It was a very sad day for Floridians yesterday when the Florida Supreme Court issued a statement that it does not have authority to intercede while a fraud investigation is pending. Although we may not agree with the decision, we must respect procedures that must be followed.

Florida, do not quit what you are doing because there are many states that we must continue to focus on. Judges need to put themselves in the homeowners situation and understand we cannot make these fraudulent documents up. These documents are sworn statements, under perjury of law and notarized. As officers of the court they must be held accountable. No ifs, ands, buts or suppose here. These are not errors.

Rest assured that The Florida Bar still has many pending investigations with these foreclosure firms and they have authority overseeing the misconduct of their members.

I am your voice, America. I share your fears, read your concerns and do try my best to reach out to you.

The Florida Constitution and court rules did not give the Chief Justice authority to intercede in pending cases involving attorney misconduct, or to investigate allegations of fraud or misconduct in foreclosure cases. The fraud cases must first beadjudicated in trial courts.

Congressman Grayson has asked the Florida Bar to take action.

Florida Default Law Group has been added as the fourth law firm under investigation along the Law offices of David J. Stern, Shapiro & Fishman and Law Office of Marshall Watson.

See where Judge Schack takes this and even if not mentioned he makes reference to MERS. Every judge must follow his example and read and research each case because it the end “each case is unique”.If we can only make a rubber stamp weigh 2 tons?? Hmm

By GREGORY BRESIGER Last Updated: 1:29 AM, September 26, 2010 Posted: 1:07 AM, September 26, 2010

With foreclosure filings growing by the month, some judges are holding banks and loan servicers’ feet to the fire to prove they “own” the mortgage and that they know what information is in the filing.

Recently, JPMorgan Chase, a mortgage servicer, was charged by a Florida judge with submitting fraudulent foreclosure paperwork on a home it did not own.

Ally Bank, formerly GMAC, the credit arm of the troubled automaker General Motors, suspended foreclosure proceedings in 23 states including New York last week, while it reviews its foreclosure procedures.

Ally, which has a $349.1 billion mortgage portfolio, according to industry records, and was also the beneficiary of more than $17 billion in US bailout funds, said this week it has amended its foreclosure procedure to make sure the documents contain truthful information and that there is a notary present when documents are signed.

Closer to home, in New York State Supreme Court no foreclosure hearing is routine in Judge Arthur Schack’s courtroom in Brooklyn. That’s where dozens of bank attorneys are learning that every detail must be right or else.

Judge Schack — the scourge of numerous banks and poorly prepared attorneys — has thrown out dozens of foreclosure applications for just the same reasons cited in Florida.

Judge Schack examines every filing in detail. That’s because “every case is unique,” said the 64-year-old judge, a former high-school social-studies teacher.

Why the large number of foreclosure dismissals for a procedure that is often routinely granted?

Ally’s GMAC unit withdraws foreclosure affidavits signed by second employee

By Ariana Eunjung Cha | September 25, 2010; 11:34 AM ET

Was Kristine Wilson another “robo-signer”?

Attorneys for homeowners in Florida say Ally Financial’s GMAC mortgage unit has begun to withdraw affidavits submitted in support of foreclosures that were signed by a second employee. Like Jeffrey Stephan–the document processor who admitted in sworn testimony that he signed 10,000 documents a month without reviewing them–Kristine Wilson signed as a “limited signing officer” for GMAC.

In a request to withdraw an affidavit listing debts owed by a homeowner that was signed by Wilson in a Palm Beach County Circuit Court case, lawyers for GMAC say that “information in the affidavit may not have been properly verified.”

Sept. 25 (Bloomberg) — Attorneys general in three U.S. states are investigating foreclosures at Ally Financial Inc.’s GMAC Mortgage unit after the lender said it would halt some evictions following a discovery of faulty documentation.

Texas, Iowa and Illinois have started investigations into mortgage practices at Ally, while California, which isn’t affected by GMAC’s action, ordered the company to stop foreclosures unless it can prove compliance with state law, according to statements. Ally said it has issued a “more robust policy” on processing foreclosures, increased staff to handle documents and instituted more training for employees.

“Preserving the integrity of the foreclosure process is of the utmost importance,” Ally said yesterday in a statement. “While we are exercising an abundance of caution in the review process, we are confident that the processing errors did not result in any inappropriate foreclosures.”

Continue reading…BUSINESS WEEK

.

September 24, 2010

ATTORNEY GENERAL MADIGAN DEMANDS MEETING WITH

MORTGAGE LENDER AT CENTER OF FORECLOSURE CONTROVERSY

GMAC Suspected of Submitting False Documents in Foreclosure Cases

Chicago Attorney General Lisa Madigan today issued a letter to the mortgage lender Ally (formerly GMAC) demanding a meeting to address concerns that the company has violated the state’s Consumer Fraud Act in its pursuit of Illinois homeowners in foreclosure. Madigan’s letter responds to reports raising serious questions about the accuracy of documents the lender files in foreclosure lawsuits.

An Ally employee testified in a Florida court case that he routinely signed affidavits for foreclosure lawsuits and submitted them to Ally’s attorneys without reviewing the homeowners’ loan documents. These affidavits were then filed with the court as evidence of Ally’s right to foreclose on the homes. The employee testified that he signed at least 10,000 affidavits a month without reviewing the underlying paperwork, and thus had no way of knowing whether the information in the affidavits was actually true.

“Families’ homes are at stake here,” Madigan said. “If I determine that Ally is rubber-stamping affidavits and filing them with our courts as evidence, I will take appropriate action. The law demands that lenders prove their case in foreclosure actions, and Illinois homeowners demand the same.”

Following these revelations, Ally announced this week that it is suspending foreclosure lawsuits in 23 states, including Illinois.

Madigan also requested that Ally immediately provide her office with details on the impact of Ally’s conduct on Illinois homeowners, including the number of Illinois homeowners affected by the suspension of foreclosures; the names of the Illinois law firms that Ally retains to pursue foreclosure actions; information about how these firms will implement and monitor the suspension of foreclosure lawsuits in Illinois; and the length of the suspension.

GMAC ranked fourth among U.S. home mortgage lenders in the first six months of this year, according to Inside Mortgage Finance, an industry newsletter.

THIS IS HUGE! Coming in… Florida might halt all Foreclosures…While pending investigation of MILLS!

SUPREME COURT,

Do what is right and protect these families. This involves children that do not understand what is going on. I lost my home to this fraud and they do not have to go through my stressful experience. You set new rules and these foreclosure mills continued to ignore you. What is it going to take?

I revere the law, the judicial system, and the legal profession and will at all times in my professional

and private lives uphold the dignity and esteem of each.

I will further my profession’s devotion to public service and to the public good.

I will strictly adhere to the spirit as well as the letter of my profession’s code of ethics, to the extent

that the law permits and will at all times be guided by a fundamental sense of honor, integrity, and fair

play. I will not knowingly misstate, distort, or improperly exaggerate any fact or opinion and will not

improperly permit my silence or inaction to mislead anyone.

I will conduct myself to assure the just, speedy and inexpensive determination of every action and

resolution of every controversy.

I will abstain from all rude, disruptive, disrespectful, and abusive behavior and will at all times act

with dignity, decency, and courtesy.

I will respect the time and commitments of others.

I will be diligent and punctual in communicating with others and in fulfilling commitments. I will exercise independent judgment and will not be governed by a client’s ill will or deceit.

My word is my bond.

Oath of Admission to The Florida Bar

The general principles which should ever control the lawyer in the practice of the legal profession

are clearly set forth in the following oath of admission to the Bar, which the lawyer is sworn on

admission to obey and for the willful violation to which disbarment may be had.

“I do solemnly swear:

“I will support the Constitution of the United States and the Constitution of the State of Florida;

“I will maintain the respect due to courts of justice and judicial officers;

“I will not counsel or maintain any suit or proceedings which shall appear to me to be unjust, nor

any defense except such as I believe to be honestly debatable under the law of the land;

“I will employ for the purpose of maintaining the causes confided to me such means only as are

consistent with truth and honor, and will never seek to mislead the judge or jury by any artifice or false

statement of fact or law;

“I will maintain the confidence and preserve inviolate the secrets of my clients, and will accept no

compensation in connection with their business except from them or with their knowledge and approval;

“I will abstain from all offensive personality and advance no fact prejudicial to the honor or reputation

of a party or witness, unless required by the justice of the cause with which I am charged;

“I will never reject, from any consideration personal to myself, the cause of the defenseless or

oppressed, or delay anyone’s cause for lucre or malice. So help me God.”

