting is rampant through the use of “cut and paste” and “lifting signatures”.

It is well known that the field of digital science is constantly evolving. As new technology becomes available, the document examiner must stay on top of the latest state-of-the-art and work to anticipate the ways criminals may use new technology to their advantage. The certified forensic document examiner must utilize all the latest techniques and technology that science has to offer when examining questioned documents. When investigating digital crimes—crimes such as forged passports, driver’s licenses, computer-generated documents, and digital images inserted into other items—document examiners are referred to as digital-crime investigators.

Comparative Ink Analysis

The newest technology today is found in comparative ink analysis equipment. One very useful forensic tool in pen-formula differentiation is ink analysis that involves the determination of chemicals specific to certain types of compounds. One method used to identify a certain kind of ballpoint-pen ink is called thin-layer chromatography. The process involves using an ultraviolet-visible photodiode array detector that allows for the dye components to be rapidly separated.

A standard is a known authentic sample from which comparisons are made. The United States Secret Service and the Internal Revenue Service (IRS) jointly maintain the International Ink Library. This collection includes more than 9,500 inks, dating from the 1920s. New inks are chemically tested and added to this database on a regular basis. This reference serves as a great resource for the detection of fraudulent signatures and documents.

In the comparison of inks, chemical analysis can be useful in a number of cases, such as medical charts, tax evasion, insurance fraud, altered checks, counterfeiting, and other types of forgeries or frauds. A 2004 article from the Associated Press referenced ink-comparison evidence as one piece of evidence that assisted in the high-profile conviction of Martha Stewart. Examination of the ink on a document showed that an entry was made at a different time, possibly as an attempt to cover up insider-trading violations.

Aging Papers and Inks

The age of paper and ink can provide important clues when attempting to verify and authenticate a document. A key example was the Hitler Diaries case from the 1980s—one that involved purported diaries written by Adolf Hitler. The document examiner in the case unknowingly compared forged writing to the writing of the diaries. Taking the authentication and investigation one step further, the diaries were sent to a laboratory where the paper and ink was analyzed. It was proven conclusively that the document could not have been written by Hitler, since there were chemical compounds discovered in the paper of the book’s cover that were not available when Hitler was alive. The age of paper can be determined according to the additives and chemicals or by watermarks. The Hitler Diaries, as well as many other questioned historical papers, have been debunked, while others have been authenticated.

Two new methods of determining the relative age of ballpoint inks has recently come to the forefront in forensic-document examination. Studies have shown that different inks have different drying times. The new method for analyzing the drying time of ink is done by chemical analysis. Unfortunately, this is a destructive process.

These new developments are extremely important when examining ledger or medical-record entries. It has been established that the longer ink has been on a sheet of paper, the slower it will dissolve in the various solvents used to analyze them. It is now possible to identify the age of ink to within a six-month period. This new process of dating the age of inks has had dramatic impact on the examination and detection of backdated documents. Many malpractice cases have been won due to the analysis of ink on questioned medical records.

Infrared Comparisons

Infrared-imaging equipment and infra-red photography have given the document examiner an exciting new world of technology for investigating cases. Although this is not a new concept, the technology has been refined and taken to mind-boggling new heights.

The mechanics behind infrared are quite simple. The human eye perceives the reflected portion of the light spectrum. But there is much more of the spectrum that the human eye cannot see. For instance, when we see a rainbow, we are not seeing all the colors that exist. We see only red, orange, yellow, green, blue, indigo and violet. The colors on each side of the rainbow that we cannot see with the naked eye are the ultraviolet (UV) and infrared (IR) areas. The instruments we need to convert UV and IR wavelengths of the light spectrum into visible images for the human eye are called video spectral comparators and forensic imaging spectrometers. This equipment is used for non-destructive analysis of questioned documents in the presence of seemingly equal but physically different features of writing. With IR and UV, we can see “through” writing that has been blacked out or obscured by “white out”, as well as scribbled-out writing.

With split-screen and overlay software, direct visual comparison can be made of several individual images. Erased elements or chemically altered characters can be easily detected with IR and UV technology. The exceptional sensitivity and broad spectral range can detect even the slightest differences in similar inks, not seen by the unaided eye. This equipment is at the highest level of authentication technology available today.

