“Years before they can get clear title and actually sell em”

“You guys in the MEDIA have a real tough time…your looking for events, your trying to cover the news minute by minute…”

“THIS IS CANCER”

“There are a lot of investors out there who don’t know what they own… they may own unsecured loans….. trustees that were supposed to do things under state law (and didn’t)… even Fannie and Freddie have issues with this.”

“This is not minutia…this is the Letter of the Law”

“Most securities issues in the United States are governed by New York law”

“Dealer has to deliver to the trustee the notes, that evidence the obligation”

“Trustees have the least duties”

“You have to indemnify them”

Christopher Whalen, managing director of Institutional Risk Analytics, talks with Bloomberg’s Mark Crumpton about the impact of U.S. mortgage foreclosures on banks and the housing market and the outlook for the economy.

Whalen is author of the book “Inflated: How Money and Debt Built the American Dream.” (Source: Bloomberg)

IN THE SUPERIOR COURT OF FULTON COUNTY

STATE OF GEORGIA

TAMMY JO LONG, CASTLE HOME §

BUILDERS, INC., AND WILLIAM KEITH §

DAVIDSON

v.

JPMORGAN CHASE BANK N.A., BANK

OF AMERICA N.A., BANK OF AMERICA,

NATIONAL ASSOCIATION AS

SUCCESSOR BY MERGER TO LASALLE

BANK NA AS TRUSTEE FOR WAMU

MORTGAGE PASS-THROUGH

CERTIFICATES SERIES 2006-AR19

TRUST, LENDER PROCESSING

SERVICES, INC., NEW ORLEANS

EMPLOYEES’ RETIREMENT SYSTEM,

MARTA/ATU LOCAL 732 EMPLOYERS

RETIREMENT PLAN, WASHINGTON

MUTUAL BANK, F.A., FIRST AMERICAN

EAPPRAISEIT, FIRST AMERICAN, INC.,

WAMU ASSET ACCEPTANCE CORP.,

SHAPIRO & SWERTFEGER, LLP, DOE(S)

ROE(S) AND WASHINGTON MUTUAL

INC.

PLAINTIFF’S FIRST VERIFIED COMPLAINT FOR EMERGENCY TEMPORARY AND PERMANENT INJUNCTIVE RELIEF, DECLARATORY RELIEF & JUDGMENT, FRAUD IN THE FACTUM & INDUCEMENT, FRAUD, ASSIGNMENT & TITLE FRAUD/ SLANDER OF TITLE, VIOLATIONS OF THE GEORGIA RESIDENTIAL MORTGAGE ACT & MORTGAGE FRAUD, VIOLATION OF FAIR DEBT COLLECTION ACT, NEGLIGENT SUPERVISION, TORTIOUS INTERFERENCE WITH CONTRACT AND BUSINESS RELATIONSHIPS, VIOLATION OF FIDUCIARY DUTY, VIOLATION OF DUTY OF GOOD FAITH & FAIR DEALING, VIOLATION OF GEORGIA’S RACKETEERING STATUTES (RICO), COUNT XIII RESCISSION, UNJUST ENRICHMENT, CLAIM FOR ATTORNEY FEES & LITIGATION EXPENSES PURSUANT TO O.C.G.A. §§ 13-6-11 & 13-1-11, BREACH OF CONTRACT, VIOLATIONS OF REAL ESTATE SETTLEMENT PROCEDURES ACT, VIOLATIONS OF FEDERAL TRUTH-IN-LENDING ACT, VIOLATION OF FAIR CREDIT REPORTING ACT, FRAUDULENT MISREPRESENTATION, & USURY & FRAUD

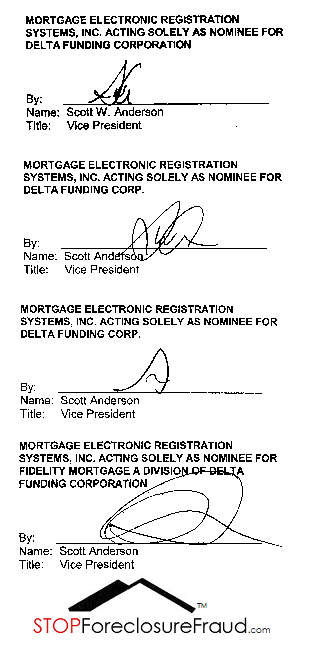

Scott Anderson

Deutsche Bank National Trust Co.

Law Offices of Marshall Watson

New Century Mortgage Corp.