California officials today demanded that Ally Financial Inc. stop foreclosing on homes in the state, citing reports indicating the big mortgage lender is violating the law.

The cease-and-desist letter, issued by Attorney General Jerry Brown, came as officials in several other states began investigating Ally’s operations.

The controversy stems from a Florida court case in which an Ally official reportedly testified that he signed thousands of documents in foreclosure cases without even reviewing the homeowners’ loan documents.

This should send a powerful message to each and every Foreclosure Mill out there! You are NEXT!

September 24, 2010

Michael J. Williams

President and Chief Executive Officer

Fannie Mae

3900 Wisconsin Avenue, N.W.

Washington, D.C. 20016

Dear Mr. Williams,

We are disturbed by the increasing reports of predatory ‘foreclosure mills’ in Florida working for Fannie Mae servicers. Foreclosure mills are law firms representing lenders that specialize in speeding up the foreclosure process, often without regard to process, substance, or legal propriety. According to the New York Times, four of these mills are both among the busiest of the firms and are under investigation by the Attorney General of Florida for fraud. The firms have been accused of fabricating or backdating documents, as well as lying to conceal the true owner of a note.

Several of the busiest of these mills show up as members of Fannie Mae’s Retained Attorney Network, a set of legal contractors on whom Fannie relies to represent its interests as a note-holder. The network also serves as a pool of legal talent that represents Fannie in its pre-filing mediation program, a program designed to facilitate communication between borrowers and servicers prior to foreclosure. In other words, Fannie Mae seems to specifically delegate its foreclosure avoidance obligations out to lawyers who specialize in kicking people out of their homes.

The legal pressure to foreclose at all costs is leading to a situation where servicers are foreclosing on properties on which they do not even own the note. This practice is blessed by a legal system overwhelmed with foreclosure cases and unable to sort out murky legal details, and a set of law firms who mass produce filings to move foreclosures as quickly as possible. At the very least, we would encourage you to remove foreclosure mills under investigation for document fraud from the Fannie Mae’s Retained Attorney Network. We also believe that Fannie should have guidelines allowing servicers to proceed on a foreclosure only when its legal entitlement to foreclose is clearly documented. In addition, these charges raise a number of questions for us about the foreclosure process as it pertains to Fannie Mae’s holdings.

Why is Fannie Mae using lawyers that are accused of regularly engaging in fraud to kick people out of their homes? Given that Fannie Mae is at this point a government entity, and it is the policy of the government that foreclosures are a costly situation best avoided if there are any lower cost alternatives, what steps is Fannie Mae taking to avoid the use of foreclosure mills? What additional steps is Fannie Mae going to take to ensure that foreclosures are done only when necessary and only in accordance with recognized law? How do your servicer guidelines take into account the incentives for fraud in the fee structure of foreclosure attorneys and others engage in the foreclosure process? What mechanisms do you employ to monitor legal outsourcing?

We look forward to your responses and to understanding more about these disturbing dynamics in future hearings.

By The Palm Beach Post

Updated: 7:45 p.m. Thursday, Sept. 23, 2010

Posted: 7:33 p.m. Thursday, Sept. 23, 2010

Last month, Palm Beach County Senior Judge Roger Colton opened his afternoon foreclosure session by telling homeowners that he’d heard all their stories before, and he would give them a maximum of five months before letting lenders take their homes.

“I know all about the Chinese drywall problems. I know all about sickness,” Judge Colton said. “I know all about divorce. I know all about anything else as to why we find ourselves in this position today.”

In the first case, Judge Colton signed a final summary judgment giving Everhome Mortgage Co. the right to foreclose on a Lake Worth couple’s home despite their attorney’s objections that Everhome had failed to prove that it owns the note. Foreclosure defense lawyers cite the case as an egregious example of Florida’s so-called “rocket docket,” the process of expediting foreclosure cases through the courts by siding with lenders.

That was not the intent of state legislators this year when they appropriated $9.6 million to reduce the foreclosure backlog. Though the state has set a goal of reducing the more than 500,000 cases by 62 percent within a year, that goal should be met by handling each case based on its merit and not by watching the clock. That’s particularly important given the fraud perpetrated by lenders – many of which knowingly issued loans to buyers who couldn’t afford them – and their attorneys.

Tampa-based Florida Default Law Group has been withdrawing legal affidavits in its GMAC Mortgage foreclosure cases, acknowledging that information it gave to courts may have been inaccurate. The affidavits supposedly attest to the validity of documents submitted to verify that a lender has the right to foreclose. Florida law requires that lenders prove ownership of the note underlying the mortgage.

In the case before Judge Colton, attorney Loretta Bangor questioned the validity of affidavits submitted by Everhome’s attorney, a lawyer with Shapiro & Fishman, one of three firms under investigation by the Florida attorney general for “unfair and deceptive actions” in foreclosure cases. Judge Colton, one of two retired judges hired to handle foreclosures under the new state program, did not ask to see the documents. Nor did he question Shapiro & Fishman about the validity of the documents.

In 1989, Brian Hershkowitz developed the “Whole Loan Book Entry” concept while serving as a director for the Mortgage Bankers Association (MBA). In 1990, he first introduced this concept to seven different industry groups; Document Custodian, Originators, Servicers, Title Insurers, County Recorders, Government Sponsored Enterprises (GSE’s) and Warehouse/Interim Lenders. The reception was very positive and it was viewed as a very useful recording system to be used for how equity and debt securities could be identified and managed.

In 1991, Mr. Hershkowtiz published Farming It Out in Mortgage Banking Magazine. His main discussion in this article is primarily about getting the opinion of the experts in the technology outsourcing service industry. In 1992, Mr. Hershkowitz published another article called Cutting Edge Solutions in Mortgage Banking Magazine. In this particular article he mentions the actual meeting that took place at the Mortgage Bankers Association of America (MBA) headquarters with many key players that are known today as some of MERSCORP’s shareholders, such as, Fannie Mae and Freddie Mac. In this meeting they discussed a “System” that will bring changes in mortgage records.

Mr. Hershkowitz went on to become President and COO of LandSafe Credit, a leading settlement service provider that was a subsidiary of Countrywide. Mr. Hershkowitz also spent several years serving Countrywide in the areas of strategic planning and executive management.

In 2001, Mr. Hershkowitz became Executive Vice President at Fidelity National Information Services (FNIS) and President of its mortgage and information services division. His responsibilities included management of the Company’s data offerings, including public records information, credit reporting information, flood hazard compliance data, real estate tax information and collateral valuation services. He left FNIS in November of 2006 to become Chief Executive Officer of Maximum Value Group, a consulting firm focused on providing advice to private equity and other market participants in the area of banking and mortgages.

ENTER THE X-FILES

MERS has evolved into a totally different purpose today.

Mortgage Electronic Registration Systems, Inc. is a wholly owned subsidiary of MERSCORP Inc., located at 1595 Spring Hill Rd Ste 310 Vienna, VA 22182.

MERS was founded by the mortgage industry. MERS tracks “changes” in the ownership of the beneficial and servicing interests of mortgage loans as they are bought and sold among MERS members or others. Simultaneously, MERS acts as the “mortgagee” of record in a “nominee” capacity (a form of agency) for the beneficial owners of these loans.

To ensure widespread acceptance within the industry, MERS sought to have security instruments modified to contain MERS as the original mortgagee (MOM) language. MERS began to change decades of business practices after the two biggest mortgage funders in the U.S. the Federal Home Loan Mortgage Corporation (Freddie Mac) and the Ferderal National Mortgage Association (Fannie Mae) modified their Uniform Security Instruments to include MOM language. Their approval opened the doors to incorporate MERS into loans at origination.

Soon after, U.S. government agencies like the Veterans Administration, Federal Housing administration and Government National Mortgage Association (Ginne Mae), and several state housing agencies followed both Fannie/Freddie to approve MERS.

More than 60 percent of all newly-originated mortgages are registered in MERS. Its mission is to register every mortgage loan in the United States on the MERS System. Since 1997, more than 65 million home mortgages have been assigned a Mortgage Identification Number (MIN) and have been registered on the MERS System.

The mortgage-backed security (MBS) sector tested the viability of MERS because a substantial number of mortgages are securitized in the secondary market. In February 1999, Lehman Brothers was the first company to include MERS registered loans in a MBS.

