The Massachusetts Supreme Court on Friday upheld a lower court ruling voiding two foreclosures because the banks failed to show the proper paperwork to prove they owned the loans-a decision that challenges the way mortgages were bundled and sold around the world.

Shares of Wells Fargo and U.S. Bancorp–the banks involved in the case–as well as those of other banks fell following the announcement of the decision. Wells Fargo was down 3.4 percent and US Bancorp 1.1 percent at midday.

The Massachusetts court is the highest to ruled on this issue and the decision has the potential to invalidate thousands of foreclosures across the state. It also provides more ammunition to borrowers in other states who could push the case to the U.S. Supreme Court. If the nation’s highest court rules that these transfers are not legal, the multi-trillion-dollar mortgage-backed securitization industry could face massive liability.

U.S. Bancorp and Wells Fargo & Co. lost a foreclosure case in Massachusetts’s highest court that will guide lower courts in that state and may influence others in the clash between bank practices and state real-estate law. The ruling drove down bank stocks.

The state Supreme Judicial Court today upheld a judge’s decision saying two foreclosures were invalid because the banks didn’t prove they owned the mortgages, which he said were transferred into two mortgage-backed trusts without the recipients’ being named.

Joshua Rosner, an analyst at the New York-based research firm Graham Fisher & Co., called the decision “a landmark ruling” showing that at least in Massachusetts a mortgage “must name the assignee to be valid.”

“This is likely to open the floodgates to more suits in Massachusetts and strengthens cases in other states,” Rosner said.

“We agree with the judge that the plaintiffs, who were not the original mortgagees, failed to make the required showing that they were the holders of the mortgages at the time of foreclosure,” Justice Ralph D. Gants wrote for a unanimous court.

NOTICE: All slip opinions and orders are subject to formal revision and are superseded by the advance sheets and bound volumes of the Official Reports. If you find a typographical error or other formal error, please notify the Reporter of Decisions, Supreme Judicial Court, John Adams Courthouse, 1 Pemberton Square, Suite 2500, Boston, MA 02108-1750; (617) 557-1030 (617) 557-1030

SJCReporter@sjc.state.ma.us

SJC-10694

U.S. BANK NATIONAL ASSOCIATION, trustee1 vs. ANTONIO IBANEZ (and a consolidated case2,3).

Real Property, Mortgage, Ownership, Record title. Mortgage, Real estate, Foreclosure, Assignment. Notice, Foreclosure of mortgage.

Civil actions commenced in the Land Court Department on September 16 and October 30, 2008.

Motions for entry of default judgment and to vacate judgment were heard by Keith C. Long, J.

The Supreme Judicial Court granted an application for direct appellate review.

R. Bruce Allensworth (Phoebe S. Winder & Robert W. Sparkes, III, with him) for U.S. Bank National Association & another.

Paul R. Collier, III (Max W. Weinstein with him) for Antonio Ibanez.

Glenn F. Russell, Jr., for Mark A. LaRace & another.

The following submitted briefs for amici curiae:

Martha Coakley, Attorney General, & John M. Stephan, Assistant Attorney General, for the Commonwealth.

Kevin Costello, Gary Klein, Shennan Kavanagh & Stuart Rossman for National Consumer Law Center & others.

Ward P. Graham & Robert J. Moriarty, Jr., for Real Estate Bar Association for Massachusetts, Inc.

Marie McDonnell, pro se.

GANTS, J. After foreclosing on two properties and purchasing the properties back at the foreclosure sales, U.S. Bank National Association (U.S. Bank), as trustee for the Structured Asset Securities Corporation Mortgage Pass-Through Certificates, Series 2006-Z; and Wells Fargo Bank, N.A. (Wells Fargo), as trustee for ABFC 2005-OPT 1 Trust, ABFC Asset Backed Certificates, Series 2005-OPT 1 (plaintiffs) filed separate complaints in the Land Court asking a judge to declare that they held clear title to the properties in fee simple. We agree with the judge that the plaintiffs, who were not the original mortgagees, failed to make the required showing that they were the holders of the mortgages at the time of foreclosure. As a result, they did not demonstrate that the foreclosure sales were valid to convey title to the subject properties, and their requests for a declaration of clear title were properly denied.5

Procedural history. On July 5, 2007, U.S. Bank, as trustee, foreclosed on the mortgage of Antonio Ibanez, and purchased the Ibanez property at the foreclosure sale. On the same day, Wells Fargo, as trustee, foreclosed on the mortgage of Mark and Tammy LaRace, and purchased the LaRace property at that foreclosure sale.

In September and October of 2008, U.S. Bank and Wells Fargo brought separate actions in the Land Court under G. L. c. 240, § 6, which authorizes actions “to quiet or establish the title to land situated in the commonwealth or to remove a cloud from the title thereto.” The two complaints sought identical relief: (1) a judgment that the right, title, and interest of the mortgagor (Ibanez or the LaRaces) in the property was extinguished by the foreclosure; (2) a declaration that there was no cloud on title arising from publication of the notice of sale in the Boston Globe; and (3) a declaration that title was vested in the plaintiff trustee in fee simple. U.S. Bank and Wells Fargo each asserted in its complaint that it had become the holder of the respective mortgage through an assignment made after the foreclosure sale.

In both cases, the mortgagors — Ibanez and the LaRaces — did not initially answer the complaints, and the plaintiffs moved for entry of default judgment. In their motions for entry of default judgment, the plaintiffs addressed two issues: (1) whether the Boston Globe, in which the required notices of the foreclosure sales were published, is a newspaper of “general circulation” in Springfield, the town where the foreclosed properties lay. See G. L. c. 244, § 14 (requiring publication every week for three weeks in newspaper published in town where foreclosed property lies, or of general circulation in that town); and (2) whether the plaintiffs were legally entitled to foreclose on the properties where the assignments of the mortgages to the plaintiffs were neither executed nor recorded in the registry of deeds until after the foreclosure sales.6 The two cases were heard together by the Land Court, along with a third case that raised the same issues.

On March 26, 2009, judgment was entered against the plaintiffs. The judge ruled that the foreclosure sales were invalid because, in violation of G. L. c. 244, § 14, the notices of the foreclosure sales named U.S. Bank (in the Ibanez foreclosure) and Wells Fargo (in the LaRace foreclosure) as the mortgage holders where they had not yet been assigned the mortgages.7 The judge found, based on each plaintiff’s assertions in its complaint, that the plaintiffs acquired the mortgages by assignment only after the foreclosure sales and thus had no interest in the mortgages being foreclosed at the time of the publication of the notices of sale or at the time of the foreclosure sales.8

The plaintiffs then moved to vacate the judgments. At a hearing on the motions on April 17, 2009, the plaintiffs conceded that each complaint alleged a postnotice, postforeclosure sale assignment of the mortgage at issue, but they now represented to the judge that documents might exist that could show a prenotice, preforeclosure sale assignment of the mortgages. The judge granted the plaintiffs leave to produce such documents, provided they were produced in the form they existed in at the time the foreclosure sale was noticed and conducted. In response, the plaintiffs submitted hundreds of pages of documents to the judge, which they claimed established that the mortgages had been assigned to them before the foreclosures. Many of these documents related to the creation of the securitized mortgage pools in which the Ibanez and LaRace mortgages were purportedly included.9

The judge denied the plaintiffs’ motions to vacate judgment on October 14, 2009, concluding that the newly submitted documents did not alter the conclusion that the plaintiffs were not the holders of the respective mortgages at the time of foreclosure. We granted the parties’ applications for direct appellate review.

Factual background. We discuss each mortgage separately, describing when appropriate what the plaintiffs allege to have happened and what the documents in the record demonstrate.10

The Ibanez mortgage. On December 1, 2005, Antonio Ibanez took out a $103,500 loan for the purchase of property at 20 Crosby Street in Springfield, secured by a mortgage to the lender, Rose Mortgage, Inc. (Rose Mortgage). The mortgage was recorded the following day. Several days later, Rose Mortgage executed an assignment of this mortgage in blank, that is, an assignment that did not specify the name of the assignee.11 The blank space in the assignment was at some point stamped with the name of Option One Mortgage Corporation (Option One) as the assignee, and that assignment was recorded on June 7, 2006. Before the recording, on January 23, 2006, Option One executed an assignment of the Ibanez mortgage in blank.