Ocwen Loan Servicing, LLC

Action Date: October 21, 2010

Location: St. Petersburg, FL

On October 21, 2010, in St. Petersburg, Florida, Circuit Court Judge Anthony Rondolino dismissed the plaintiff’s First Amended Complaint in a foreclosure action, Deutsche Bank National Trust Co., et al. v. Donnie J. Decker, et al., Case No. 09-20548-CI-13, 6th Judicial Circuit, in and for Pinellas County, Florida.

The complaint was brought by Deutsche Bank as trustee for a mortgage-backed trust, Morgan Stanley Dean Witter Capital, Inc., under a Pooling & Servicing Agreement dated May 1, 2001. The original complaint was dismissed due to chain-of-title problems.

The amended complaint included an Assignment from New Century Mortgage Corp. to the plaintiff that was executed on February 17, 2010 by Scott Anderson in his capacity as an Executive Vice President of Residential Loan Servicing for Ocwen Loan Servicing, LLC through its authority as Attorney-In-Fact for New Century Mortgage Corporation. Regarding this Assignment, Judge Rondolino commented as follows:

“There is nothing about this assignment which would support a determination at the pleading stage that it is invalid. On the other hand, should evidence be presented at a summary judgment hearing that New Century Mortgage Corporation, LLC became the subject of a bankruptcy proceeding which resulted in a liquidation order, the validity of this assignment would be called into question. Then, absent specific proof that Ocwen had authority from either the bankruptcy court or the liquidation trustee, this disposition of New Century’s (the debtor in bankruptcy) asset there would be a disputed material fact precluding a summary judgment. These concerns however are not ripe at this time…”

In closing, Judge Rondolino warned the plaintiff and its counsel, the Law Offices of Marshall Watson, that any new complaint must be verified, in accordance with the revised Florida Rules of Civil Procedure.

Judge Rondolino then warned very plainly, “If it is thereafter determined that the verification was not based on an appropriate investigation or that the allegations were false, the Plaintiff and the person who signed the verified complaint will be subject to sanctions which may include dismissal of the action with prejudice, assessment of fees and costs, monetary or incarcerative sanctions and referral to the State Attorney for prosecution pursuant to F.S. 837.”

Rondolino’s concerns arose in part because the Assignment came after the foreclosure action was filed. Plaintiff’s law firm is one of four law firms under investigation by the Florida Attorney General for using forged and fraudulent documents in foreclosure actions.

Scott Anderson of Ocwen has been named in foreclosure opinions of Brooklyn Judge Arthur M. Schack as an individual who signs using many different job titles. The trust in this case had a closing date in 2001, but according to the Anderson Assignment, acquired Decker’s non-performing loan in February, 2010. These same or similar facts have been presented in hundreds of foreclosure cases across the country.

Almost every major robo-signer, including Liquenda Allotey, China Brown, Linda Green, Alfonzo Greene, Korell Harp, Bethany Hood and John Kennerty have signed as Attorney-In-Fact for New Century Mortgage Corporation in 2009 and 2010 to transfer mortgages to securitized trusts that closed years earlier.

Judge Rondolino’s opinion lays a blueprint for other judges to follow when presented with mortgage assignments that appear to have been specially created to facilitate foreclosures. It is the first opinion in Florida to warn of possible “incarcerative sanctions.” (Five different versions of the “Scott Anderson” signature are posted in the “Pleadings” section of this web site.)

After a quick review of its procedures, Bank of America this week announced that it will resume its foreclosures in 23 lucky states next Monday. While the evidence is overwhelming that the entire foreclosure process is riddled with fraud, President Obama refuses to support a national moratorium. Indeed, his spokesmen on the issue told reporters three key things. As the Los Angeles Times reported:

A government review of botched foreclosure paperwork so far has found that the problems do not pose a “systemic” threat to the financial system, a top Obama administration official said Wednesday.

Yes, that’s right. HUD reviewed the “paperwork” problem to see whether it threatened the banks — not the homeowners who were the victims of foreclosure fraud. But it got worse, for the second point was how the government would respond to the epidemic of foreclosure fraud.

The Justice Department is leading an investigation of possible crimes involving mortgage fraud.

That language was carefully chosen to sound reassuring. But the fact is that despite our pleas the FBI has continued its “partnership” with the Mortgage Bankers Association (MBA). The MBA is the trade association of the “perps.” It created a ridiculous on its face definition of “mortgage fraud.” Under that definition the lenders — who led the mortgage frauds — are the victims. The FBI still parrots this long discredited “definition.” That is one of the primary reasons why — in complete contrast to prior financial crises — the Justice Department has not convicted a single senior officer of the large nonprime lenders who directed, committed, and profited enormously from the frauds.