Moody’s Investor Service issued an independent Structured Finance special report on MERS and it’s impact of MBS transactions and found that where the securitzer used MERS, new assignments of mortgages to the trustee of MBS transactions were not necessary.

Since MERS is a privately owned data system and not public, all mortgages and assignments must be recorded in order to perfect a lien. Since they failed to record assignments when these loans often traded ownership several times before any assignment was created, the legal issue is apparent. MERS may have destroyed the public land records by breaking the chain of title to millions of homes.

IN MERS CEO’S OWN WORDS

In or around the summer of 1997, MERSCORP President and CEO R.K. Arnold wrote, “Yes, There is life on MERS” Mr. Arnold stated, “Some county recorders have expressed concerns that MERS will eliminate their offices nationwide or destroy the public land records by breaking the chain of title. As implemented, MERS will not create a break in the chain of title, and, because MERS is premised on an assignment recorded in the public land records, MERS cannot work without county recorders.”

In this same article Mr. Arnold also states “The sheer volume of transfers between servicing companies and the resulting need to record assignments caused a heavy drag on the secondary market. Loan servicing can trade several times before even the first assignment in a chain is recorded, leaving the public land records clogged with unnecessary assignments. Sometimes these assignments are recorded in the wrong sequence, clouding title to the property”. Mr. Arnold never mentions the fact that the mortgage notes have been securitized, thereby becoming “negotiable securities” under the Uniform Commercial Code.

In an interview for The New York Times, Mr. Arnold said, “that his company had benefited not only banks, but also millions of borrowers who could not have obtained loans without the money-saving efficiencies MERS brought to the mortgage trade.”

Mr. Arnold went on to say that, ” far from posing a hurdle for homeowners, MERS had helped reduce mortgage fraud and imposed order on a sprawling industry where, in the past, lenders might have gone out of business and left no contact information for borrowers seeking assistance.”

“We’re not this big bad animal,” Mr. Arnold said. “This crisis that we’ve had in the mortgage business would have been a lot worse without MERS.”

Unfortunately, even a simple search in the Florida Land Records proves the opposite to be the case. Researchers have easily found affidavits of lost assignments actually stating, “the said mortgage was assigned to Mortgage Electronic Registration Systems, Inc., from “XXXXXXX”, the original of the said assignment to Mortgage Electronic Registration Systems, Inc., was lost, misplaced or destroyed before same could be placed of record with the Florida Land Records County Clerk’s office; That, “XXXXXXX”, it’s successors and/or assignee is no longer in business/or do not respond to our request for a duplicate assignment, and therefore, a duplicate original of said assignment cannot be obtained.”

According to affidavits such as these, not only have the borrowers lost contact with the lenders, but the same is true that MERS did as well.

Yet again, researchers have easily located affidavits recorded in the Florida Land Records stating “That said Deed of Trust has not been assigned to any other party and that MORTGAGE ELECTRONIC REGISTRATION SYSTEMS, Inc. is the current holder and owner of the Note and Deed of Trust in question.”

NO. THERE’S NO LIFE AT MERS

Aside from not recording assignments, Mr. Arnold failed to mention that the certifying officers given authority to execute sensitive loan documents would not be paid employees of MERS. This raises the critical legal question as to how one can act as a certified officer and execute any equitable interest on behalf of any security instruments without being an employee of MERS.

Q Do the assistant secretaries — first off, are

you a salaried employee of MERS?

A No.

Q Are you a salaried employee of MERS Corp,

Inc.?

A Yes.

Q Are any of the employees of MERS, Inc.

salaried employees?

A I don’t understand your question.

Q Does anyone get a paycheck, if they are an

employee of MERS, Inc., do they get a paycheck from

Mercer, Inc.?

A There is no MERS, Inc.

Q I thought, sir, there’s a company that was

formed January 1, 1999, Mortgage Electronic Registration

Systems, Inc. Does it have paid employees?

A No, it does not.

Q Does it have employees?

A No.

Q Does MERS have any employees?

A Did they ever have any? I couldn’t hear you.

Q Does MERS have any employees currently?

A No.

Q In the last five years has MERS had any

employees?

A No.

<SNIP>

Q How many assistant secretaries have you

appointed pursuant to the April 9, 1998 resolution; how

many assistant secretaries of MERS have you appointed?

A I don’t know that number.

Q Approximately?

A I wouldn’t even begin to be able to tell you

right now.

Q Is it in the thousands?

A Yes.

Q Have you been doing this all around the

country in every state in the country?

A Yes.

Q And all these officers I understand are unpaid

officers of MERS?

A Yes.

Q And there’s no live person who is an employee

of MERS that they report to, is that correct, who is an employee?

A There are no employees of MERS.

If so, how does anyone have any authority to sign security instruments encumbered by any loan documents, if these certifying officers are not paid employees and never attend corporate meetings in the capacity as Vice President, Assistant Secretary, etc. with Mortgage Electronic Registration System, Inc..

COURTS FIND ISSUES WITH MERS

Federal and state judges across America are realizing that the mortgage industry’s nominee is backfiring.

In Mr. Arnold’s own words, “For these servicing companies to perform their duties satisfactorily, the note and mortgage were bifurcated. The investor or its designee held the note and named the servicing company as mortgagee, a structure that became standard.” What has become a satisfactory standard structure for the mortgage industry has not been found by many courts to be legally sufficient to foreclose upon the property.

Again, MERS only acts as nominee for the mortgagee of record for any mortgage loan registered on the computer system MERS maintains, called the MERS System. MERS cannot negotiate a security instrument. Therefore, MERS certifying officers cannot have legal standing to assign what MERS does not own or hold.

The Supreme Court of New York Nassau County: Bank of New York Mellon V. Juan Mojica Index No: 26203/09

Justice Thomas A. Adams stated, “Not only has plaintiff failed to establish MERS’ right as a nominee for purposes of recording to assign the mortgage, more importantly, no effort has been made to establish the authority of MERS, a non-party to the note, to transfer its ownership.”

The Supreme Court of Maine: Mortgage Electronic Registration Systems, Inc. v. Saunders, No. 09-640, 2010 WL 3168374, (Me. August 12, 2010) The Court explains that the only rights conveyed to MERS in either the Saunders’ mortgage or the corresponding promissory note are bare legal title to the property for the sole purpose of recording the mortgage and the corresponding right to record the mortgage with the Registry of Deeds. This comports with the limited role of a nominee. A nominee is a “person designated to act in place of another, usu[ally] in a very limited way,” or a “party who holds bare legal title for the benefit of others or who receives and distributes funds for the benefit of others.” Black’s Law Dictionary 1149 (9th ed. 2009).

In Hawkins, No. BK-S-07-13593-LBR, 2009 WL 901766

The Court found that the deed of trust “attempts to name MERS as both beneficiary and a nominee” but held that MERS was not the beneficiary, as it had “no rights whatsoever to any payments, to any servicing rights, or to any of the properties secured by the loans.”

In Re: Walker, Case No. 10-21656-E-11– Eastern District of CA Bankruptcy court rules MERS has NO actionable interest in title. “Any attempt to transfer the beneficial interest of a trust deed without ownership of the underlying note is void under California law.” “MERS could not, as a matter of law, have transferred the note to Citibank from the original lender, Bayrock Mortgage Corp.” The Court’s ruled that MERS and Citibank are not the real parties in interest.

In re Vargas, 396 B.R. at 517-19. Judge Bufford found that the witness called to testify as to debt and default was incompetent. All the witness could testify was that he had looked at the MERS computerized records. The witness was unable to satisfy the requirements of the Federal Rules of Evidence, particularly Rule 803, as applied to computerized records in the Ninth Circuit. See id. at 517-20. “The low level employee could really only testify that the MERS screen shot he reviewed reflected a default. That really is not much in the way of evidence, and not nearly enough to get around the hearsay rule.”

FRAUD ON THE COURT

In US Bank v. Harpster the Law Offices Of David J. Stern committed fraud on the court by the evidence based on the Assignment of Mortgage that was created and notarized on December 5, 2007. However, that purported creation/notarization date was facially impossible: the stamp on the notary was dated May 19, 2012. Since Notary commissions only last four years in Florida (see F .S. Section 117.01 (l)), the notary stamp used on this instrument did not even exist until approximately five months after the purported date on the Assignment.