According to U.S. Bank, Option One assigned the Ibanez mortgage to Lehman Brothers Bank, FSB, which assigned it to Lehman Brothers Holdings Inc., which then assigned it to the Structured Asset Securities Corporation,12 which then assigned the mortgage, pooled with approximately 1,220 other mortgage loans, to U.S. Bank, as trustee for the Structured Asset Securities Corporation Mortgage Pass-Through Certificates, Series 2006-Z. With this last assignment, the Ibanez and other loans were pooled into a trust and converted into mortgage-backed securities that can be bought and sold by investors — a process known as securitization.

For ease of reference, the chain of entities through which the Ibanez mortgage allegedly passed before the foreclosure sale is:

U.S. Bank National Association, as trustee for the Structured Asset Securities Corporation Mortgage Pass-Through Certificates, Series 2006-Z

According to U.S. Bank, the assignment of the Ibanez mortgage to U.S. Bank occurred pursuant to a December 1, 2006, trust agreement, which is not in the record. What is in the record is the private placement memorandum (PPM), dated December 26, 2006, a 273-page, unsigned offer of mortgage-backed securities to potential investors. The PPM describes the mortgage pools and the entities involved, and summarizes the provisions of the trust agreement, including the representation that mortgages “will be” assigned into the trust. According to the PPM, “[e]ach transfer of a Mortgage Loan from the Seller [Lehman Brothers Holdings Inc.] to the Depositor [Structured Asset Securities Corporation] and from the Depositor to the Trustee [U.S. Bank] will be intended to be a sale of that Mortgage Loan and will be reflected as such in the Sale and Assignment Agreement and the Trust Agreement, respectively.” The PPM also specifies that “[e]ach Mortgage Loan will be identified in a schedule appearing as an exhibit to the Trust Agreement.” However, U.S. Bank did not provide the judge with any mortgage schedule identifying the Ibanez loan as among the mortgages that were assigned in the trust agreement.

On April 17, 2007, U.S. Bank filed a complaint to foreclose on the Ibanez mortgage in the Land Court under the Servicemembers Civil Relief Act (Servicemembers Act), which restricts foreclosures against active duty members of the uniformed services. See 50 U.S.C. Appendix §§ 501, 511, 533 (2006 & Supp. II 2008).13 In the complaint, U.S. Bank represented that it was the “owner (or assignee) and holder” of the mortgage given by Ibanez for the property. A judgment issued on behalf of U.S. Bank on June 26, 2007, declaring that the mortgagor was not entitled to protection from foreclosure under the Servicemembers Act. In June, 2007, U.S. Bank also caused to be published in the Boston Globe the notice of the foreclosure sale required by G. L. c. 244, § 14. The notice identified U.S. Bank as the “present holder” of the mortgage.

At the foreclosure sale on July 5, 2007, the Ibanez property was purchased by U.S. Bank, as trustee for the securitization trust, for $94,350, a value significantly less than the outstanding debt and the estimated market value of the property. The foreclosure deed (from U.S. Bank, trustee, as the purported holder of the mortgage, to U.S. Bank, trustee, as the purchaser) and the statutory foreclosure affidavit were recorded on May 23, 2008. On September 2, 2008, more than one year after the sale, and more than five months after recording of the sale, American Home Mortgage Servicing, Inc., “as successor-in-interest” to Option One, which was until then the record holder of the Ibanez mortgage, executed a written assignment of that mortgage to U.S. Bank, as trustee for the securitization trust.14 This assignment was recorded on September 11, 2008.

The LaRace mortgage. On May 19, 2005, Mark and Tammy LaRace gave a mortgage for the property at 6 Brookburn Street in Springfield to Option One as security for a $103,200 loan; the mortgage was recorded that same day. On May 26, 2005, Option One executed an assignment of this mortgage in blank.

According to Wells Fargo, Option One later assigned the LaRace mortgage to Bank of America in a July 28, 2005, flow sale and servicing agreement. Bank of America then assigned it to Asset Backed Funding Corporation (ABFC) in an October 1, 2005, mortgage loan purchase agreement. Finally, ABFC pooled the mortgage with others and assigned it to Wells Fargo, as trustee for the ABFC 2005-OPT 1 Trust, ABFC Asset-Backed Certificates, Series 2005-OPT 1, pursuant to a pooling and servicing agreement (PSA).

For ease of reference, the chain of entities through which the LaRace mortgage allegedly passed before the foreclosure sale is:

Option One Mortgage Corporation (originator and record holder)

Bank of America

Asset Backed Funding Corporation (depositor)

Wells Fargo, as trustee for the ABFC 2005-OPT 1, ABFC Asset-Backed Certificates, Series 2005-OPT 1

Wells Fargo did not provide the judge with a copy of the flow sale and servicing agreement, so there is no document in the record reflecting an assignment of the LaRace mortgage by Option One to Bank of America. The plaintiff did produce an unexecuted copy of the mortgage loan purchase agreement, which was an exhibit to the PSA. The mortgage loan purchase agreement provides that Bank of America, as seller, “does hereby agree to and does hereby sell, assign, set over, and otherwise convey to the Purchaser [ABFC], without recourse, on the Closing Date . . . all of its right, title and interest in and to each Mortgage Loan.” The agreement makes reference to a schedule listing the assigned mortgage loans, but this schedule is not in the record, so there was no document before the judge showing that the LaRace mortgage was among the mortgage loans assigned to the ABFC.

Wells Fargo did provide the judge with a copy of the PSA, which is an agreement between the ABFC (as depositor), Option One (as servicer), and Wells Fargo (as trustee), but this copy was downloaded from the Securities and Exchange Commission website and was not signed. The PSA provides that the depositor “does hereby transfer, assign, set over and otherwise convey to the Trustee, on behalf of the Trust . . . all the right, title and interest of the Depositor . . . in and to . . . each Mortgage Loan identified on the Mortgage Loan Schedules,” and “does hereby deliver” to the trustee the original mortgage note, an original mortgage assignment “in form and substance acceptable for recording,” and other documents pertaining to each mortgage.

The copy of the PSA provided to the judge did not contain the loan schedules referenced in the agreement. Instead, Wells Fargo submitted a schedule that it represented identified the loans assigned in the PSA, which did not include property addresses, names of mortgagors, or any number that corresponds to the loan number or servicing number on the LaRace mortgage.Wells Fargo contends that a loan with the LaRace property’s zip code and city is the LaRace mortgage loan because the payment history and loan amount matches the LaRace loan.

On April 27, 2007, Wells Fargo filed a complaint under the Servicemembers Act in the Land Court to foreclose on the LaRace mortgage. The complaint represented Wells Fargo as the “owner (or assignee) and holder” of the mortgage given by the LaRaces for the property. A judgment issued on behalf of Wells Fargo on July 3, 2007, indicating that the LaRaces were not beneficiaries of the Servicemembers Act and that foreclosure could proceed in accordance with the terms of the power of sale. In June, 2007, Wells Fargo caused to be published in the Boston Globe the statutory notice of sale, identifying itself as the “present holder” of the mortgage.

At the foreclosure sale on July 5, 2007, Wells Fargo, as trustee, purchased the LaRace property for $120,397.03, a value significantly below its estimated market value. Wells Fargo did not execute a statutory foreclosure affidavit or foreclosure deed until May 7, 2008. That same day, Option One, which was still the record holder of the LaRace mortgage, executed an assignment of the mortgage to Wells Fargo as trustee; the assignment was recorded on May 12, 2008. Although executed ten months after the foreclosure sale, the assignment declared an effective date of April 18, 2007, a date that preceded the publication of the notice of sale and the foreclosure sale.

Discussion. The plaintiffs brought actions under G. L. c. 240, § 6, seeking declarations that the defendant mortgagors’ titles had been extinguished and that the plaintiffs were the fee simple owners of the foreclosed properties. As such, the plaintiffs bore the burden of establishing their entitlement to the relief sought. Sheriff’s Meadow Found., Inc. v. Bay-Courte Edgartown, Inc., 401 Mass. 267, 269 (1987). To meet this burden, they were required “not merely to demonstrate better title . . . than the defendants possess, but . . . to prove sufficient title to succeed in [the] action.” Id. See NationsBanc Mtge. Corp. v. Eisenhauer, 49 Mass. App. Ct. 727, 730 (2000). There is no question that the relief the plaintiffs sought required them to establish the validity of the foreclosure sales on which their claim to clear title rested.

Massachusetts does not require a mortgage holder to obtain judicial authorization to foreclose on a mortgaged property. See G. L. c. 183, § 21; G. L. c. 244, § 14. With the exception of the limited judicial procedure aimed at certifying that the mortgagor is not a beneficiary of the Servicemembers Act, a mortgage holder can foreclose on a property, as the plaintiffs did here, by exercise of the statutory power of sale, if such a power is granted by the mortgage itself. See Beaton v. Land Court, 367 Mass. 385, 390-391, 393, appeal dismissed, 423 U.S. 806 (1975).