Note that the Justice Department is not investigating foreclosure fraud. HUD Secretary Donovan’s statement shows why:

“We will not tolerate business as usual in the mortgage market,” he said. “Where there have been mistakes made or errors, we will hold those entities, those institutions, accountable to stop those processes, review them and fix them as quickly as possible.”

Note the language: “mistakes”, “errors”, “processes” (following the initial use of “paperwork”). No mention of “fraud”, “felony”, “criminal investigations”, or “prosecutions” for the tens of thousands of felonies that representatives of the entities foreclosing on homes have admitted that they committed. Note that Donovan does not even demand that the felons remedy the harm caused by their past fraudulent foreclosures. Donovan wants them to “fix” “processes” — not repair the harm their frauds caused to their victims.

The fraudulent CEOs looted with impunity, were left in power, and were granted their fondest wish when Congress, at the behest of the Chamber of Commerce, Chairman Bernanke, and the bankers’ trade associations, successfully extorted the professional Financial Accounting Standards Board (FASB) to turn the accounting rules into a farce. The FASB’s new rules allowed the banks (and the Fed, which has taken over a trillion dollars in toxic mortgages as wholly inadequate collateral) to refuse to recognize hundreds of billions of dollars of losses. This accounting scam produces enormous fictional “income” and “capital” at the banks. The fictional income produces real bonuses to the CEOs that make them even wealthier. The fictional bank capital allows the regulators to evade their statutory duties under the Prompt Corrective Action (PCA) law to close the insolvent and failing banks.

PLANTATION, Fla., Oct. 22, 2010 (GLOBE NEWSWIRE) — DJSP Enterprises, Inc. (Nasdaq: DJSP) (Nasdaq:DJSPW) (Nasdaq:DJSPU) today announced that it has instituted further staff reductions as a result of continued reduced file volumes. DJSP has reduced its staffing levels by an additional 198 employees, bringing the total number of layoffs to approximately 300 since the reduction in staff was initiated.

About DJSP Enterprises, Inc.

DJSP is the largest provider of processing services for the mortgage and real estate industries in Florida and one of the largest in the United States. We provide a wide range of processing services in connection with mortgages, mortgage defaults, title searches and abstracts, REO (bank-owned) properties, loan modifications, title insurance, loss mitigation, bankruptcy, related litigation and other services. Our principal customer is The Law Offices of David J. Stern, P.A. (“DJSPA”). We are headquartered in Plantation, Florida, with additional operations in Louisville, Kentucky and San Juan, Puerto Rico. Our U.S. operations are supported by a scalable, low-cost back office operation in Manila, the Philippines, that provides data entry and document preparation support for our U.S. operations.

Forward Looking Statements

This press release contains forward-looking statements about us within the meaning of the Private Securities Litigation Reform Act of 1995 (the “Act”), including but not limited to management’s expectations about the impact of our expense reduction efforts and recent developments in the residential mortgage foreclosure industry. Additionally, words such as “anticipate,” “believe,” “estimate,” “expect” and “intend” and other similar expressions are forward-looking statements within the meaning of the Act. Such forward-looking statements are based upon the current beliefs and expectations of our management and are subject to risks and uncertainties, which could cause actual results to differ from the forward looking statements. The following factors, among others, could cause actual results to differ from those set forth in the forward-looking statements: business conditions, changing interpretations of generally accepted accounting principles; outcomes of government or other regulatory reviews, particularly those relating to the regulation of the practice of law; the impact of inquiries, investigations, litigation or other legal proceedings involving us or our affiliates, which, because of the nature of our business, have happened in the past to us and DJSPA; the impact and cost of continued compliance with government or state bar regulations or requirements; legislation or other changes in the regulatory environment, particularly those impacting the mortgage default industry; unexpected changes adversely affecting the businesses in which we are engaged; fluctuations in customer demand; our ability to manage growth and integrate acquisitions; intensity of competition from other providers in the industry; general economic conditions, including improvements in the economic environment that slows or reverses the growth in the number of mortgage defaults, particularly in the State of Florida; the ability to efficiently expand our operations to other states or to provide services we do not currently provide; the impact and cost of complying with applicable U.S. Securities and Exchange Commission (“SEC”) rules and regulations; geopolitical events and changes, as well as other relevant risks detailed in our filings with the SEC, including our Annual report on Form 20-F for the period ended December 31, 2009, which are available at the SEC’s internet site (http://www.sec.gov). Forward-looking statements in this press release speak only as of the date of the press release, and we assume no obligation to update forward-looking statements or the reasons why actual results could differ.