The Court specifically finds that the purported Assignment did not exist at the time of filing of this action; that the purported Assignment was subsequently created and the execution date and notarial date were fraudulently backdated, in a purposeful, intentional effort to mislead the Defendant and this Court. The Court rejects the Assignment and finds that is not entitled to introduction in evidence for any purpose. The Court finds that the Plaintiff does not have standing to bring its action.

The Court dismissed this case with prejudice.

In Duval County, Florida another foreclosure case was dismissed with prejudice for fraud on the court. In JPMorgan V. Pocopanni, the Court found that Fishman & Shapiro representing JPMorgan had actual knowledge at all times that the Complaint, the Assignment, and the Motion for Substitution were all false. The Court found that by clear and convincing evidence WAMU, Chase and Shapiro & Fishman committed fraud on this court.

Both these cases involved Mortgage Electronic Registration Systems Inc. assignments.

On August 10, 2010 Florida attorney general Bill McCollum announced that he is investigating three foreclosure law firms for allegedly providing fraudulent assignments and affidavits relating in foreclosure cases.

In a deposition taken in December 2009, GMAC employee Jeffrey Stephan said he signed 10,000 affidavits or similar documents a month without personally verifying who the mortgage holder was. That means many foreclosures could have taken place based on false documentation and many homes may have been unlawfully foreclosed on.

On September 20, 2010, GMAC halted foreclosures in 23 different states. Two of the three firms being investigated by the Florida attorney general, the Law Office of Marshall C. Watson and the Law Offices of David J. Stern PA, have represented GMAC in foreclosure proceedings.

This is not limited to only GMAC Mortgage. There are many hundreds of thousands of these same documents that are being created by many foreclosure law firms across the nation.

University of Utah law professor Christopher L. Peterson has raised the issue that MERS should be regarded as a debt collector. He argues that some of MERS’ methods are just the sort of deceptive practices that ought to be regulated under The Fair Debt Collection Practices Act (FDCPA), 15 U. S. C. §1692(a),(j).

CONCLUSION

Finally in May, 2009, Mr. Arnold said in Mortgage Technology Magazine, “Every system in the mortgage industry can switch MERS registry on or off at will,” referencing that both the Obama administration and Congressional leaders are aware of this.

President Obama and Congressional leaders it is time to permanently switch MERS lifeless device off!

Not until MERS became the primary focus for challenges to legal standing in foreclosure courts as reported by the alternative media, have the main stream media and the mortgage industry have begun to realize that property records cross the United States have become totally unreliable.

It has taken more than a decade for the courts to recognize that MERS has become a mortgage backfire system leaving clouded titles in over 65 million loans since 1997.

Courts across the nation must comply with the law. Any documents submitted to the courts regarding property ownership should be assumed to be nothing but smoke in a mirror.

Chief Justice Charles T. Canady

Florida Supreme Court

500 South Duval Street

Tallahassee, FL 32399-1900

Dear Chief Justice Canady,

I am disturbed by the increasing reports of predatory ‘foreclosure mills’ in Florida. The New York Times and Mother Jones have both recently reported on the rampant and widespread practices of document fraud and forgery involved in mortgage assignments. My staff has spoken with multiple foreclosure specialists and attorneys in Florida who confirm these reports.

Three foreclosure mills – the Law Offices of Marshall C. Watson, Shapiro & Fishman, and the Law Offices of David J. Stern – constitute roughly 80% of all foreclosure proceedings in the state of Florida. All are under investigation by Attorney General Bill McCollum. If the reports I am hearing are true, the illegal foreclosures taking place represent the largest seizure of private property ever attempted by banks and government entities. This is lawlessness.

I respectfully request that you abate all foreclosures involving these firms until the Attorney General of the state of Florida has finished his investigations of those firms for document fraud.

I have included a court order, in which Chase, WAMU, and Shapiro and Fishman are excoriated by a judge for document fraud on the court. In this case, Chase attempted to foreclose on a home, when the mortgage note was actually owned by Fannie Mae.

Taking someone’s home should not be done lightly. And it should certainly be done in accordance with the law.

For those who may not know both David J. Stern and Cheryl Samons both were former employees of Shapiro & Fishman prior to Mr. Stern and Mrs. Samons departing from Shapiro & Fishman…“thats all“. <grin>————————–>

180 PAGES!

PROTECTIVE ORDER? Lender Processing Services? Specialized Loan Servicing? American Home Mortgage Servicing? DEPOS? SUBPOENAS?

DISMISSAL WITH PREJUDICE!

Florida Rules of Civil Procedure

1.420 Dismissal of Actions

(a) Voluntary Dismissal.

(1) By Parties. Except in actions in which property has been seized or is in the custody of the court, an action may be dismissed by plaintiff without order of court

(B) by filing a stipulation of dismissal signed by all parties who have appeared in the action. Unless otherwise stated in the notice or stipulation, the dismissal is without prejudice, except that a notice of dismissal operates as an adjudication on the merits when served by a plaintiff who has once dismissed in any court an action based on or including the same claim.

In 2006 MERS released a mortgage belonging to the Velez’s. MERS Vice President name is Merhl Gibson and the notary is Jane Eyler. Both from Maryland. It appears that the same individual signed the entire document. See exhibit below.

Now these same individuals are signing this document below as Vice President and Notary for CitiMortgage. But take a close look and compare the signatures to the release above.Both of these are about a few weeks apart. Merhl’s stamp is from New York.

“On 8/30, I had a Summary Judgment Foreclosure hearing on Palm Beach County’s “Rocket Docket”. The judge spoke for 14 minutes to the crowd, of mostly pro se defendants, about how they should just agree to the summary judgment and the plaintiffs, (whose attorneys (Shapiro & Fishman had a dedicated courtroom and to whom he referred to as “my attorneys”) would be gracious (Ha!) enough to allow them to stay in their homes for 120 days if needed (even though the statute says he only has to give them 30). When it came to hearing arguments which were fully briefed and provided to the court (pursuant to the instructions of the Divisions head judge) he only allowed 30-60 seconds for argument, failed to read any of the papers, failed to review the plaintiff’s foreclosure package,flatly ignored the Affidavit filed in Opposition, ignored my plea for a trial, signed the judgment and dismissed me. I never was permitted to even read the proposed judgment or to examine the “newly discovered” allonge which Shapiro’s counsel said I had no right to see. Thank God I had a court reporter!”

Well it just happens to be that Lori is an Attorney and got a transcript of what went down…

Pew family trusts which I am a beneficiary and/or remainderman have maintained

investments in various banks, mutual funds, and other entities that maintain

interests in various shares, mortgage backed securities and/or debt issuances and I

have been a shareholder in many mortgage companies including Fannie Mae,

Bear Stearns, JPMorganChase, Washington Mutual, MGIC, Ocwen and Radian,

many of which are members, owners and shareholders in Mortgage Electronic

Registration Systems, Inc. [MERS].