Where a mortgage grants a mortgage holder the power of sale, as did both the Ibanez and LaRace mortgages, it includes by reference the power of sale set out in G. L. c. 183, § 21, and further regulated by G. L. c. 244, §§ 11-17C. Under G. L. c. 183, § 21, after a mortgagor defaults in the performance of the underlying note, the mortgage holder may sell the property at a public auction and convey the property to the purchaser in fee simple, “and such sale shall forever bar the mortgagor and all persons claiming under him from all right and interest in the mortgaged premises, whether at law or in equity.” Even where there is a dispute as to whether the mortgagor was in default or whether the party claiming to be the mortgage holder is the true mortgage holder, the foreclosure goes forward unless the mortgagor files an action and obtains a court order enjoining the foreclosure.15 See Beaton v. Land Court, supra at 393.

Recognizing the substantial power that the statutory scheme affords to a mortgage holder to foreclose without immediate judicial oversight, we adhere to the familiar rule that “one who sells under a power [of sale] must follow strictly its terms. If he fails to do so there is no valid execution of the power, and the sale is wholly void.” Moore v. Dick, 187 Mass. 207, 211 (1905). See Roche v. Farnsworth, 106 Mass. 509, 513 (1871) (power of sale contained in mortgage “must be executed in strict compliance with its terms”). See also McGreevey v. Charlestown Five Cents Sav. Bank, 294 Mass. 480, 484 (1936).16

One of the terms of the power of sale that must be strictly adhered to is the restriction on who is entitled to foreclose. The “statutory power of sale” can be exercised by “the mortgagee or his executors, administrators, successors or assigns.” G. L. c. 183, § 21. Under G. L. c. 244, § 14, “[t]he mortgagee or person having his estate in the land mortgaged, or a person authorized by the power of sale, or the attorney duly authorized by a writing under seal, or the legal guardian or conservator of such mortgagee or person acting in the name of such mortgagee or person” is empowered to exercise the statutory power of sale. Any effort to foreclose by a party lacking “jurisdiction and authority” to carry out a foreclosure under these statutes is void. Chace v. Morse, 189 Mass. 559, 561 (1905), citing Moore v. Dick, supra. See Davenport v. HSBC Bank USA, 275 Mich. App. 344, 347-348 (2007) (attempt to foreclose by party that had not yet been assigned mortgage results in “structural defect that goes to the very heart of defendant’s ability to foreclose by advertisement,” and renders foreclosure sale void).

A related statutory requirement that must be strictly adhered to in a foreclosure by power of sale is the notice requirement articulated in G. L. c. 244, § 14. That statute provides that “no sale under such power shall be effectual to foreclose a mortgage, unless, previous to such sale,” advance notice of the foreclosure sale has been provided to the mortgagee, to other interested parties, and by publication in a newspaper published in the town where the mortgaged land lies or of general circulation in that town. Id. “The manner in which the notice of the proposed sale shall be given is one of the important terms of the power, and a strict compliance with it is essential to the valid exercise of the power.” Moore v. Dick, supra at 212. See Chace v. Morse, supra (“where a certain notice is prescribed, a sale without any notice, or upon a notice lacking the essential requirements of the written power, would be void as a proceeding for foreclosure”). See also McGreevey v. Charlestown Five Cents Sav. Bank, supra. Because only a present holder of the mortgage is authorized to foreclose on the mortgaged property, and because the mortgagor is entitled to know who is foreclosing and selling the property, the failure to identify the holder of the mortgage in the notice of sale may render the notice defective and the foreclosure sale void.17 See Roche v. Farnsworth, supra (mortgage sale void where notice of sale identified original mortgagee but not mortgage holder at time of notice and sale). See also Bottomly v. Kabachnick, 13 Mass. App. Ct. 480, 483-484 (1982) (foreclosure void where holder of mortgage not identified in notice of sale).

For the plaintiffs to obtain the judicial declaration of clear title that they seek, they had to prove their authority to foreclose under the power of sale and show their compliance with the requirements on which this authority rests. Here, the plaintiffs were not the original mortgagees to whom the power of sale was granted; rather, they claimed the authority to foreclose as the eventual assignees of the original mortgagees. Under the plain language of G. L. c. 183, § 21, and G. L. c. 244, § 14, the plaintiffs had the authority to exercise the power of sale contained in the Ibanez and LaRace mortgages only if they were the assignees of the mortgages at the time of the notice of sale and the subsequent foreclosure sale. See In re Schwartz, 366 B.R. 265, 269 (Bankr. D. Mass. 2007) (“Acquiring the mortgage after the entry and foreclosure sale does not satisfy the Massachusetts statute”).18 See also Jeff-Ray Corp. v. Jacobson, 566 So. 2d 885, 886 (Fla. Dist. Ct. App. 1990) (per curiam) (foreclosure action could not be based on assignment of mortgage dated four months after commencement of foreclosure proceeding).

The plaintiffs claim that the securitization documents they submitted establish valid assignments that made them the holders of the Ibanez and LaRace mortgages before the notice of sale and the foreclosure sale. We turn, then, to the documentation submitted by the plaintiffs to determine whether it met the requirements of a valid assignment.

Like a sale of land itself, the assignment of a mortgage is a conveyance of an interest in land that requires a writing signed by the grantor. See G. L. c. 183, § 3; Saint Patrick’s Religious, Educ. & Charitable Ass’n v. Hale, 227 Mass. 175, 177 (1917). In a “title theory state” like Massachusetts, a mortgage is a transfer of legal title in a property to secure a debt. See Faneuil Investors Group, Ltd. Partnership v. Selectmen of Dennis, 458 Mass. 1, 6 (2010). Therefore, when a person borrows money to purchase a home and gives the lender a mortgage, the homeowner-mortgagor retains only equitable title in the home; the legal title is held by the mortgagee. See Vee Jay Realty Trust Co. v. DiCroce, 360 Mass. 751, 753 (1972), quoting Dolliver v. St. Joseph Fire & Marine Ins. Co., 128 Mass. 315, 316 (1880) (although “as to all the world except the mortgagee, a mortgagor is the owner of the mortgaged lands,” mortgagee has legal title to property); Maglione v. BancBoston Mtge. Corp., 29 Mass. App. Ct. 88, 90 (1990). Where, as here, mortgage loans are pooled together in a trust and converted into mortgage-backed securities, the underlying promissory notes serve as financial instruments generating a potential income stream for investors, but the mortgages securing these notes are still legal title to someone’s home or farm and must be treated as such.

Focusing first on the Ibanez mortgage, U.S. Bank argues that it was assigned the mortgage under the trust agreement described in the PPM, but it did not submit a copy of this trust agreement to the judge. The PPM, however, described the trust agreement as an agreement to be executed in the future, so it only furnished evidence of an intent to assign mortgages to U.S. Bank, not proof of their actual assignment. Even if there were an executed trust agreement with language of present assignment, U.S. Bank did not produce the schedule of loans and mortgages that was an exhibit to that agreement, so it failed to show that the Ibanez mortgage was among the mortgages to be assigned by that agreement. Finally, even if there were an executed trust agreement with the required schedule, U.S. Bank failed to furnish any evidence that the entity assigning the mortgage — Structured Asset Securities Corporation — ever held the mortgage to be assigned. The last assignment of the mortgage on record was from Rose Mortgage to Option One; nothing was submitted to the judge indicating that Option One ever assigned the mortgage to anyone before the foreclosure sale.19 Thus, based on the documents submitted to the judge, Option One, not U.S. Bank, was the mortgage holder at the time of the foreclosure, and U.S. Bank did not have the authority to foreclose the mortgage.

Turning to the LaRace mortgage, Wells Fargo claims that, before it issued the foreclosure notice, it was assigned the LaRace mortgage under the PSA. The PSA, in contrast with U.S. Bank’s PPM, uses the language of a present assignment (“does hereby . . . assign” and “does hereby deliver”) rather than an intent to assign in the future. But the mortgage loan schedule Wells Fargo submitted failed to identify with adequate specificity the LaRace mortgage as one of the mortgages assigned in the PSA. Moreover, Wells Fargo provided the judge with no document that reflected that the ABFC (depositor) held the LaRace mortgage that it was purportedly assigning in the PSA. As with the Ibanez loan, the record holder of the LaRace loan was Option One, and nothing was submitted to the judge which demonstrated that the LaRace loan was ever assigned by Option One to another entity before the publication of the notice and the sale.