CONTACT: DJSP Enterprises, Inc. Chris Simmons, Director of Investor Relations 954-233-8000 ext. 1744 Cell: 954-294-9095 900 South Pine Island Rd. Plantation, FL 33324

And my duties at

21 that point was a consultant for certain investors that

22 we — that we acquired their pools of loans.

23 And I was that go-to person for that investor,

24 and it was Morgan Stanley and Goldman Sachs at the time.

25 And we acquired — we didn’t acquire, but I acquired

1 Ohio [phonetic] Savings as one of my relationships that

2 I had; and they — I was the go-to person for any of

3 their reporting, any questions they may have had on one

4 of their loans in their pools that we were servicing.

5 So I was that go-to person in client relations, and that

6 position —

7 Q. Can you define what being a go-to person

8 entailed?

9 A. Basically if there — again, if there was

10 questions on a particular loan in the pool, if there was

11 an acquisition or they were selling a certain pool of

12 loans, you know, they’d send me up the numbers reports.

13 Q. Okay. For example, you say questions regarding a

14 particular loan in a certain pool. What would be an

15 example of a type of question that you might get?

16 A. I may get a phone call from the investor, I’ve

17 got this particular loan that perhaps is in foreclosure,

18 REO, I need some details of what’s going on, where that

19 loan is at in the process of foreclosure, or perhaps it

20 was an REO. And then my job was to go to those

21 different areas, those different departments and get the

22 details for the client.

<SNIP>

4 Q. You have, okay. So it’s your testimony that

5 you’ve never seen this one, though?

6 A. Correct.

7 Q. Okay. But you did review all of the documents

8 that were produced in connection with this case?

9 A. This is the history that I reviewed.

10 Q. Okay. Not the question. The question was did

11 you review all of the documents that Wells Fargo

12 produced in connection with this case?

13 A. I did.

14 Q. Okay. Did you review all the documents —

15 MR. ALFIERI: Objection, form.

16 Q. (By Mr. Bartholow) Did you review all of the

17 documents that I produced on behalf of the Guevaras in

18 connection with this case?

19 A. I have.

20 Q. Okay. And so it’s your testimony that you have

21 never seen that document before?

22 A. I do not recall looking at this particular

23 account activity statement.

24 Q. Okay. Do you know how Wells Fargo determines

25 when and whether to charge a late fee?

1 A. I do.

2 Q. Okay. How do they do it?

3 A. Okay. After the — after the 15-day grace period

4 — and this is typical. Some notes can vary, but it’s

5 typical that the payment is due on the 1st of the month;

6 and after 15 days a late fee is assessed on the 16th of

7 the month. And typically that’s 5 percent of what their

8 payment is.

9 Q. Is it assessed every time?

10 A. Every — each time the payment is late, yes, a

11 late fee is assessed if it’s not received by the due

12 date or the grace period that’s been granted.

13 Q. Are there any exceptions that would be made?

14 A. Not that I’m aware of.

15 Q. Okay. Are you aware of any changes to Wells

16 Fargo’s accounting practices following April of 2007?

17 MR. ALFIERI: Objection, form.

18 A. I am not.

19 Q. (By Mr. Bartholow) Okay. And specifically with

20 regard to how Wells Fargo books receipts and pays late

21 fees from those receipts, have you ever heard of any

22 changes being made?

23 A. I have not.

24 Q. Okay. Are you familiar with Freddie Mac

25 Servicing Guidelines?

1 A. If it pertains to what I do on a daily basis,

2 yes.

3 Q. Okay. And what does that include?

4 A. General servicing of the loan. I do — I have

5 some knowledge of how the custodial files are held.

6 Q. How are the custodial files held?

7 A. It’s designated by Freddie Mac who the custodian

8 would be.

9 Q. I’m sorry, what is designated?

10 A. Who the custodial facility would be, who the

11 custodian would be.

12 Q. Where would that designation be, or how does

13 that designation — I mean, does it appear on a computer

14 screen? Is it in a file?

15 A. It — in general I’m just — no, it would not

16 be — it would not be — are you asking in relation to

17 this loan or just in general?

18 Q. I want to know what your knowledge is —

19 A. Okay.

20 Q. — regarding the custodial procedures pertaining

21 to Freddie Mac and their guidelines.

22 MR. ALFIERI: Okay. Ask — wait for the

23 question.

24 THE WITNESS: Thank you.

25 MR. ALFIERI: Mr. Bartholow will ask you a

1 question. Answer the question.