Obliterated, faded, or altered writing can also be detected with IR and UV analysis. In a recent case handled by the IRS, the IRS claimed the defendant could not prove an expense he had written off for office equipment because the receipt had faded. The paper was old and the writing was “invisible”. Under an IR filter, the “blank” receipt luminesced, showing writing that was outside the wavelength of visible light to the naked eye.

Electrostatic Detection Apparatus

Another valuable piece of equipment to the document examiner is an electrostatic detection apparatus (ESDA). With an ESDA and specialized infra-red side-lighting photographic techniques, the characteristic indentations found in writing may prove that the writing was traced. In addition, when the top page of a pad that has been written on is removed, the “blank” writing underneath can be processed with an ESDA to show the writing by the indentations on the pages below. Research performed by the John Jay College of Criminal Justice in New York City indicates that an ESDA can recover indented impressions from documents that were written up to 60 years earlier.

The technology behind the ESDA is fairly simple: To develop the indentations on paper, the indented paper is placed in a high-humidity device and transferred onto a bronze vacuum plate. The page is then carefully covered with a Mylar (transparent, non-conducting) film. The page is then electrically charged so that toner will adhere to the impressions when applied to the Mylar covering. The final step is to pour the toner on the Mylar. This process develops the page containing the various indentations.

An example of the use of an ESDA in a recent case involved a bust on a PCP drug lab. Although there was no paper evidence at the scene of the raid, the telephone book at the scene was analyzed and, in the end, it held the incriminating evidence—only visible by use of the ESDA. An astute investigator noticed a telephone book on the counter where the drugs were being processed. On the cover of the phone book were slight indentations that appeared to be writing. The indentations were restored by ESDA and the writing was compared to that of the known chief chemist of the PCP lab. The writing the ESDA retrieved was the chemical formulas, written by the chief chemist. Busted!

As an investigator, you need to think outside the parameters of visible evidence. Evidence to solve your case may be right in front of you and may easily go unnoticed. In this case of the PCP lab, the real incriminating evidence was truly invisible. If not for the trained eye of the investigator, the case may have been dismissed for lack of solid evidence that could link the suspect with the actual manufacturer of the drugs.

As an advocate of the court, the document examiner is relied upon to dispel any doubts about a questioned document. Sometimes, the examiner simply will not be able to render an opinion on certain documents. In those instances, the document examiner’s letter of opinion will state an explicit explanation.

From murder scenes where notes are left behind, to kidnappings, to white-collar crimes such as forged checks, document examiners, investigators, and the technology they utilize prove to be a formidable team.

Questioned documents are a global issue. As investigators, you must be cognizant of the technologically advanced level of the criminals we face today. We must use all of the intelligence, the technology, and the resources available to educate ourselves on the topic of continually evolving criminal minds.

About the Author

E’lyn Bryan is a court-qualified and certified document examiner through the National Questioned Document Association. She offers presentations and training sessions for businesses and law-enforcement agencies on questioned-document examination. She is the current president of the South Florida Investigators Association and a member of the World Association of Detectives. She can be reached by phone at: 561-361-0007or by e-mail at: bocaforensic@aol.com

Litigation Support

Forensic Document Examiners Inc.

div. of Forensic Bureau of Investigations Inc. www.FloridaDocumentExaminer.com President of South Florida Investigators Association

Instructor of Forensic Document Examination to Law Enforcement

National Association of Document Examiners

World Association of Detectives

Gold Coast Forensics Association

Florida Association of Private Investigators

Member of South County Bar Association

Forensic Expert Witness Association 561.361.0007

Cheryl Samons is an employee of David Stern Firm in Plantation Florida. The mere fact that she is signing documents representing the grantor when the grantee is the client of her employer’s law firm leads to questions and concerns, but:

How can an unsigned legal document get notarized and witnessed? (St. Lucie County, FL)

Bank of America took over Countrywide on June 3, 2009. How can Countrywide assign a mortgage on April 28, 2010? (Palm Beach County, FL)

In every foreclosure case, there are at least one, possibly two, points at which a legal notice must be published. In every foreclosure case, the notice of sale must be published in a local newspaper twice before the sale (Fla. Stat. § 45.031 (2)) and in some cases, if the owner of the property cannot be found, the plaintiff can serve by publication in the newspaper instead of having a process server deliver it personally.