Where a plaintiff files a complaint asking for a declaration of clear title after a mortgage foreclosure, a judge is entitled to ask for proof that the foreclosing entity was the mortgage holder at the time of the notice of sale and foreclosure, or was one of the parties authorized to foreclose under G. L. c. 183, § 21, and G. L. c. 244, § 14. A plaintiff that cannot make this modest showing cannot justly proclaim that it was unfairly denied a declaration of clear title. See In re Schwartz, supra at 266 (“When HomEq [Servicing Corporation] was required to prove its authority to conduct the sale, and despite having been given ample opportunity to do so, what it produced instead was a jumble of documents and conclusory statements, some of which are not supported by the documents and indeed even contradicted by them”). See also Bayview Loan Servicing, LLC v. Nelson, 382 Ill. App. 3d 1184, 1188 (2008) (reversing grant of summary judgment in favor of financial entity in foreclosure action, where there was “no evidence that [the entity] ever obtained any legal interest in the subject property”).

We do not suggest that an assignment must be in recordable form at the time of the notice of sale or the subsequent foreclosure sale, although recording is likely the better practice. Where a pool of mortgages is assigned to a securitized trust, the executed agreement that assigns the pool of mortgages, with a schedule of the pooled mortgage loans that clearly and specifically identifies the mortgage at issue as among those assigned, may suffice to establish the trustee as the mortgage holder. However, there must be proof that the assignment was made by a party that itself held the mortgage. See In re Samuels, 415 B.R. 8, 20 (Bankr. D. Mass. 2009). A foreclosing entity may provide a complete chain of assignments linking it to the record holder of the mortgage, or a single assignment from the record holder of the mortgage. See In re Parrish, 326 B.R. 708, 720 (Bankr. N.D. Ohio 2005) (“If the claimant acquired the note and mortgage from the original lender or from another party who acquired it from the original lender, the claimant can meet its burden through evidence that traces the loan from the original lender to the claimant”). The key in either case is that the foreclosing entity must hold the mortgage at the time of the notice and sale in order accurately to identify itself as the present holder in the notice and in order to have the authority to foreclose under the power of sale (or the foreclosing entity must be one of the parties authorized to foreclose under G. L. c. 183, § 21, and G. L. c. 244, § 14).

The judge did not err in concluding that the securitization documents submitted by the plaintiffs failed to demonstrate that they were the holders of the Ibanez and LaRace mortgages, respectively, at the time of the publication of the notices and the sales. The judge, therefore, did not err in rendering judgments against the plaintiffs and in denying the plaintiffs’ motions to vacate the judgments.20

We now turn briefly to three other arguments raised by the plaintiffs on appeal. First, the plaintiffs initially contended that the assignments in blank executed by Option One, identifying the assignor but not the assignee, not only “evidence[] and confirm[] the assignments that occurred by virtue of the securitization agreements,” but “are effective assignments in their own right.” But in their reply briefs they conceded that the assignments in blank did not constitute a lawful assignment of the mortgages. Their concession is appropriate. We have long held that a conveyance of real property, such as a mortgage, that does not name the assignee conveys nothing and is void; we do not regard an assignment of land in blank as giving legal title in land to the bearer of the assignment. See Flavin v. Morrissey, 327 Mass. 217, 219 (1951); Macurda v. Fuller, 225 Mass. 341, 344 (1916). See also G. L. c. 183, § 3.

Second, the plaintiffs contend that, because they held the mortgage note, they had a sufficient financial interest in the mortgage to allow them to foreclose. In Massachusetts, where a note has been assigned but there is no written assignment of the mortgage underlying the note, the assignment of the note does not carry with it the assignment of the mortgage. Barnes v. Boardman, 149 Mass. 106, 114 (1889). Rather, the holder of the mortgage holds the mortgage in trust for the purchaser of the note, who has an equitable right to obtain an assignment of the mortgage, which may be accomplished by filing an action in court and obtaining an equitable order of assignment. Id. (“In some jurisdictions it is held that the mere transfer of the debt, without any assignment or even mention of the mortgage, carries the mortgage with it, so as to enable the assignee to assert his title in an action at law. . . . This doctrine has not prevailed in Massachusetts, and the tendency of the decisions here has been, that in such cases the mortgagee would hold the legal title in trust for the purchaser of the debt, and that the latter might obtain a conveyance by a bill in equity”). See Young v. Miller, 6 Gray 152, 154 (1856). In the absence of a valid written assignment of a mortgage or a court order of assignment, the mortgage holder remains unchanged. This common-law principle was later incorporated in the statute enacted in 1912 establishing the statutory power of sale, which grants such a power to “the mortgagee or his executors, administrators, successors or assigns,” but not to a party that is the equitable beneficiary of a mortgage held by another. G. L. c. 183, § 21, inserted by St. 1912, c. 502, § 6.

Third, the plaintiffs initially argued that postsale assignments were sufficient to establish their authority to foreclose, and now argue that these assignments are sufficient when taken in conjunction with the evidence of a presale assignment. They argue that the use of postsale assignments was customary in the industry, and point to Title Standard No. 58 (3) issued by the Real Estate Bar Association for Massachusetts, which declares: “A title is not defective by reason of . . . [t]he recording of an Assignment of Mortgage executed either prior, or subsequent, to foreclosure where said Mortgage has been foreclosed, of record, by the Assignee.”21 To the extent that the plaintiffs rely on this title standard for the proposition that an entity that does not hold a mortgage may foreclose on a property, and then cure the cloud on title by a later assignment of a mortgage, their reliance is misplaced because this proposition is contrary to G. L. c. 183, § 21, and G. L. c. 244, § 14. If the plaintiffs did not have their assignments to the Ibanez and LaRace mortgages at the time of the publication of the notices and the sales, they lacked authority to foreclose under G. L. c. 183, § 21, and G. L. c. 244, § 14, and their published claims to be the present holders of the mortgages were false. Nor may a postforeclosure assignment be treated as a pre-foreclosure assignment simply by declaring an “effective date” that precedes the notice of sale and foreclosure, as did Option One’s assignment of the LaRace mortgage to Wells Fargo. Because an assignment of a mortgage is a transfer of legal title, it becomes effective with respect to the power of sale only on the transfer; it cannot become effective before the transfer. See In re Schwartz, supra at 269.

However, we do not disagree with Title Standard No. 58 (3) that, where an assignment is confirmatory of an earlier, valid assignment made prior to the publication of notice and execution of the sale, that confirmatory assignment may be executed and recorded after the foreclosure, and doing so will not make the title defective. A valid assignment of a mortgage gives the holder of that mortgage the statutory power to sell after a default regardless whether the assignment has been recorded. See G. L. c. 183, § 21; MacFarlane v. Thompson, 241 Mass. 486, 489 (1922). Where the earlier assignment is not in recordable form or bears some defect, a written assignment executed after foreclosure that confirms the earlier assignment may be properly recorded. See Bon v. Graves, 216 Mass. 440, 444-445 (1914). A confirmatory assignment, however, cannot confirm an assignment that was not validly made earlier or backdate an assignment being made for the first time. See Scaplen v. Blanchard, 187 Mass. 73, 76 (1904) (confirmatory deed “creates no title” but “takes the place of the original deed, and is evidence of the making of the former conveyance as of the time when it was made”). Where there is no prior valid assignment, a subsequent assignment by the mortgage holder to the note holder is not a confirmatory assignment because there is no earlier written assignment to confirm. In this case, based on the record before the judge, the plaintiffs failed to prove that they obtained valid written assignments of the Ibanez and LaRace mortgages before their foreclosures, so the postforeclosure assignments were not confirmatory of earlier valid assignments.

Finally, we reject the plaintiffs’ request that our ruling be prospective in its application. A prospective ruling is only appropriate, in limited circumstances, when we make a significant change in the common law. See Papadopoulos v. Target Corp., 457 Mass. 368, 384 (2010) (noting “normal rule of retroactivity”); Payton v. Abbott Labs, 386 Mass. 540, 565 (1982). We have not done so here. The legal principles and requirements we set forth are well established in our case law and our statutes. All that has changed is the plaintiffs’ apparent failure to abide by those principles and requirements in the rush to sell mortgage-backed securities.

Conclusion. For the reasons stated, we agree with the judge that the plaintiffs did not demonstrate that they were the holders of the Ibanez and LaRace mortgages at the time that they foreclosed these properties, and therefore failed to demonstrate that they acquired fee simple title to these properties by purchasing them at the foreclosure sale.

Judgments affirmed.