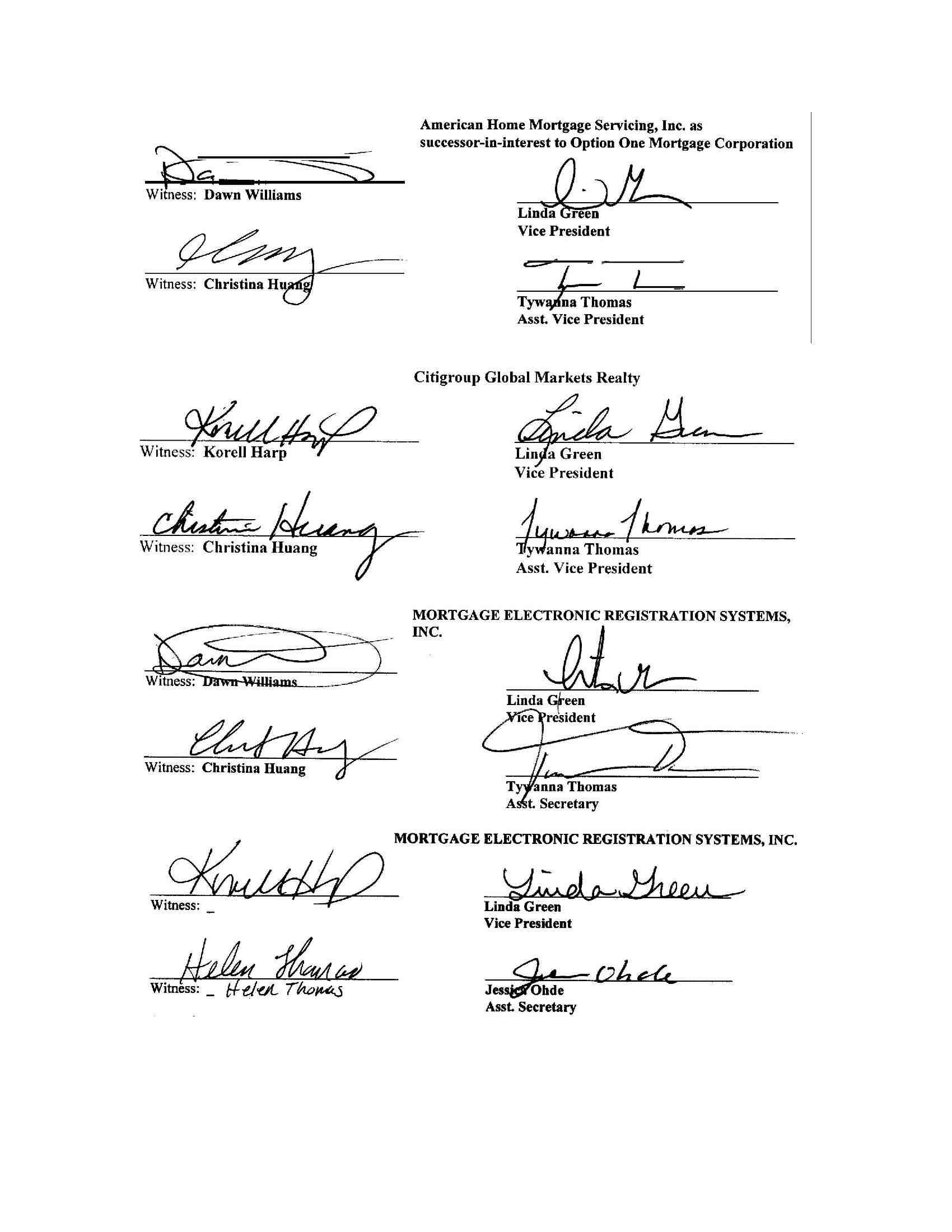

Linda Green

Lender Processing Services

Shapiro & Fishman

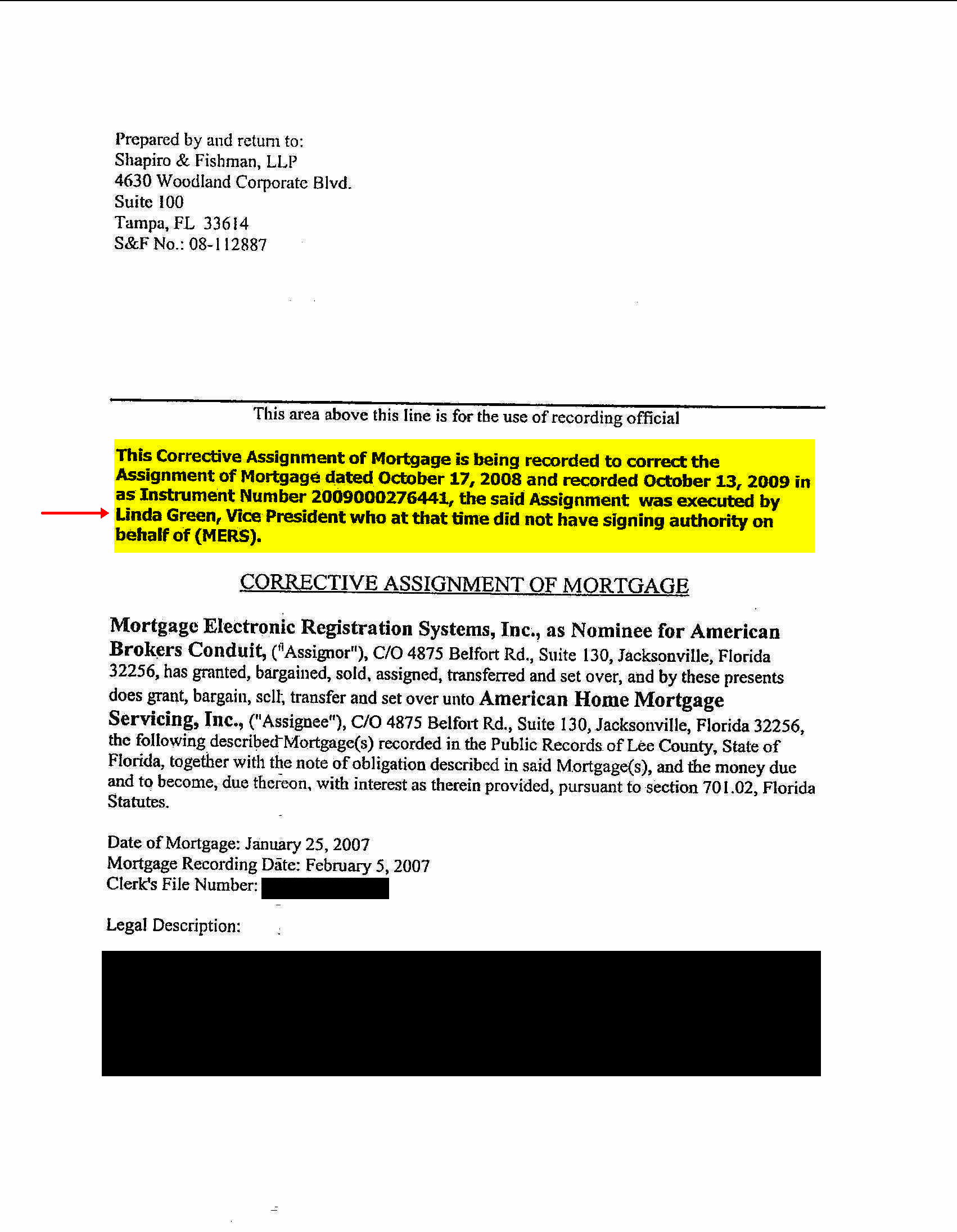

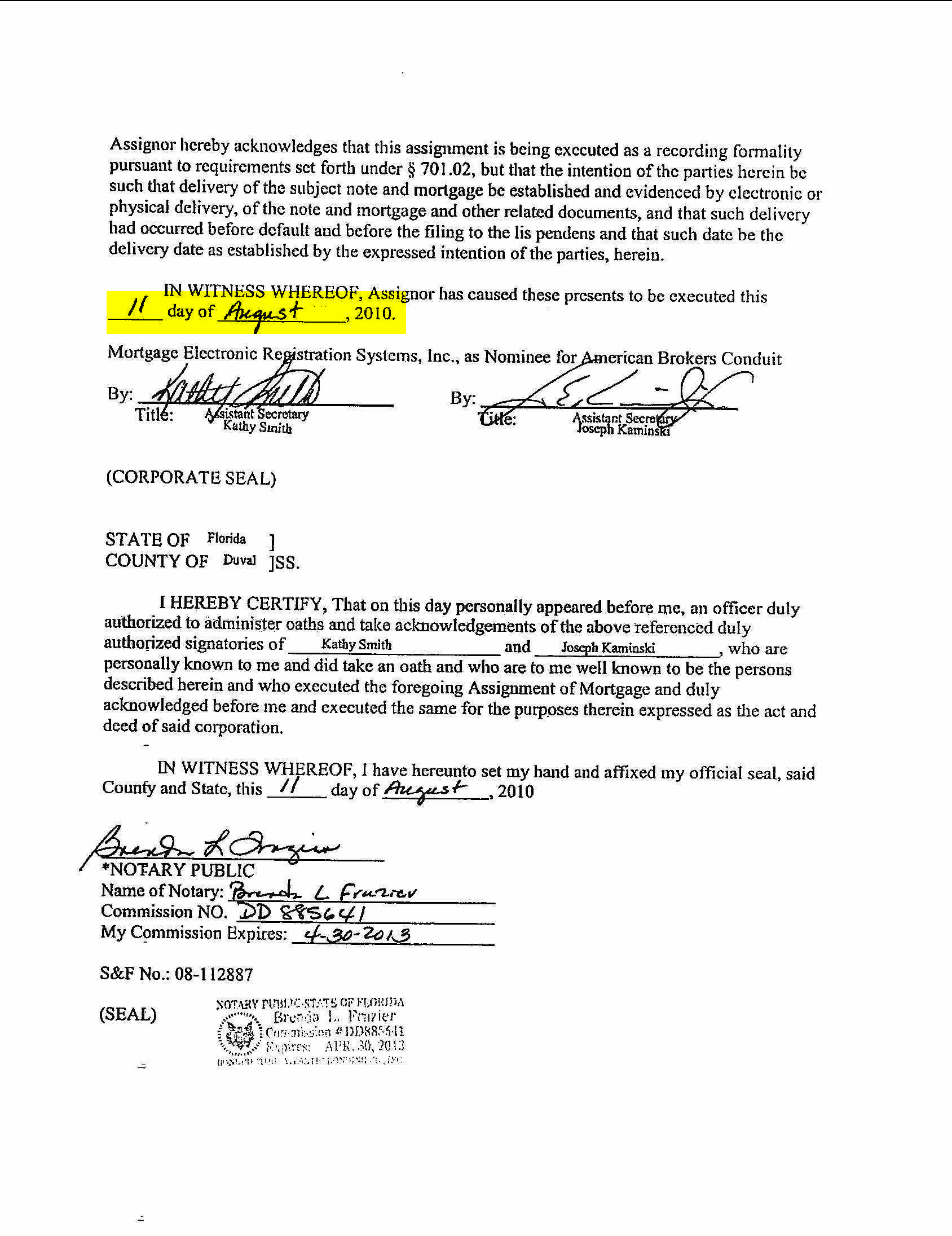

Action Date: August 26, 2010 Location: Fort Lauderdale, FL

On August 11, 2010, the Florida foreclosure mill law firm of Shapiro & Fishman (S&F) filed a “corrective” mortgage assignment (copy available in the “Pleadings” section herein). According to S & F, this “corrective” assignment was necessary because previous assignments filed by S & F were signed by Linda Green “who at that time did not have signing authority on behalf of MERS.” The day before, on August 10, 2010, the Florida Attorney General’s office issued a press release identifying S & F as one of the Florida law firms under investigation for unfair & deceptive trade practices involving improper documentation used to speed foreclosure proceedings. When Linda Green signed the prior assignments as a MERS officer, she was actually employed by Lender Processing Services in its Alpharetta, Georgia offices. Lender Processing Services decides which law firms get assigned foreclosure cases by the banks in hundreds of thousands of cases. Lender Processing Services hires the law firms and provides these firms with the documents they might need – using its own employees to sign the documents – without authority from MERS. The “corrective” assignment was signed by Kathy Smith and Joseph Kaminski who were identified as Assistant Secretaries of MERS, as nominee for American Brokers Conduit ( a company in bankruptcy since 2007). Smith & Kaminski are not actually employed by MERS or by American Brokers Conduit – so S&H may need another “corrective assignment.” The original assignment was dated October 17, 2008 – over two weeks AFTER the Lis Pendens was filed, but the “corrective” assignment attempts to solve the obvious lack of standing by a provision that states that the actual delivery of the documents took place on an unspecified date “and that such delivery of documents had occurred before default and before the filing to the lis pendens…” Courts and homeowners can expect a few more corrections from Shapiro & Fishman.

Today an article was released about the the foreclosure mills moving forward to quash the subpoenas served upon them by the Florida Attorney General. In this article there was a tad bit of heresay going on…

One of the firms is represented by WPB attorney Gerry Richman:

The subpoena has had a chilling effect on clients and has led to defense lawyers citing the investigation in motions to have the Shapiro firm disqualified from cases. One judge, according to the petition, has said in open court he will deny all summary judgment motions filed by the law firms named by the attorney general based solely on the existence of the investigation. In an interview, attorney Gerald Richman, who is representing the Shapiro firm, said he did not know who the judge is. He denied the Shapiro firm falsified any documents.

“One of our concerns is the broad brush,” he said. “We are not in the category with David Stern, we are not in the category with any other law firm. Hopefully we will not lose clients. We’re doing whatever we can to fight back.”

Ok, well how can anyone make such a statement without clarifying who the judge is? This is clear speculation!

The Attorney General’s office is fighting back stating the facts…

McCollum spokeswoman Sandi Copes responded, “our office is responsible for protecting consumers year-round, and this investigation has been ongoing for some time.”

Last is information requesting from David J. Stern regarding the subpoena from the AG…

“This request would include entities that have nothing to do with the Law Firm’s legal practice, e.g., if David J. Stern owns a piece of real estate in an entity or he has trusts set up for his family,” according to the petition filed by Stern’s attorney, Jeffrey Tew of Miami. “This request should be narrowed to include entities that have a connection with his legal practice.”