But no matter what, any time a legal notice is published in a newspaper, some representative of the newspaper must provide a “Proof of Publication” affidavit, swearing that the ad was published on the dates indicated, and that the newspaper meets certain specified legal requirements.

In the Tampa Bay area, there is one newspaper that handles the legal notices for almost every foreclosure case: the Gulf Coast Business Review. And just last night, I had the opportunity to take a look at several of the “proof of publication” affidavits produced by that particular newspaper. You’ll be shocked at what I found.

Two things looked suspicious about the signatures on the affidavits. First, they were extremely uniform – almost identical. Second, the notary’s signature blocked out the signature line. Underneath the signature, instead of a line, there was just white space. These are classic signs of digital manipulation.

So I grabbed six different affidavits in a series of related foreclosure sales in Sarasota County. Once I had the digital images, I was able to copy the signature block by itself from each one, and digitally overlay them to see just how alike they were. One by one, the signatures shows themselves to be…

Every letter on every affidavit, whether typed or signed, fell in exactly the same place on each sheet of paper – except the notary stamp. What does this mean? The affidavits aren’t affidavits at all – they’re computer-generated images that some foolish notary has been stamping her seal on. Knowing the volume of legal ads run by this paper, they’re probably generating hundreds of them for every issue.

And here’s the problem:

A notary public may not sign notarial certificates using a facsimile signature stamp unless the notary public has a physical disability that limits or prohibits his or her ability to make a written signature and unless the notary public has first submitted written notice to the Department of State with an exemplar of the facsimile signature stamp….

A notary public may not notarize a signature on a document if the person whose signature is being notarized is not in the presence of the notary public at the time the signature is notarized. Any notary public who violates this subsection is guilty of a civil infraction, punishable by penalty not exceeding $5,000, and such violation constitutes malfeasance and misfeasance in the conduct of official duties. It is no defense to the civil infraction specified in this subsection that the notary public acted without intent to defraud. A notary public who violates this subsection with the intent to defraud is guilty of violating s. 117.105.

Fla. Stat. § 117.107 (2) & (9) Mass-producing affidavit signatures like this, by computer, is flatly illegal. And if that’s what is really happening over at the Gulf Coast Business Review, this business is about to take a very interesting turn – for the worse. And for homeowners, it means one more chink in the armor, one more place to attack, one argument of last resort, before the sheriff comes to remove you from your home.

This matter is currently before the Court on the motion for partial summary judgment filed by the plaintiff-trustee, Lauren Helbling, and the joint brief in opposition of Carrington Mortgage and Deutsche Bank National Trust Company (“Deutsche Bank”). The main issue is whether the trustee is entitled to avoid a mortgage because the notary’s certificate of acknowledgment failed to recite the names of the parties whose signatures were acknowledged. The Court must also decide whether the filing of one or both foreclosure actions imparted the trustee with constructive notice resulting in inability to act as a bona fide purchaser for value. If the trustee is charged with constructive notice, then the Court must consider whether the second foreclosure action was an avoidable preference. For the reasons that follow, the Court holds that the Mortgage was not executed in accordance with Ohio’s statutory requirements but that the trustee is charged with constructive notice of the interest of Deutsche Bank as a result of the filing of the second foreclosure action. However, the filing of the second foreclosure acted to perfect the defective mortgage as against third persons, and it is a preferential transfer. As such, the Mortgage can be avoided by the trustee as a preference. Accordingly, the trustee’s motion for partial summary judgment is granted.