CORDY, J. (concurring, with whom Botsford, J., joins). I concur fully in the opinion of the court, and write separately only to underscore that what is surprising about these cases is not the statement of principles articulated by the court regarding title law and the law of foreclosure in Massachusetts, but rather the utter carelessness with which the plaintiff banks documented the titles to their assets. There is no dispute that the mortgagors of the properties in question had defaulted on their obligations, and that the mortgaged properties were subject to foreclosure. Before commencing such an action, however, the holder of an assigned mortgage needs to take care to ensure that his legal paperwork is in order. Although there was no apparent actual unfairness here to the mortgagors, that is not the point. Foreclosure is a powerful act with significant consequences, and Massachusetts law has always required that it proceed strictly in accord with the statutes that govern it. As the opinion of the court notes, such strict compliance is necessary because Massachusetts is both a title theory State and allows for extrajudicial foreclosure.

The type of sophisticated transactions leading up to the accumulation of the notes and mortgages in question in these cases and their securitization, and, ultimately the sale of mortgaged-backed securities, are not barred nor even burdened by the requirements of Massachusetts law. The plaintiff banks, who brought these cases to clear the titles that they acquired at their own foreclosure sales, have simply failed to prove that the underlying assignments of the mortgages that they allege (and would have) entitled them to foreclose ever existed in any legally cognizable form before they exercised the power of sale that accompanies those assignments. The court’s opinion clearly states that such assignments do not need to be in recordable form or recorded before the foreclosure, but they do have to have been effectuated.

What is more complicated, and not addressed in this opinion, because the issue was not before us, is the effect of the conduct of banks such as the plaintiffs here, on a bona fide third-party purchaser who may have relied on the foreclosure title of the bank and the confirmative assignment and affidavit of foreclosure recorded by the bank subsequent to that foreclosure but prior to the purchase by the third party, especially where the party whose property was foreclosed was in fact in violation of the mortgage covenants, had notice of the foreclosure, and took no action to contest it.

1 For the Structured Asset Securities Corporation Mortgage Pass-Through Certificates, Series 2006-Z.

2 Wells Fargo Bank, N.A., trustee, vs. Mark A. LaRace

& another.

3 The Appeals Court granted the plaintiffs’ motion to consolidate these cases.

4 Chief Justice Marshall participated in the deliberation on this case prior to her retirement.

5 We acknowledge the amicus briefs filed by the Attorney General; the Real Estate Bar Association for Massachusetts, Inc.; Marie McDonnell; and the National Consumer Law Center, together with Darlene Manson, Germano DePina, Robert Lane, Ann Coiley, Roberto Szumik, and Geraldo Dosanjos.

6 The uncertainty surrounding the first issue was the reason the plaintiffs sought a declaration of clear title in order to obtain title insurance for these properties. The second issue was raised by the judge in the LaRace case at a January 5, 2009, case management conference.

7 The judge also concluded that the Boston Globe was a newspaper of general circulation in Springfield, so the foreclosures were not rendered invalid on that ground because notice was published in that newspaper.

8 In the third case, LaSalle Bank National Association, trustee for the certificate holders of Bear Stearns Asset Backed Securities I, LLC Asset-Backed Certificates, Series 2007-HE2 vs. Freddy Rosario, the judge concluded that the mortgage foreclosure “was not rendered invalid by its failure to record the assignment reflecting its status as holder of the mortgage prior to the foreclosure since it was, in fact, the holder by assignment at the time of the foreclosure, it truthfully claimed that status in the notice, and it could have produced proof of that status (the unrecorded assignment) if asked.”

9 On June 1, 2009, attorneys for the defendant mortgagors filed their appearance in the cases for the first time.

10 The LaRace defendants allege that the documents submitted to the judge following the plaintiffs’ motions to vacate judgment are not properly in the record before us. They also allege that several of these documents are not properly authenticated. Because we affirm the judgment on other grounds, we do not address these concerns, and assume that these documents are properly before us and were adequately authenticated.

11 This signed and notarized document states: “FOR VALUE RECEIVED, the undersigned hereby grants, assigns and transfers to _______ all beneficial interest under that certain Mortgage dated December 1, 2005 executed by Antonio Ibanez . . . .”

12 The Structured Asset Securities Corporation is a wholly owned direct subsidiary of Lehman Commercial Paper Inc., which is in turn a wholly owned, direct subsidiary of Lehman Brothers Holdings Inc.

13 As implemented in Massachusetts, a mortgage holder is required to go to court to obtain a judgment declaring that the mortgagor is not a beneficiary of the Servicemembers Act before proceeding to foreclosure. St. 1943, c. 57, as amended through St. 1998, c. 142.

14 The Land Court judge questioned whether American Home Mortgage Servicing, Inc., was in fact a successor in interest to Option One. Given our affirmance of the judgment on other grounds, we need not address this question.

15 An alternative to foreclosure through the right of statutory sale is foreclosure by entry, by which a mortgage holder who peaceably enters a property and remains for three years after recording a certificate or memorandum of entry forecloses the mortgagor’s right of redemption. See G. L. c. 244, §§ 1, 2; Joyner v. Lenox Sav. Bank, 322 Mass. 46, 52-53 (1947). A foreclosure by entry may provide a separate ground for a claim of clear title apart from the foreclosure by execution of the power of sale. See, e.g., Grabiel v. Michelson, 297 Mass. 227, 228-229 (1937). Because the plaintiffs do not claim clear title based on foreclosure by entry, we do not discuss it further.

16 We recognize that a mortgage holder must not only act in strict compliance with its power of sale but must also “act in good faith and . . . use reasonable diligence to protect the interests of the mortgagor,” and this responsibility is “more exacting” where the mortgage holder becomes the buyer at the foreclosure sale, as occurred here. See Williams v. Resolution GGF Oy, 417 Mass. 377, 382-383 (1994), quoting Seppala & Aho Constr. Co. v. Petersen, 373 Mass. 316, 320 (1977). Because the issue was not raised by the defendant mortgagors or the judge, we do not consider whether the plaintiffs breached this obligation.

17 The form of foreclosure notice provided in G. L. c. 244, § 14, calls for the present holder of the mortgage to identify itself and sign the notice. While the statute permits other forms to be used and allows the statutory form to be “altered as circumstances require,” G. L. c. 244, § 14, we do not interpret this flexibility to suggest that the present holder of the mortgage need not identify itself in the notice.

18 The plaintiffs were not authorized to foreclose by virtue of any of the other provisions of G. L. c. 244, § 14: they were not the guardian or conservator, or acting in the name of, a person so authorized; nor were they the attorney duly authorized by a writing under seal.

19 Ibanez challenges the validity of this assignment to Option One. Because of the failure of U.S. Bank to document any preforeclosure sale assignment or chain of assignments by which it obtained the Ibanez mortgage from Option One, it is unnecessary to address the validity of the assignment from Rose Mortgage to Option One.

20 The plaintiffs have not pressed the procedural question whether the judge exceeded his authority in rendering judgment against them on their motions for default judgment, and we do not address it here.

21 Title Standard No. 58 (3) issued by the Real Estate Bar Association for Massachusetts continues: “However, if the Assignment is not dated prior, or stated to be effective prior, to the commencement of a foreclosure, then a foreclosure sale after April 19, 2007 may be subject to challenge in the Bankruptcy Court,” citing In re Schwartz, 366 B.R. 265 (Bankr. D. Mass. 2007).

updated 12/6/2010 2:10:09 PM ET 2010-12-06T19:10:09

.

JACKSONVILLE, Florida — Lender Processing Services is riding the waves of foreclosures sweeping the United States, but in late October its CEO, Jeff Carbiener, found himself needing to reassure investors in the $2.8 billion company.

Although profits were rolling in, LPS’s stock had taken a hit in the wake of revelations that mortgage companies across the country had filed fraudulent documents in foreclosures cases. Earlier in the year, the company, which handles more than half of the nation’s foreclosures, had disclosed that it was under federal criminal investigation and admitted that employees at a small subsidiary had falsely signed foreclosure documents.

Still, Carbiener told the Wall Street analysts in an October 29 conference call that LPS’s legal concerns were overblown, and the stock has jumped 13 percent since its close the day before the call.

But a Reuters investigation shows that LPS’s legal woes are more serious than he let on. Public records reveal that the company’s LPS Default Solutions unit produced documents of dubious authenticity in far larger quantities than it has disclosed, and over a much longer timespan.