2 A. Okay. Could you re-ask the question, please?

3 Thank you.

4 Q. (By Mr. Bartholow) Okay. You stated a moment

5 ago that you were familiar with the custodian — custody

6 guidelines for Freddie Mac, correct?

7 A. Yes, correct.

8 Q. Okay. What are the custody guidelines for

9 Freddie Mac? What is your knowledge of them anyway?

10 MR. ALFIERI: Ask a specific question to my

11 witness, please.

12 MR. BARTHOLOW: That is as specific as I can

13 get.

14 Q. (By Mr. Bartholow) Please answer the question if

15 you can.

16 MR. ALFIERI: Objection, form.

17 Q. (By Mr. Bartholow) You can answer if you know,

18 if you’re able. If you’re unable, that’s fine. We

19 can — I can pull out some Freddie guidelines and we can

20 talk about them specifically.

21 A. Okay. Let’s move forward.

22 (Exhibit No. 10 was marked.)

23 Q. (By Mr. Bartholow) The document I am handing you 24 is a custodian certification schedule summary form

25 1034S. Have you seen this form before?

As much as state attorneys general could be an effective force in acting for consumers and investors against banks, the fact that an attorney general has saddled up does not necessarily mean the effort is serious. At a minimum, it might just be a gambit to garner some good PR without seriously inconveniencing the perps; at worse, the action might be a pure Trojan horse.

Consider the curious conduct of one Bill McCollum, the lame duck attorney general of Florida. It appears that McCollum has been going after the foot soldiers in the foreclosure chicanery business (although some of them, like David Stern, head of the biggest foreclosure mill in the state, have earned a tidy fortune). His recent actions have targeted firms offering dubious foreclosure advice, and more recently, the foreclosure mills as well as a firm that may be best known for its real estate related document fabrication activities, Lender Processing Services, through its DocX subsidiary.

Now starting with these actors isn’t a bad thing at all; in fact, prosecutors often target low level criminals with the hope of getting them to turn evidence on the kingpins. And there is good reason to think McCollum has no interest in asking tough questions that will inconvenience bigger fry.

McCollum Is falling in with the banking industry party line. He appears to regard not disrupting the foreclosure process, a top priority of the financiers, as a worthy goal. Gee, isn’t preserving the rule of law and making sure no one is abused or defrauded the sort of thing his office is tasked to defend, not the functioning of markets or the bottom lines of banks? From the Wall Street Journal (hat tip reader f247):

“They’re training a lot of new people, and apparently now they are comfortable with the legality of their foreclosure process,” Mr. McCollum said in an interview. “The primary purpose of these meetings is talking about not having this stuff held back. It’s very important for us to not have a backlog of foreclosures. We already have a backlog. We don’t want it to get worse.”…

Mr. McCollum, Florida’s attorney general, said most errors in the foreclosure process have been “procedural,” adding that his top priority is to resolve the mess in a way that allows foreclosures to resume quickly….

The talks also centered on how to quickly get the foreclosure process moving again, according to the Florida attorney general’s office. Mr. McCollum described the meeting as more cooperative than combative.

A few weeks after he started working at Ameriquest Mortgage, Mark Glover looked up from his cubicle and saw a coworker do something odd. The guy stood at his desk on the twenty-third floor of downtown Los Angeles’s Union Bank Building. He placed two sheets of paper against the window. Then he used the light streaming through the window to trace something from one piece of paper to another. Somebody’s signature.

Glover was new to the mortgage business. He was twenty-nine and hadn’t held a steady job in years. But he wasn’t stupid. He knew about financial sleight of hand — at that time, he had a check-fraud charge hanging over his head in the L.A. courthouse a few blocks away. Watching his coworker, Glover’s first thought was: How can I get away with that? As a loan officer at Ameriquest, Glover worked on commission. He knew the only way to earn the six-figure income Ameriquest had promised him was to come up with tricks for pushing deals through the mortgage-financing pipeline that began with Ameriquest and extended through Wall Street’s most respected investment houses.

Glover and the other twentysomethings who filled the sales force at the downtown L.A. branch worked the phones hour after hour, calling strangers and trying to talk them into refinancing their homes with high-priced “subprime” mortgages. It was 2003, subprime was on the rise, and Ameriquest was leading the way. The company’s owner, Roland Arnall, had in many ways been the founding father of subprime, the business of lending money to home owners with modest incomes or blemished credit histories. He had pioneered this risky segment of the mortgage market amid the wreckage of the savings and loan disaster and helped transform his company’s headquarters, Orange County, California, into the capital of the subprime industry. Now, with the housing market booming and Wall Street clamoring to invest in subprime, Ameriquest was growing with startling velocity.