This is quite a fight! Listen this is exactly what is happening across the country. When and Who is going to pick up this mess when it all finally comes to reality?

In my Florida Bar Complaint I raised this same issue against my MILL and they saw nothing wrong??…Again, we are on our own to bring them down!

(1) Citimortgage admits its own employees signed an assignment of mortgage, conveying a mortgage to itself.

(2) Foreclosure Mill Shapiro & Fishman, LLP admits its standard practice is to prepare these assignments for their own clients (not the original mortgagee) to execute and record in the public record.

(3) Shapiro never runs conflict checks prior to filing new lawsuits, leaving it up to their other clients (who may or may not be named as Defendants) to assert a conflict after the case has been filed.

These admissions were made in the course of a 3.5 hour, evidentiary hearing on a Motion to Disqualify Counsel brought by Mark Stopa on June 18, 2010 before Judge Foster in Tampa.

I’ve attached the Transcript, DQ Motion, and the Exhibits introduced into evidence, but they’re not going to make sense without some background. (Bear with me, this is fascinating stuff. To illustrate, even as he denied the motion (incorrectly, in my opinion), Judge Foster openly acknowledged the need for a written opinion from the Florida Supreme Court, comparing the issue to Gideon v. Wainwright, 372 U.S. 335 (1963) and Miranda v. Arizona, 384 U.S. 436 (1966)).

Facts (as set forth in DQ Motion,Transcript, and Exhibits): Shapiro & Fishman represents Citimortgage, Inc. in a foreclosure lawsuit against JPMorgan, MERS, and the homeowners. The Complaint does not specify how Citimortgage acquired standing to foreclose. The public records reflect an Assignment of Mortgage, prepared by Shapiro, purporting to assign the mortgage from MERS, as Nominee for First Security Mortgage Services, to Citimortgage. The assignment was executed the same day Citimortgage filed suit. Citimortgage’s own employee testified that Nate Blackstun and Jamie Hardcastle, the individuals who signed this assignment (purporting to transfer the mortgage from MERS to Citimortgage) are actually employees of Citimortgage. Quoting the testimony of a Citimortgage employee:

Q: Who is Jamie Hardcastle?

A: She works at Citimortgage in the — well, I’m not quite sure which department she works in.

Q: Do you know her?

A: Yes.

Q: Do you work with her?

A: No, she works in my building.

Q: She’s an employee of Citimortgage, Inc.?

A: Yes.

Q: How about Nate Blackstun? Do you know him?

A: Yes.

Q: Who is he?

A: He’s vice president of Citimortgage.

Q: Does he work in your building as well?

A: Yes. …

Q: Do you know whether Mr. Blackstun obtained the consent of MERS prior to signing an assignment of mortgage in this case?

A: He’s an authorized signer for MERS.

Q: Even though he’s also the Vice President of Citimortgage?

A: Yes.

Q: You see any sort of problem with that?

A: No.

Q: How do you allege that Citimortgage became the owner and holder of this note in this case?

A: It was assigned to Citimortgage –

Q: From whom?

A: from MERS.

Q: From whom?

A: MERS.

Q: On behalf of whom?

A: I’m not sure.

In fact, Shapiro and Fishman’s office manager admitted that Shapiro’s standard practice is to prepare an Assignment of Mortgage, provide it to its own client to sign (on behalf of the original mortgage holder, typically MERS), have its client execute the assignment, and cause the assignment to be recorded.

Q: Do you dispute that Jamie Hardcastle is an employee of Citimortgage, Inc.?

A: Do I dispute that? No.

Q: Do you dispute that Nate Blackstun is an employee of Citimortgage, Inc.?

A: No.

Q: Yet they are the individuals who signed an assignment of mortgage on October 13, 2009, purporting to convey a mortgage from Mortgage Electronic Registration Systems, Inc. as nominee for First Security Mortgage Services to Citimortgage?