Questionable signing and notarization practices weren’t limited to its subsidiary, called DocX, but occurred in at least one of LPS’s own offices, mortgage assignments filed in county recorders’ offices show. And rather than halt such practices after the federal investigation got underway, the company shifted the signing to firms with which it has close business ties. LPS provided personnel to work in the new signing operations, according to information from an LPS spokeswoman and court records including an October 21 ruling by a judge in Brooklyn, New York. Records in county recorders’ offices, and in the judge’s opinion, show that “robosigning” and preparation of apparently false documents went on at these sites on a large scale.

In one instance, it helped set up a massive signing operation at the nearby office of a major client, a spokeswoman for the client, American Home Mortgage Servicing, confirmed. LPS-hired notaries who worked there said in interviews that troves of documents were improperly handled. They said that about 200 affidavits per day were robosigned during the two months the two notaries remained there.

A spokeswoman for LPS confirmed to Reuters that it had helped other firms establish operations that performed the same function. LPS spokeswoman Michelle Kersch didn’t specify which firms. But beginning early in 2010, county recorders’ records show, signing shifted also to law firms under contract with LPS.

Interviews with key players and court records also show that pending investigations and lawsuits pose a bigger threat to the company than Carbiener let on.

The criminal investigation in Jacksonville by federal prosecutors and the Federal Bureau of Investigation is intensifying. The same goes for a separate inquiry by the Florida attorney general’s office. Individuals with direct knowledge of the federal inquiry said that prosecutors have impaneled a grand jury, begun calling witnesses and subpoenaed records from LPS.

The company confirmed to Reuters that it has hired Paul McNulty, former deputy U.S. attorney general in the George W. Bush administration, to represent it in the investigation. A spokeswoman for the U.S. Attorney’s office declined to comment on the probe.

The U.S. Comptroller of the Currency’s office, which is responsible for supervising national banks, also announced in November that it had teamed up with the Federal Reserve to conduct an on-site examination of LPS.

Linda Green is/was an employee of DocX a subsidiary of Lender Processing Services located in Alpharetta, Georgia. Her signature was forged on key sensitive documents relating to county land records.

Below is a document that Shapiro & Fishman filed as a CORRECTIVE ASSIGNMENT OF MORTGAGE.

What about the Satisfactions? In DOCX’s website they said:

“DOCX has built its solid reputation at not only managing large assignment projects, but satisfactions as well“.

Exactly how many documents were signed by Green’s name as VP for MERS between these dates?

Who do we contact to make this a nationwide recall alert like the recent “egg recall” containing salmonella?

Exactly who is being notified if there is any title issues on your homes?

Has there been a recall notice sent to County Recorders on this issue?

Are there more VP’s of MERS who had no authority to execute documents?

R.K. Arnold

Mortgage Electronic Registration Systems

Action Date: November 18, 2010

Location: WASHINGTON, DC

As the many problems (frauds) are exposed regarding documents used by mortgage-backed trusts in foreclosures, some revelations stand out. Literally millions of foreclosures by mortgage-backed trusts hinge on a Mortgage Assignment signed by an officer of Mortgage Electronic Registration Systems (“MERS”) showing that the mortgage in question was transferred to the trust by MERS. The “MERS officer” who signs the Mortgage Assignment is actually most often an employee of a mortgage servicing company that is paid by the trust.

MERS itself has only 50 employees and they are not involved in signing mortgage assignments to trusts. These servicing company employees sign as officers of MERS “as nominee for” a particular mortgage company or bank. They are not employees of the mortgage companies or employees of the original named lender, but their titles on the Mortgage Assignment belie this and typically read: “Linda Green, Vice President, Mortgage Electronic Registration Systems, Inc., as nominee for American Brokers Conduit.”

MERS president R.K. Arnold testified in Senate testimony earlier this week that there are over 20,000 MERS “certifying officers.” To become a MERS certifying officer, a mortgage servicing company employee need only complete an online form and pay $25.00. Because of the concealment of the actual employer on the Mortgage Assignments, it is easy enough for Courts, and homeowners, to believe that they are examining a document prepared by the lender that sold the mortgage to the trust, when, in fact, the signer was a servicing company clerk paid by the trust itself.

The representative of the GRANTOR is, in truth, a paid employee of the GRANTEE. In hundreds of thousands of cases, the authority is, therefore, misrepresented. It is now also coming to light that in tens of thousands of cases, the individuals signing these forms did not even sign their own names. The documents were made to look official because other mortgage servicing company employees signed as witnesses and then all four “signatures” were notarized by yet another mortgage servicing company employee. The titles were false, the signatures were forged, the “witnessing” was a lie, as was the notarization. Despite all of these false statements, the BIGGEST LIE on these documents is that the trust acquired the mortgage on the date stated plainly on the Mortgage Assignment. In truth, no such transfers ever took place as represented by these MERS certifying officers (or their stand-in forgers). The date chosen almost always corresponds not to an actual transfer, but to the date roughly corresponding to the time the loan went into default. The Mortgage Assignment was prepared only to provide “proof” that the trust owned the mortgage. Until courts require Trusts to come forward with actual proof that they acquired the mortgages in question, specifying whom they paid and how much they paid for each such trust-owned mortgage, the actual owner of these mortgages will never be known.

In response to the exposure of the widespread fraud in the securitization process, the American Bankers Association issued a statement essentially saying that Mortgage Assignments were unnecessary. Investors and regulators were told, however, that the trusts owned the mortgages and notes in each pool of mortgages and that valid Assignments of Mortgages had been obtained. Where the proof of ownership put forth by the trusts is a sworn statement by a MERS “certifying officer” who had no knowledge whatsoever of the transactions involved and did not even review documents related to the transactions, such proof of ownership should be deemed worthless by the Courts. Other litigants are not allowed to manufacture their own evidence and offer it as proof at trial – there should be no exception for mortgage-backed trusts.

In particular, where the “MERS Certifying Officer” is actually an employee of the law firm hired to handle the foreclosure, such documents should be stricken and sanctioned. “MERS Certifying Officers” should be the next group required to testify before Congress. Here are the statistics for one Florida county, Palm Beach County, regarding the number of Mortgage Assignments filed by Mortgage Electronic Registration Systems: January, 2009: 1,164; February, 2009: February, 2009: 1,230; March, 2009: March, 2009: 1,113. An examination of just one day’s (March 31, 2009) filed Mortgage Assignments reveals that the signers of these Assignments are the very same mortgage servicing company employees who signed the “no-actual knowledge” Affidavits that triggered the national scrutiny: Jeffrey Stephan from Ally, Erica Johnson-Seck from IndyMac, Crystal Moore from Nationwide Title Clearing, Liquenda Allotey from Lender Processing Services, Denise Bailey from Litton Loan Services, Noriko Colston, Krystal Hall, and other well-known professional signers from the mortgage servicing industry. The most frequent signers from that particular day were two lawyers, associates in the law firm representing the trusts, who signed as Assistant Secretary for Mortgage Electronic Registration Systems.

Just a few weeks ago Wells Fargo made an announcement that there were no problems at all blah blah blah…and now they have passed the baton to Lender Processing Services…

LPS: no defects in related foreclosures, no fee-splitting

by JACOB GAFFNEY

Friday, October 29th, 2010, 7:30 am

Lender Processing Services (LPS: 28.69 +4.33%) began reducing its foreclosure signing services back in 2008 and stands by its mortgage processing services. Further, when the firm caught a manager robo-signing foreclosure documents, the only such case it says it found, that manager was immediately dismissed and documents remediated.

“We believe we have taken appropriate steps and we do not believe it resulted in any wrongful foreclosures,” said LPS CEO Jeff Carbiener in a third-quarter conference call to investors Friday. “We no longer provide foreclosure document services.”

Carbiener also said that his company does not participate in fee-splitting or revenue-sharing with lawyers, another recent charge against the company.

“We are not an equity owner in any law firm,” he said.

LPS, a mortgage and real estate technology and services provider, reported net earnings of $78.7 million or 85 cents per share, in the third quarter of 2010, up from $75.5 million or 78 cents per share, in last year’s quarter.

JPMorgan Chase (JPM: 37.605 +0.25%), Bank of America (BAC: 11.4301 -0.87%) and Wells Fargo (WFC: 25.85 -0.35%) also now use LPS desktop management software for dealing with clerical issues when it comes to mortgages, the CEO said.