The foreclosure case against Patrick Jeffs was thrown out of court when a Jacksonville judge ruled that the summons to inform him of the lawsuit was counterfeit.

Mark Browne was in Iraq when a process server tried to give his mother in New Mexico a summons to inform him that his house in Jacksonville was being foreclosed on. She didn’t accept it, but the server signed a document that said she did. A judge threw that out, too.

Nancy Rush sold her Jacksonville condo in March, walking away poorer after the short sale and was getting on with her life when her phone rang with unlikely news: She was in foreclosure. A week after she unloaded the unit at Kendall Town in Arlington, a Jacksonville judge ordered the home sold at auction to settle a $190,000 mortgage debt, even though Rush had never received a summons saying she was being sued. “I didn’t even know there was a court date,” Rush said. “It scared the crap out of me.”

Even the summons, the simple but important legal notice required to inform homeowners that they are being foreclosed on, has not been immune to the massive problems surrounding what has become known in Florida and across the nation as the foreclosure mess.

The Times-Union has reviewed documents where the same name with obviously different signatures was used to certify that papers were served to the homeowner.

While there is no simple way to know how often every type of irregularity occurs, there is documentation showing a sharp rise in one narrow area of concern.

Instances where summonses entrusted to servers have been reported as lost, once fairly rare, have skyrocketed, making it harder to document the fate of important paperwork. From barely more than 100 annually six years ago, more than 2,000 summonses have been lost in Duval County in each of the last two years.

Critics attribute the problems to both sloppiness and fraud.

Tammie Lou Kapusta, a paralegal in the office of David Stern, the foreclosure law firm at the center of much of the investigations, described the serving process as “a complete mess” during a recent deposition. Renters were served rather than property owners, Kapusta told the Florida Attorney General’s Office. An affidavit of service – the legal document required to verify that the summons was served properly – would be filed when the summons hadn’t been served, she said.

Feel sorry for the poor robo-signer who had to sign 1,000 foreclosure files a day? Then here’s some good news: allegations are now surfacing that at least one robo-signer got help from co-workers.

Imagine standing in your front yard and watching as a car pulls up. A stranger gets out, walks up to you, verifies your identity, then serves you with foreclosure papers. Now imagine that you’ve never missed a mortgage payment in your life.

You’ve seen the headlines about banks stopping foreclosures – but if you haven’t yet realized the implications for every American, this is a story you don’t want to miss.

There’s been plenty of recent media attention to the prospect of investor lawsuits over fraudulent mortgages and mortgage securities. But investor lawsuits against mortgage servicers could be even more damaging than these other lines of legal inquiry. The four largest banks hold nearly half a trillion dollars worth of second-lien mortgages on their books—loans that could be decimated if investors successfully target improper mortgage servicing operations. The result would be major trouble for the financial system. The result would be major trouble for too-big-to-fail behemoths.

Mortgage servicers are the banking industry’s debt collectors. They accept payments and forward them along to investors who own mortgage securities– servicers themselves don’t actually own the mortgages they handle. This is a recipe for trouble for a variety of reasons, but one of the biggest problems is the fact that the nation’s four largest banks also operate the four largest mortgage servicers. Bank of America, Wells Fargo, JPMorgan Chase and Citigroup service about half of all mortgages in the United States. They also have multi-trillion-dollar businesses whose interests often conflict with those of mortgage security investors.

Richard M. Bowen, former chief underwriter for Citigroup’s consumer-lending group, said he warned his superiors of concerns that some types of loans in securities didn’t conform with representations and warranties in 2006 and 2007.

“In mid-2006, I discovered that over 60 percent of these mortgages purchased and sold were defective,” Bowen testified on April 7 before the Financial Crisis Inquiry Commission created by Congress. “Defective mortgages increased during 2007 to over 80 percent of production.”

<SNIP>

“The potential for owners to challenge lenders on foreclosure improprieties certainly is there,” Pallotta said. “Even if it turns out that the banks were right in 99 percent of these foreclosures, the additional diligence on their part, going forward, is going to cost them more money.”

The litigation over buybacks, also known as putbacks, can also pit big banks against each other. Last month, Deutsche Bank AG, acting as a trustee, refiled a lawsuit over misrepresented mortgages in $34 billion of Washington Mutual Inc. mortgage securities, with $165 billion in original balances.

The new suit in the U.S. District Court for the District of Columbia included JPMorgan as a defendant, after the Federal Deposit Insurance Corp. said that JPMorgan was wrongly claiming its insurance fund had agreed to cover the liabilities, according to the amended complaint.