FACTS AND PROCEDURAL BACKGROUND

On December 30, 2009, the plaintiff-trustee and defendants Deutsche Bank and Carrington submitted the following stipulations:

1. Jurisdiction of this Court is proper and as set forth in Paragraph 1 of the complaint.

2. This is a core proceeding as set forth in Paragraph 2 of the Complaint.

3. Plaintiff is the duly appointed, qualified and acting Trustee of the estate of the debtor.

4. A legal description for property known as 4155 West 114th Street, Cleveland, OH is shown as Exhibit A to the Complaint (“Property”).

5. The petition in this case was filed on May 31, 2009.

6. The Debtor’s interest in the Property is property of the bankruptcy estate pursuant to 11 U.S.C. § 541.

7. The Debtor is the owner, in fee simple of the Property, by virtue of a General Warranty Deed filed in Instrument No. 200302030753 of the records of Cuyahoga County, Ohio on February 3, 2003.

8. Deutsche Bank National Trust Company (“Deutsche”) is the holder of a mortgage on the Property (the “Mortgage”), which Mortgage is at issue in this proceeding.

9. The Mortgage was filed on May 5, 2004, as Instrument No. 200405050625 in the records of Cuyahoga County, Ohio.

10. A true and exact copy of the Mortgage is attached to the Complaint as Exhibit B.

11. The original mortgagee under the Mortgage is New Century Mortgage Corporation. The Mortgage was assigned to Deutsche of record by assignment filed December 16, 2008 as Instrument No. 200812160236, Cuyahoga County Records.

12. The acknowledgment provision of the Mortgage on page 15 reads as follows:

This instrument was acknowledged before me this 30th day of April 2004, by

Stamp JERRY RUSSO

Notary Public

In and for the State of Ohio

My Commission Expires

May 19, 2008

/s/ Jerry Russo

Notary Public

13. Debtor’s initials appear at the bottom of Mortgage pages 1 through 13, and page 15 and page 17.

14. A foreclosure action was filed as to thea subject property in Case No. 663230 of the Cuyahoga County, Ohio Common Pleas Court on June 25, 2008 by Deutsche. The property was described in the foreclosure Complaint. The debtor answered in that case on September 25, 2008. The case was dismissed without prejudice on October 30, 2008.

15. A foreclosure action was filed as to the subject property in Case No. 694194 of the Cuyahoga County, Ohio Common Pleas Court on May 28, 2009 by Aeon Financial. The property was described in the foreclosure Complaint. The debtor filed a Notice of Suggestion of Stay on June 15, 2009. The Court entered an Order staying the case on June 19, 2009. The case was dismissed without prejudice on August 5, 2009.

On August 28, 2009, the trustee of the Chapter 7 estate initiated this adversary proceeding seeking to avoid the Mortgage and to determine the respective interests of various parties in the real property. The complaint named as defendants the debtor; Carrington Mortgage; CitiFinancial Inc.; Aeon Financial, LLC; Beneficial Ohio, Inc.; TFC National Bank; Deutsche Bank National Trust Company; and the Cuyahoga County Treasurer. The treasurer, Citifinancial, David Cleary, Aeon Financial, TFC National Bank, and Carrington/Deutsche Bank filed answers to the complaint. Aeon Financial and TFC National Bank disclaimed any interest, and all parties stipulated that the Cuyahoga County Treasurer has a first lien for taxes and assessments. Default was entered against Beneficial Ohio on March 24, 2010. On January 13, 2010, the trustee filed a motion for partial summary judgment seeking to avoid the Mortgage held by Deutsche Bank. On February 3, 2010, Deutsche Bank filed a brief in response. Briefing on the trustee’s partial motion for summary judgment is complete, and the Court is ready to rule.

JURISDICTION

Determinations of the validity, extent, or priority of liens are core proceedings under 28 U.S.C. section 157(b)(2)(K). The Court has jurisdiction over core proceedings under 28 U.S.C. sections 1334 and 157(a) and Local General Order No. 84, entered on July 16, 1984, by the United States District Court for the Northern District of Ohio.

SUMMARY JUDGMENT STANDARD

Federal Rule of Civil Procedure 56(c), as made applicable to bankruptcy proceedings by Bankruptcy Rule 7056, provides that a court shall render summary judgment, if the pleadings, depositions, answers to interrogatories, and admissions on file, together with affidavits, if any, show that there is no genuine issue as to any material fact and that the moving party is entitled to judgment as a matter of law.