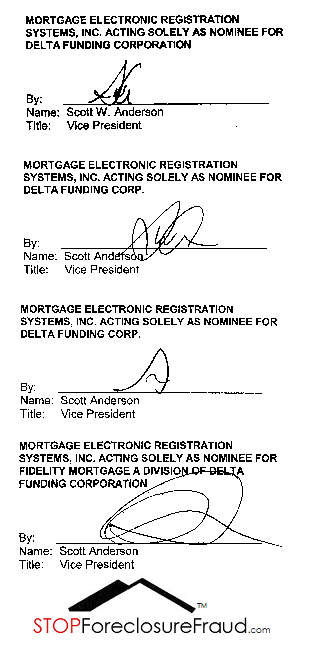

Scott Anderson

Deutsche Bank National Trust Co.

Law Offices of Marshall Watson

New Century Mortgage Corp.

Ocwen Loan Servicing, LLC

Action Date: October 21, 2010

Location: St. Petersburg, FL

On October 21, 2010, in St. Petersburg, Florida, Circuit Court Judge Anthony Rondolino dismissed the plaintiff’s First Amended Complaint in a foreclosure action, Deutsche Bank National Trust Co., et al. v. Donnie J. Decker, et al., Case No. 09-20548-CI-13, 6th Judicial Circuit, in and for Pinellas County, Florida.

The complaint was brought by Deutsche Bank as trustee for a mortgage-backed trust, Morgan Stanley Dean Witter Capital, Inc., under a Pooling & Servicing Agreement dated May 1, 2001. The original complaint was dismissed due to chain-of-title problems.

The amended complaint included an Assignment from New Century Mortgage Corp. to the plaintiff that was executed on February 17, 2010 by Scott Anderson in his capacity as an Executive Vice President of Residential Loan Servicing for Ocwen Loan Servicing, LLC through its authority as Attorney-In-Fact for New Century Mortgage Corporation. Regarding this Assignment, Judge Rondolino commented as follows:

“There is nothing about this assignment which would support a determination at the pleading stage that it is invalid. On the other hand, should evidence be presented at a summary judgment hearing that New Century Mortgage Corporation, LLC became the subject of a bankruptcy proceeding which resulted in a liquidation order, the validity of this assignment would be called into question. Then, absent specific proof that Ocwen had authority from either the bankruptcy court or the liquidation trustee, this disposition of New Century’s (the debtor in bankruptcy) asset there would be a disputed material fact precluding a summary judgment. These concerns however are not ripe at this time…”

In closing, Judge Rondolino warned the plaintiff and its counsel, the Law Offices of Marshall Watson, that any new complaint must be verified, in accordance with the revised Florida Rules of Civil Procedure.

Judge Rondolino then warned very plainly, “If it is thereafter determined that the verification was not based on an appropriate investigation or that the allegations were false, the Plaintiff and the person who signed the verified complaint will be subject to sanctions which may include dismissal of the action with prejudice, assessment of fees and costs, monetary or incarcerative sanctions and referral to the State Attorney for prosecution pursuant to F.S. 837.”

Rondolino’s concerns arose in part because the Assignment came after the foreclosure action was filed. Plaintiff’s law firm is one of four law firms under investigation by the Florida Attorney General for using forged and fraudulent documents in foreclosure actions.

Scott Anderson of Ocwen has been named in foreclosure opinions of Brooklyn Judge Arthur M. Schack as an individual who signs using many different job titles. The trust in this case had a closing date in 2001, but according to the Anderson Assignment, acquired Decker’s non-performing loan in February, 2010. These same or similar facts have been presented in hundreds of foreclosure cases across the country.

Almost every major robo-signer, including Liquenda Allotey, China Brown, Linda Green, Alfonzo Greene, Korell Harp, Bethany Hood and John Kennerty have signed as Attorney-In-Fact for New Century Mortgage Corporation in 2009 and 2010 to transfer mortgages to securitized trusts that closed years earlier.

Judge Rondolino’s opinion lays a blueprint for other judges to follow when presented with mortgage assignments that appear to have been specially created to facilitate foreclosures. It is the first opinion in Florida to warn of possible “incarcerative sanctions.” (Five different versions of the “Scott Anderson” signature are posted in the “Pleadings” section of this web site.)

Today the Florida Attorney General issued Subpoenas Duces Tecum’s to both Lender Processing Services Inc. and to a subsidiary DOCX. This involves employees past or present, the four foreclosure firms currently being investigated.

Both Assistant AG’s “McCollum’s Angels” June Clarkson and Theresa Edwards are doing an outstanding job!

STATE OF FLORIDA

OFFICE OF THE ATTORNEY GENERAL

DEPARTMENT OF LEGAL AFFAIRS

______________________________________

ECONOMIC CRIMES

INVESTIGATIVE SUBPOENA DUCES TECUM

“You,” “Your” or “DOC X” as used herein means DOCX, L.L.c. and any ofthe respondents, their agents and employees or any “affiliate” of the aforementioned entities, as that term is herein defined. Your agents include but are not limited to your officers, directors, attorneys, accountants, CPA’s, advertising consultants, or advertising account representatives. Any document in the possession ofyou, your affiliates, your agents or your employees is deemed to be within your possession or control. You have the affirmative duty to contact your agents, affiliates and employees and to obtain documentation from them, if such documentation is responsive to this subpoena.

B. Unless otherwise indicated, documents to be produced pursuant to this subpoena should include all original documents prepared, sent, dated, received, in effect, or which otherwise came into existence at any time. If your “original” is a photocopy, then the photocopy would be and should be produced as the original.

C. This subpoena duces tecum calls for the production of all responsive documents in your possession, custody or control without regard to the physical location ofsaid documents.

D. “And” and “or” are used as terms of inclusion, not exclusion.

E. The documents to be produced pursuant to each request should be segregated and specifically identified to indicate clearly the particular numbered request to which they are responsIve.

F. In the event that you seek to withhold any document on the basis that is properly entitled to some privilege or limitation, please provide the following information:

1. A list identifying each document for which you believe a limitation exists;

2. The name of each author, writer, sender or initiator of such document or thing, if any;

3. The name of each recipient, addressee or party for whom such document or thing was intended, ifany;

4. The date of such document, if any, or an estimate thereof so indicated if no date appears on the document;

5. The general subject matter as described in such document, or, if no such description appears, then such other description sufficient to identify said document; and

6. The claimed grounds for withholding the document, including, but not limited to, the nature of any claimed privilege and grounds in support thereof.

G. For each request, or part thereof, which is not fully responded to pursuant to a privilege, the nature of the privilege and grounds in support thereof should be fully stated.

H. If you possess, control or have custody of no documents responsive to any of the numbered requests set forth below, state this fact in your response to said request.

1. For purposes of responding to this subpoena, the term “document” shall mean all writings or stored data or information ofany kind, in any form, including the originals and all nonidentical copies, whether different from the originals by reason of any notation(s) made on such copies or otherwise, including, without limitation: correspondence, notes, letters, telegrams, minutes, certificates, diplomas, contracts, franchise agreements and other agreements, brochures, pamphlets, forms, scripts, reports, studies, statistics, inter-office and intra-office communications, training materials, analyses, memoranda, statements, summaries, graphs, charts, tests, plans, arrangements, tabulations, bulletins, newsletters, advertisements, computer printouts, teletype, telefax, microfilm, e-mail, electronically stored data, price books and lists, invoices, receipts, inventories, regularly kept summaries or compilations of business records, notations of any type of conversations, meetings, telephone or other communications, audio and videotapes; electronic, mechanical or electrical records or representations of any kind (including without limitation tapes, cassettes, discs, magnetic tapes, hard drives and recordings to include each document translated, if necessary, through detection devices into reasonably usable form).

1. For purposes of responding to this subpoena, the term “affiliate” shall mean: a corporation, partnership, business trust, joint venture or other artificial entity which effectively controls, or is effectively controlled by you, or which is related to you as a parent or subsidiary or sibling entity. “Affiliate” shall also mean any entity in which there is a mutual identity of any officer or director. “Effectively controls” shall mean having the status of owner, investor (if 5% or more of voting stock), partner, member, officer, director, shareholder, manager, settlor, trustee, beneficiary or ultimate equitable owner as defined in Section 607.0505(11)(e), Florida Statutes.

K. The term “Florida affiliates” shall mean those of your affiliates which do business in Florida or which are licensed to do business in Florida.

L. If production of documents or other items required by this subpoena would be, in whole or in part, unduly burdensome, or if the response to an individual request for production may be aided by clarification of the request, contact the Assistant Attorney General who issued this subpoena to discuss possible amendments or modifications of the subpoena, within five (5) days of receipt ofsame.