Washington Post Staff Writer

Thursday, October 21, 2010; 10:09 AM

The federal bailout for Fannie Mae and Freddie Mac could more than double in size during the next three years, according to projections from the companies’ federal regulator.

Fannie and Freddie, the federally-controlled mortgage finance giants, will likely need at least another $73 billion and perhaps as much $215 billion from taxpayers in the next three years to meet their financial obligations, the Federal Housing Finance Agency said.

The growing taxpayer infusions will cover losses Fannie and Freddie suffer on home loans, as well as payments the companies must make to the U.S. Treasury in exchange for a federal guarantee to provide cash to keep the companies solvent.

In fact, over time, the majority of funds flowing to Fannie and Freddie from taxpayers will go to pay that dividend.

To date, the Treasury has already injected $148 billion into Fannie and Freddie. Under the worst-case scenario, in which the country enters a second recession, the total infusion would equal $363 billion in three years.

Just a friendly reminder to you that you’re still missing the target by a looooooooong shot.

In order for anyone to have standing to foreclose in the first place one needs to perfect the chain of title.

An assignment of mortgage is the document which indicates that a mortgage has been transferred from the original lender or borrower to a third party. Assignments of mortgage are more commonly seen when lenders sell mortgages to other lenders. When someone has what is known as an assumable mortgage, it is possible for the borrower to transfer the mortgage to another person, in which case an assignment of mortgage will need to be filed to record the transaction.

Before anyone can produce any affidavits period…they first must have equitable rights transferred!

PRESENT:

Honorable Karen V. Murphy

Justice of the Supreme Court

Index No. 5541/09

IN THE MATTER OF:

MORTGAGE ELECTRONIC REGISTRATION

SYSTEMS, INC. as NOMINEE for ENCORE

CREDIT CORP.,

-against-

DIANA ESPOSITO a/kla DIANE ESPOSITO;

BANK OF AMERICA, N. ; NASSAU COUNTY

CLERK,

Excerpt:

The supporting affidavits are in conflict with the recorded satisfaction in that the

satisfaction executed by MERS as nominee for Encore states that there had been no

assignments.There is a purported, and as yet unrecorded assignment from MERS as nominee

for Encore to Bank of America dated March 12, 2009.This Court is left to question the

motivation behind MERS’ assignment of a mortgage previously satisfied of record during

the pendency of this matter.There is no proof that MERS physically delivered the note and

mortgage to Bank of America prior to the date ofthe assignment. (See Wells Fargo Bank,

N.A. v. Marchione , 2009 WL 3380639 (2d Dept. , 2009)).

Pacific Investment Management Co., BlackRock Inc. and the Federal Reserve Bank of New York are seeking to force Bank of America Corp. to repurchase soured mortgages packaged into $47 billion of bonds by its Countrywide Financial Corp. unit, people familiar with the matter said.

A group of bondholders wrote a letter to Bank of America and Bank of New York Mellon Corp., the debt’s trustee, citing alleged failures by Countrywide to service loans properly, their lawyer said yesterday in a statement that didn’t name the firms. The New York Fed acquired mortgage debt through its 2008 rescues of Bear Stearns Cos. and American International Group Inc.

Investors are stepping up efforts to recoup losses on mortgage bonds, which plummeted in value amid the worst slump in home prices since the 1930s. Last month, BNY Mellon declined to investigate mortgage files in response to a demand from the bondholder group, which has since expanded. Countrywide’s servicing failures, including insufficient record keeping, may open the door for investors to seek repurchases by bypassing the trustee, said Kathy Patrick, their lawyer at Gibbs & Bruns LLP.

“We now are in a position where we have to start a clock ticking,” Patrick, who is based in Houston, said today in a telephone interview.

If the issues aren’t fixed within 60 days, BNY Mellon should declare Countrywide in default on its servicing contracts, Patrick said.

P R E S E N T :

Hon. RALPH. T. GAZZILLO

Justice of the Supreme Court

MORTGAGE ELECTRONIC REGISTRATION

SYSTEMS, INC.

c/ 0 Wells Fargo Bank, NA

3470 Stateview Boulevard

Ft, Mill, SC 2971 5

v.

THOMAS STANDFORD, UNITED STATES

OF AMERICA ACTING THROUGH THE IRS

EXCERPT:

Based up0n the submissions herein, it appears that plaintiff “MERS” had no standing to

commence the present action as it was not the owner of the mortgage and note when the action was

commenced. As of January 28,2005, “MERS” had already relinquished its interest in the note and

mortgage and at no subsequent lime did it regain an interest in the subject mortgage and note. In

addition, the affidavit of merit that is attached in support of the moving papers as Exhibit C, was

executed b) “Certifying Officer” Carolyn Brown of “MERS” on February 13,2009. “MERS” had no

demonstrable interest or standing in this matter on Feb.l3,2009 and, accordingly, the affidavit of its

of officer has no probative value.