The moving party bears the burden of showing that “there is no genuine issue as to any material fact and that [the moving party] is entitled to judgment as a matter of law.” Jones v. Union County, 296 F.3d 417, 423 (6th Cir. 2002). See generally Celotex Corp. v. Catrett, 477 U.S. 317, 322 (1986). Once the moving party meets that burden, the nonmoving party “must identify specific facts supported by affidavits, or by depositions, answers to interrogatories, and admissions on file that show there is a genuine issue for trial.” Hall v. Tollett, 128 F.3d 418, 422 (6th Cir. 1997). See, e.g., Anderson v. Liberty Lobby, Inc., 477 U.S. 242, 252 (1986) (“The mere existence of a scintilla of evidence in support of the plaintiff’s position will be insufficient; there must be evidence on which the jury could reasonably find for the plaintiff.”). The Court shall view all evidence in a light most favorable to the nonmoving party when determining the existence or nonexistence of a material fact. See Tenn. Dep’t of Mental Health & Mental Retardation v. Paul B., 88 F.3d 1466, 1472 (6th Cir. 1996).

DISCUSSION

Under the “strong arm” clause of the Bankruptcy Code, the bankruptcy trustee has the power to avoid transfers that would be avoidable by certain hypothetical parties. See 11 U.S.C. § 544(a). Section 544 provides in pertinent part:

(a) The trustee shall have, as of the commencement of the case, and without regard to any knowledge of the trustee or of any creditor, the rights and powers of, or may avoid any transfer of property of the debtor or any obligation incurred by the debtor that is voidable by —

. . . .

(3) a bona fide purchaser of real property, other than fixtures, from the debtor, against whom applicable law permits such transfer to be perfected, that obtains the status of a bona fide purchaser and has perfected such transfer at the time of the commencement of the case, whether or not such a purchaser exists.

11 U.S.C. § 544. Any transfer under section 544 is preserved for the benefit of the estate. See 11 U.S.C. § 551.

Page 10 of the Mortgage provides that “[t]his Security Instrument shall be governed by federal law and the law of the jurisdiction in which the Property is located.” Accordingly, because the real property in question is located in Ohio, the Court will apply Ohio law to determine whether the trustee may avoid the Mortgage using the “strong arm” clause. See Simon v. Chase Manhattan Bank (In re Zaptocky), 250 F.3d 1020, 1024 (6th Cir. 2001) (applicable state law governs determination whether hypothetical bona fide purchaser can avoid mortgage).

Under Ohio law, a bona fide purchaser is a purchaser who ” `takes in good faith, for value, and without actual or constructive knowledge of any defect.’ ” Stubbins v. Am. Gen. Fin. Servs. (In re Easter), 367 B.R. 608, 612 (Bankr. S.D. Ohio 2007) (quoting Terlecky v. Beneficial Ohio, Inc. (In re Key), 292 B.R. 879, 883 (Bankr. S.D. Ohio 2003)); see also Shaker Corlett Land Co. v. Cleveland, 139 Ohio St. 536 (1942). The Bankruptcy Code expressly provides that a bankruptcy trustee is a bona fide purchaser regardless of actual knowledge. See In re Zaptocky, 250 F.3d at 1027 (“actual knowledge does not undermine [trustee’s] right to avoid a prior defectively executed mortgage”). Because actual knowledge does not affect the trustee’s strong-arm power, contrary to the assertions made by the defendants, the Court need only determine whether the trustee had constructive knowledge of the prior interest held by Deutsche Bank.

Ohio law provides that “an improperly executed mortgage does not put a subsequent bona fide purchaser on constructive notice.” In re Zaptocky, 250 F.3d at 1028. Ohio courts have refused to allow a recorded mortgage to give constructive notice when the mortgage has been executed in violation of a statute. See In re Nowak, 104 Ohio St. 3d 466, 469 (2004) (listing cases). The first question, then, is whether the Mortgage was executed in compliance with, or substantially conforms to applicable statutory law.