M. Documents maintained in electronic form must be produced in their native electronic form with all metadata intact. Data must be produced in the data format in which it is typically used and maintained. Moreover, to the extent that a responsive Document has been electronically scanned (for any purpose), that Document must be produced in an Optical Character Recognition (OCR) format and an opportunity provided to review the original Document. In addition, documents that have been electronically scanned must be in black and white and should be produced in a Group IV TIFF Format (TIF image format), with a Summation format load file (dii extension). DII Coded data should be received in a (Comma-Separated Values) CSV format with a pipe (I) used for multivalue fields. Images should be single page TIFFs, meaning one TIFF file for each page of the Document, not one .tifffor each Document. Ifthere is no text for a text file, the following should be inserted in that text file: “Page Intentionally Left Blank.”

Moreover, this Subpoena requires all objective coding for the production, to the extent it exists. For electronic mail systems using Microsoft Outlook or LotusNotes, provide all responsive emails and, if applicable, email attachments and any related Documents, in their native file format (i.e., .pst for Outlook personal folder, .nsf for LotusNotes). For all other email systems, provide all responsive emails and, if applicable, email attachments and any related Documents in OCR and TIFF formats as described above.

P. The relevant time period for the present request shall be from January 1, 2006 to present unless otherwise specifically stated. YOU ARE HEREBY COMMANDED to produce at said time and place all documents, as defined above, relating to the following subjects:

1. Copies ofall “Network Agreements” between DOCX and any law firm with offices located in the State of Florida.

2. Copies of any and all underlying documentation that allows for your employee or ex-employee, Linda Green to sign documents in the following capacities:

a. Vice President of Loan Documentation, Wells Fargo Bank, N.A. successor by merger to Wells Fargo Home Mortgage, Inc.; ;

b. Vice President, Mortgage Electronic Registration Systems, Inc. as nominee for American Home Mortgage Acceptance, Inc.;

c. Vice President, American Home Mortgage Servicing as successor-in-interest to Option One Mortgage Corporation;

d. Vice President, Mortgage Electronic Registration Systems, Inc. as nominee for American Brokers Conduit;

e. Vice President & Asst. Secretary, American Home Mortgage Servicing, Inc., as servicer for Ameriquest Mortgage Corporation;

f. Vice President, Option One Mortgage Corporation;

g. Vice President, Mortgage Electronic Registration Systems, Inc. as nominee for HLB Mortgage;

h. Vice President, American Home Mortgage Servicing, Inc.;

1. Vice President, Mortgage Electronic Registration Systems, Inc. as nominee for Family Lending Services, Inc.;

J. Vice President, American Home Mortgage Servicing, Inc. as Successor -ininterest to Option One Mortgage Corporation;

k. Vice President, Argent Mortgage Company, LLC by Citi Residential Lending, Inc., attorney-in-fact;

m. Vice President, Amtrust Funsing (sic) Services, Inc., by American Home Mortgage Servicing, Inc., as Attorney-in -fact;

n. Vice President, Seattle Mortgage Company.

3. Copies of every document signed in any capacity by Linda Green.

4. Copies of any and all underlying documentation that allows for your employee or ex-employee, Korell Harp to sign documents in any capacity for any lender and/or servicing company.

5. Copies of any and all underlying documentation that allows for your employee or ex-employee, Jessica Ohde to sign documents in any capacity for any lender and/or servicing company.

6. Copies of any and all underlying documentation that allows for your employee or ex-employee, Pat Kingston to sign documents in any capacity for any lender and/or servicing company.

7. Copies of any and all underlying documentation that allows for your employee or ex-employee, Christina Huang to sign documents in any capacity for any lender and/or servicing company.

8. Copies of any and all underlying documentation that allows for your employee or ex-employee, Tywanna Thomas to sign documents in any capacity for any lender and/or servicing company.

9. All policy and procedure manuals and/or training materials regarding the methods and timing that DOCX uses, including without limitation relating to the drafting and/or execution of foreclosure and mortgage related documents, including but not limited to Assignments of Mortgage, Satisfactions ofMortgage and Affidavits ofany and all kind.

10. A list ofall employees, dates ofhire and termination, and their duties, including whether or not they provide any notary services for DOCX.

11. All documents in your possession regarding any contracts with Florida Default Law Group, P.L., The Law Offices of David J. Stem, P.A., Shapiro & Fishman, L.L.P. and The Law Offices of Marshall C. Watson, P.A., including contracts regarding payments to or from any of those entities.

12. Documents relating to the relationship between DOCX and NewTrac and/or NewInvoice, including but not limited to, documents relating to the types ofdocuments that are or can be generated or are requested to be generated.

13. Any price lists published in any manner to prospective customers, whether by printed or electronic means.

14. All communications between DOCX and Florida Default Law Group, P.L., The Law Offices of David J. Stem, P.A., Shapiro & Fishman, L.L.P. or The Law Offices ofMarshall C. Watson, P.A. relating to procedures, policies, instructions or performance ofthe creation, backdating, modification, amendment, or other alteration ofany real property-related transactional document or records, including assignments, satisfactions ofmortgage, affidavits, notes, allonges, or other documents filed in any court.

15. Ledgers ofall financial transactions between DOCX and Florida Default Law Group, P.L., The Law Offices of David J. Stem, P.A., Shapiro & Fishman, L.L.P. or The Law Offices of Marshall C. Watson, P .A.

16. Ledgers ofall financial transactions between DOCX and any title company, recording service, process server, or any other entity that provides payments to DOCX in connection with any services rendered in connection with any residential foreclosure.

17. Ledgers ofall financial transactions between DOCX and any title company, recording service, process server, or any other entity to whom DOCX provides payment(s) in connection with any services rendered in connection with any residential foreclosure.

WITNESS the FLORIDA OFFICE OF THE ATTORNEY GENERAL in Fort Lauderdale, Florida, this 13th day of October, 2010.

June M. Clarkson

Assistant Attorney General

Florida Bar Number: 785709

OFFICE OF THE ATTORNEY GENERAL 110 S.E. 6th Street, 10th Floor

Fort Lauderdale, Florida 33301

Telephone: 954-712-4600

Facsimile: 954-712-4658

Theresa B. Edwards

Assistant Attorney General

Florida Bar Number: 252794

NOTE: In accordance with the Americans with Disabilities Act of 1990, persons needing a special accommodation to participate in this proceeding should contact George Rudd, Assistant Attorney General at (954) 712-4600 no later than seven days prior to the proceedings. Ifhearing impaired, contact the Florida Relay Service 1-800-955-8771 (TDD); or 1-800-955-8770 (Voice), for assistance.

AUTHORITY

Florida Statute 501.206

501.206 Investigative powers of enforcing authority.(

1) If, by his own inquiry or as a result ofcomplaints, the enforcing authority has reason to believe that a person has engaged in, or is engaging in, an act or practice that violates this part, he may administer oaths and affinnations, subpoena witnesses or matter, and collect evidence. Within 5 days excluding weekends and legal holidays, after the service ofa subpoena or at any time before the return date specified therein, whichever is longer, the party served may file in the circuit court in the county in which he resides or in which he transacts business and serve upon the enforcing authority a petition for an order modifying or setting aside the subpoena. The petitioner may raise any objection or privilege which would be available under this chapter or upon service of such subpoena in a civil action. The subpoena shall infonn the party served of his rights under this subsection.

(2) If matter that the enforcing authority seeks to obtain by subpoena is located outside the state, the person subpoenaed may make it available to the enforcing authority or his representative to examine the matter at the place where it is located. The enforcing authority may designate representatives, including officials ofthe state in which the matter is located, to inspect the matter on his behalf, and he may respond to similar requests from officials ofother states.

(3) Upon failure ofa person without lawful excuse to obey a subpoena and upon reasonable notice to all persons affected, the enforcing authority may apply to the circuit court for an order compelling compliance.

(4) The enforcing authority may request that the individual who refuses to comply with a subpoena on the ground that testimony or matter may incriminate him be ordered by the court to provide the testimony or matter. Except in a prosecution for perjury, an individual who complies with a court order to provide testimony or matter after asserting a privilege against selfincrimination to which he is entitled by law shall not have the testimony or matter so provided, or evidence derived there from, received against him in any criminal investigation proceeding.

(5) Any person upon whom a subpoena is served pursuant to this section shall comply with the tenns thereof unless otherwise provided by order of the court. Any person who fails to appear with the intent to avoid, evade, or prevent compliance in whole or in part with any investigation under this part or who removes, destroys, or by any other means falsifies any documentary material in the possession, custody, or control of any person subject to any such subpoena, or knowingly conceals any relevant infonnation with the intent to avoid, evade, or prevent compliance shall be liable for a civil penalty of not more than $5,000, reasonable attorney’s fees, and costs.