A: With authority from MERS to execute the document, yes they did. …

Q: So all you basically do when you get a new client for a foreclosure case, you cause an assignment of mortgage to be prepared, send it to your client for signature, and knowing that your clients have it own employees signing it and then sending it back to you, true?

A: Yes. However, that assignment is not part of the foreclosure action itself. It’s a chain of title document which is not part of the foreclosure.

Q: You’ve never seen these assignments of mortgage be attached to a complaint?

A: Sure.

Shapiro represents JPMorgan and MERS in other, pending cases, including at least one case where MERS is adverse to Citimortgage. Yet Shapiro continues to represent Citimortgage in this case, adverse to JPMorgan and MERS. (If you don’t think there is anything wrong with that, call The Florida Bar and tell them you represent ABC Corp. against XYZ Corp. and ask The Bar if it’s ok for you to represent XYZ Corp. against ABC Corp. – see what they say. See if the Bar gives its blessing, even if both entities waive the conflict.) Shapiro did not perform a “conflict check” prior to representing Citimortgage in this case and, in fact, does not perform conflict checks when taking on new files. Instead, Shapiro’s standard practice is to file the suit for whichever bank it is representing in that case and presume there is no conflict unless a different bank asserts such a conflict.

The issues: (a) Whether Shapiro & Fishman have a conflict of interest under 4-1.7, R.Reg.Fla.Bar, precluding it from acting as counsel for Citimortgage, when it is simultaneously representing JPMorgan and MERS (in other, pending cases and, arguably, the instant case); and (b) whether Citimortgage has used Shapiro’s services to perpetrate a crime or fraud, without agreeing to disclose and rectify the crime or fraud, in violation of 4-1.16, R.Reg.Fla.Bar.

The law: Rule 4-1.7(a) precludes a law firm from representing a client if the representation is (1) directly adverse to another client; or (2) there is a substantial risk that the lawyer’s representation will be “materially limited” by the lawyer’s responsibilities to another client, a former client, a third person, or a personal interest of the lawyer. The only way around this prohibition is compliance with 4-1.7(b), which requires, among other things, that each client gives informed consent, confirmed in writing or clearly stated on the record at a hearing. See Lincoln Associates & Constr., Inc. v. Wentworth Constr. Co., Inc., 26 So. 3d 638 (Fla. 1st DCA 2010). Additionally, Rule 4-1.16 precludes a lawyer from representing a client who has used the lawyer’s services to commit a crime or fraud unless the client agrees to disclose and rectify the crime or fraud.

Analysis: In the face of the Motion to Disqualify Counsel, Shapiro presented a waiver of conflict, signed by an employee of Citimortgage, dated just one day before the hearing (the first time Shapiro discussed the issue of conflict with Citimortgage). However, Shapiro presented no such waiver from MERS or JPMorgan, and no witness from MERS or JPMorgan testified or otherwise consented to waive the conflict. In my opinion, the absence of consent from MERS and JPMorgan required Shapiro’s disqualification. See Rule 4-1.7 and Wentworth.

Throughout the hearing, Judge Foster repeatedly ruled that he “did not see the conflict” and that Citimortgage was “not adverse” to MERS and JPMorgan. Respectfully, when these entities are on opposite sides of a lawsuit, the adversity is presumed. They are adverse by definition, one being the Plaintiff and the other the Defendant. Although Shapiro contends, when these entities are named as Defendants, that it’s merely to ”clear title,” that does not change the adversarial nature of the relationship. For instance, suppose MERS or JPMorgan or First Security later realized it was the owner and holder of the note and mortgage (or, at minimum, that it had a bona fide claim in that regard) – the judgment in this case would bar such a claim under principles of res judicata and collateral estoppel. Similarly, suppose a ”junior” lien holder had a bona fide argument that its lien was superior. Isn’t Shapiro throwing one client under the bus (the defendant) for the sake of another (the plaintiff) without checking if its own client, the defendant, takes the position that it owns and holds the note and mortgage? Shapiro says the defendant was defaulted, so it isn’t contesting the plaintiff’s position and there is hence no conflict, but isn’t it the lawyer’s job to inquire about the conflict, before filing suit, and not merely to leave it up to the client to figure it out? Isn’t it Shapiro’s responsibility, under The Rules Regulating The Florida Bar, before filing suit against its own client, to make sure that the client it is suing consents to the relief being requested? How do we know the client isn’t relying on the law firm (as clients reasonably do)? I can see the logic now – “Shapiro is filing suit against us for a different bank. Shapiro represents us. Shapiro must be right – we must not have an ownership interest in this Note and Mortgage.” We’ve already established that Shapiro isn’t checking – Shapiro admitted as much at this hearing – so if the bank isn’t checking, either, then who is?

Suppose this were any other setting, not a foreclosure case, and you represent ABC Corp. against XYZ Corp. Would you ever file suit for XYZ Corp. against ABC Corp., in a different suit, without asking ABC Corp. if it consented? Without asking ABC Corp. if it agreed with XYZ Corp’s position in that case? I highly doubt it. So why it is okay for Shapiro to do that in these cases, over and over again? Merely because they are foreclosure cases?

And what about all of the cases where Shapiro’s “other” client may claim ownership of the Note and Mortgage (e.g. because it is the record owner or prior record owner) but is not named as a defendant in the suit? Why does Shapiro name these entities as Defendants in some cases but not in others? If they need to “clear title” in some cases, why not in others? Is Shapiro intentionally not naming its own client as a defendant to make it easier for its other client, the plaintiff, to win the foreclosure case, while leaving the door open for its other client (not named as a defendant) to file suit on the same Note andMortgage? After all, if the bank isn’t named as a defendant, the foreclosure judgment is not binding on it, and nothing stops that bank from filing a different lawsuit for foreclosure.

Meanwhile, in the face of an assignment of mortgage that appears fraudulent (unless you think self-dealing or dual agency is okay), Shapiro asserts Citimortgage’s standing is based on transfer of the note, not the assignment of mortgage. Of course, Shapiro did not take this position until after the Motion to Disqualify Counsel was filed, which raises the question – why is Shapiro so willing to concede one ground for standing in this case when it asserts that basis for standing in other, similar cases? We all know there are many cases in which Shapiro has used an assignment of mortgage as a basis for standing; in fact,often the assignment is attached to the Complaint. Why, then, would it be giving up this argument in this case? In my opinion, the answer is clear – Shapiro wants to take the spotlight off of itself and its own conduct, even if it means giving up an argument for a client. “Let’s argue the assignment is irrelevant for purposes of standing, that way our conduct vis a vis the assignment becomes irrelevant, too.” Maybe standing is, in any given case, based on transfer of the Note. Respectfully, though, wouldn’t a conflict-free attorney want to argue every possible basis for standing, including the assignment, and not forego an argument for standing because it highlighted that attorney’s own conduct? In other words, isn’t Shapiro’s representation of Citimortgage “materially limited” by its own self-interest? See Rule 4-1.7(a)(2). Notably, upon inquiry from Mr. Stopa, the Citimortgage employee made it clear Shapiro never advised her that it was giving up one basis for standing in the case. Respectfully, how can a waiver be “informed’ when Citimortgage does not understand the ramifications of its waiver in the pending case?

Unfortunately, Judge Foster did not seem to get (for lack of a better term) this latter argument, as he sustained an objection that Shapiro’s reliance on an assignment in other cases was irrelevant. (That’s one purpose of a blog like this – to make judges think about these issues and understand them. To wit, by no means am I trying to criticize Judge Foster here – I respect and appreciate that he gave me the opportunity to flesh out this evidence. I just think the issues merit consideration from all of us.) But Shapiro’s reliance on the assignments in other cases – and refusal to do so in this case – is precisely the point. If Shapiro is relying on assignments in other cases, but not in this case, merely to take the spotlight off of itself so as to defeat a motion to disqualify, it’s representation is materially limited by its own self-interest, in violation of 4-1.7. Remember, the rule requires “informed” consent, and if Citimortgage is consenting to the representation without understanding that Shapiro is waiving an argument that a conflict-free attorney would assert, the consent is not “informed.” Also, how many hundreds or thousands of times has Shapiro relied on these assignments in other foreclosure cases (in which I, or another defense attorney, am not involved)?