Bethany Hood

Lender Processing Services, Inc.

MERS

Action Date: October 20, 2010

Location: South Bend, IN

On September 30, 2010, U.S. Bankruptcy Judge Harry C. Dees, Jr., Northern District of Indiana, South Bend Division, confronted head-on the widespread practice of employees of mortgage servicing companies signing Mortgage Assignments with false job titles, in Koontz v. EverHome Mortgage and Mortgage Electronic Registration Systems, Inc., Case No. 09-30024, Proc. No. 10-3005.

In this contested foreclosure, EverHome and MERS moved for summary judgment, while the plaintiff homeowners argued that there were genuine issues of material fact that precluded summary judgment. One such issue involved a Mortgage Assignment signed by Bethany Hood as Vice President of Mortgage Electronic Registration Systems, Inc. (“MERS”). (Regular readers of Fraud Digest will recognize that Bethany Hood is a clerical employee of Lender Processing Services who works in the Mendota Heights, MN office and who signs thousands of mortgage documents monthly using at least 20 different job titles.)

Here is what the Court said about this:

“MERS, in its Answer to the plaintiff’s Complaint, admit(ted) that Bethany Hood is not an employee of MERS. (cite omitted).

The debtor claimed that the document [assignment signed by Bethany Hood as a MERS officer] was fabricated and MERS has offered no other explanation, nor has it submitted properly authenticated documentation of an assignment. It appears to this Court that a fraudulent recorded Assignment of Mortgage might still be found today in the St. Joseph’s County Recorder’s Office, despite MERS’ knowledge of the false signature.

Indeed, MERS has completely sidestepped the fact that this Assignment was signed by someone representing herself to be a Vice President of MERS, and it has declined to explain why this false document was attached to the amended Proof of Claim… In the view of this court, the conduct of the EverHome defendants and the MERS defendant – reflecting a lack of transparency and determination not to provide information or documents until required – has burdened both the debtor and this Court…On this case, the Creditors have been forced to admit that a non-employee signed the Assignment of Mortgage, representing herself to be a Vice President of MERS and other banks or mortgage companies held the Mortgage and or Note at issue… Having determined that genuine issues of material fact exist, the Court denies the Motions for Summary Judgment filed by the EverHome defendants and MERS…” How many other Mortgage Assignments signed by individuals falsely claiming to be Vice Presidents of MERS have been filed since 2008?

It is likely that the number is greater than ten million.

FRANCIS R. BALOUN and ANTOINETTE M. BALOUN, Appellant(s),

v.

CITIMORTGAGE, INC., etc., Appellee(s).

Case No. 5D09-2793.

District Court of Appeal of Florida, Fifth District.

Opinion filed October 15, 2010

Michael E. Rodriguez, of Foreclosure Defense Law Firm, PL, Tampa, for Appellants.

Forrest G. McSurdy, of Stern & McSurdy, Law Offices of David J. Stern, P.A., Plantation, for Appellees.

ON CONCESSION OF ERROR

PER CURIAM.

Pursuant to the Appellees’ concession of error, the order granting summary final judgment in foreclosure is reversed and this cause is remanded for further proceedings.

New York is instituting new filing requirements in order to ensure the integrity of the home foreclosure process, the state’s chief judge said Wednesday.

Lawyers bringing foreclosure claims will now be required to file an affirmation that they themselves have taken reasonable steps to verify the accuracy of documents filed in support of residential foreclosures.

“We cannot allow the courts in New York State to stand by idly and be party to what we now know is a deeply flawed process, especially when that process involves basic human needs–such as a family home–during this period of economic crisis,” said New York State Chief Judge Jonathan Lippman in a statement.

The new filing requirement goes into effect immediately. In new cases, the affirmation must be filed along with the initial request for judicial intervention. In pending cases, it must accompany a request for judgment or must be submitted to the court referee if a judgment has been entered, but the property hasn’t yet sold.

![[NYSC] MERS HAS NO INTEREST, STANDING, OFFICER AFFIDAVIT HAS NO PROVATIVE VALUE](https://stopforeclosurefraud.com/wp-content/themes/gazette/thumb.php?src=wp-content/uploads/2010/10/wellsmers.png&w=100&h=57&zc=1&q=90)

{kind=link}

Recent Comments