Meanwhile, Judge Foster seemed to accept that a fraud was not being committed upon the Court (given how Shapiro distanced itself from the assignment of mortgage), but Rule 4-1.16 doesn’t require that the fraud be committed in that case. The Rule requires that a lawyer withdraw from representation if “the client has used the lawyer’s services to perpetrate a crime or fraud, unless the client agrees to disclose and rectify the crime or fraud.” Here, isn’t an assignment of mortgage, filed in the public records, purporting to convey an assignment from MERS to Citimortgage, but which is actually signed by employees of Citimortgage, a fraud? As I’ve presented this argument, judges seem to be taking the position that it’s OK for an employee of Citimortgage to execute an assignment from MERS to itself as long as MERS consents, but how is that not self-dealing? And why is it ok? I know I’m not the only person who thinks it’s wrong. See HSBC Bank USA, N.A. v. Vazquez, 2009 N.Y. Slip Op. 51814 (N.Y. 2009); Bank of New York v. Mulligan, 2008 N.Y. Slip. Op 31501 (N.Y. 2008) (“The Court is concerned that Mr. Harless might be engaged in a subterfuge, wearing various corporate hats. Before granting an application for an order of reference, the Court requires an affidavit from Mr. Harless describing his employment history for the past three years.”); Bank of New York v. Orosco, 2007 N.Y. Slip Op 33818 (N.Y. 2007); Deutsche Bank Nat’l Trust Co. v. Castellanos, 2008 N.Y. Slip. Op. 50033 (N.Y. 2008) (“Did Mr. Rivas somehow change employers on July 21, 2006 or is he concurrently a Vice President of both assignor Argent Mortgage Company, LLC and assignee Deutsche Bank? If he is a Vice President of both the assignor and the assignee, this would create a conflict of interest and render the July 21, 2006 assignment void. … The court is concerned that there may be fraud on the part of Deutsche Bank, Argent Mortgage Company, LLC, and/or MTGLQ Investors, L.P., or at least malfeasance.”).

In comments made as the hearing began (which are unfortunately not in the transcript), Judge Foster made it clear that he didn’t want to require disqualification and upset the entire banking industry. In a way, that’s exactly what this motion is doing – arguing that the manner in which these assignments have been completed (and, in essence, the entire MERS system) is a fraud. Respectfully, though, why should the fact that the fraud is pervasive – and would upset the way banks litigate foreclosure cases – make this problem less worthy of attention? Shouldn’t the fact that these assignments are being prepared fraudulently in virtually every case make judges more likely to fix the problem, not less?

Shapiro argued extensively that my clients lack standing to argue this issue. However, the Comment to 4-1.7 provides: “Where the conflict is such as clearly to call into question the fair or efficient administration of justice, opposing counsel may properly raise the question.” This is where we need to educate judges about the widespread ramifications of “pushing through” foreclosure cases. For instance, in these cases where the wrong Plaintiff is suing, what will happen when the actual owner of the Note and Mortgage emerges, after the foreclosure is granted? What will happen to the homeowner, who has already been foreclosed upon by the wrong bank (but faces another lawsuit by the correct one)? What will happen to the then-owner of the property, who purchased the property either at the courthouse auction or from such a purchaser? What about the title company that issued title insurance based on that sale? Particularly in lawsuits where the Note is lost, or where the original mortgage holder went into bankruptcy (and subsequent transfers or assignments were unauthorized as a matter of law) we must safeguard against these problems. That’s why addressing these conflict issues is so important – it forces banks and their lawyers to take a hard look at the interests of all parties involved before a foreclosure case gets “pushed through.”

Many Florida cases on the issue of disqualification talk about the appearance of impropriety and the public’s perception of our conduct as lawyers. See Wentworth, Campbell v. American Pioneer Savings Bank, 565 So. 2d 417 (Fla. 4th DCA 1990); Andrews v. Allstate Ins. Co., 366 So. 2d 462 (Fla. 4th DCA 1978). For the life of me, I can’t see how anyone can dispute the unseemliness of these events. Perhaps that’s why at least one judge has questioned the conflict of interest in these situations. See HSBC Bank USA, N.C. v. Vazquez, 2009 N.Y. Slip. Op 51814 (N.Y. 2009) (“Even if Plaintiff HSBC is able to cure the assignment defect, plaintiff’s counsel then has to adderess the conflict of interest that exists with his representation of both the assignor of the instant mortgage, MERS as Nominee for HSCB Mortgage, and the assignee of the instant mortgage, HSBC.”). I urge more attorneys and judges in our great state to give careful consideration to these issues.

fannie mae owned.bank property. property is vacant.all offers requiring financing must have preapproval letter.all cash offer require proof of fund(see attachement).this property is eligible for home path renovation mortgage-as little as 3% down.buyer must close with seller closing agent(david j. stern law offices,p.a).investors not eligible for first 15days.*for showing instr please read broker remarks* note:offers must be submitted using attachment.close by 30 june and receive extra 3.5% in closing cost

Looking further into this I noticed the following:

Still in the name of the owner

NOT named under any REO

Home last sold for 245K

Now listed at 120K

Here is the BIGGEST:

I found a Bank-owned packet for this “SPECIALLY SELECTED” Agent/BROKER in many other REO’s and in this package it states the following: (SEE ABOVE LINK PACKET)

9) Which title companies are the sellers and who do I make out the earnest money deposit to once offer is verbally accepted?

a. PLEASE LOOK ON MLX REMARKS FOR TITLE COMPANY. MLX WILL HAVE ONE OF THE FOLLOWING:

HERE IS same Agent/Broker for a FLORIDA DEFAULT LAW GROUP property:

THIS IS FANNIE MAE HOMEPATH PROPERTY.BANK OWNED.ALL OFFERS REQUIRING FINANCING MUST HAVE PREAPPROVAL LETTER. ALL CASH OFFERS REQUIRE PROOF OF FUNDS. THIS PROPERTY IS APPROVED FOR HOMEPATH AND HOMEPATH RENOVATION MORTGAGE FINANCING-AS LITTLE AS 3% DOWN,NO APPRAISAL OR MORTGAGE INSURANCE REQUIRED! ** FOR SHOWING INST PLEASE READ BROKER REMARKS** YOU MUST SUBMIT OFFER USING ATTACHMENT! INVESTORS NOT ELIGIBLE FOR FIRST 15DAYS.CLOSE BY JUNE 30 TO BE ELIGIBLE FOR EXTRA 3.5% SC.EMD: FL DEFAULT LAW GROUP.

Here is another same Agent/Broker forMARSHALL C. WATSON property:

FANNIE MAE OWNED.BANK PROPERTY. PROPERTY IS VACANT.ALL OFFERS REQUIRING FINANCING MUST HAVE PREAPPROVAL LETTER.ALL CASH OFFERS REQUIRE PROOF OF FUNDS(SEE ATTACHEMENT).THIS PROPERTY IS ELIGIBLE FOR HOME PATH RENOVATION MORTGAGE-AS LITTLE AS 3% DOWN.BUYER MUST CLOSE WITH SELLER CLOSING AGENT (LAW OFFICES OF MARSHALL C. WATSON).INVESTOR NOT ELIGIBLE FOR FIRST 15DAYS.*FOR SHOWING INSTR PLEASE READ BROKER REMARK* NOTE:OFFERS MUST BE SUBMITTED USING ATTACHMENT.CLOSE BY JUNE 30 TO GET 3.5% EXTRA IN CLOSING COST

Does the JUNE 30th Closing Day have any significance??

What “if” the BUYER selects their own Title company? Does this eliminate their chances of ever even being considered as a buyer?

Why even bother to state this?

Is this a way for the selected Agent/ Broker to find the buyer and discourage other agents or buyers from viewing?

Was this at all even necessary to state?

Is this verbiage to coerce agents to get a higher commission rather than pass down the incentive of 3.5% towards closing cost “if” under contract by 6/30?

Why do investors have to refrain from buying for the first 15 days?

Coercion (pronounced /ko???r??n/) is the practice of forcing another party to behave in an involuntary manner (whether through action or inaction) by use of threats, intimidation, trickery, or some other form of pressure or force. Such actions are used as leverage, to force the victim to act in the desired way. Coercion may involve the actual infliction of physical pain/injury or psychological harm in order to enhance the credibility of a threat. The threat of further harm may lead to the cooperation or obedience of the person being coerced. Torture is one of the most extreme examples of coercion i.e. severe pain is inflicted until the victim provides the desired information.

")

{kind=link}

{kind=link}

{kind=link}

Recent Comments