MERS was created in 1995 under the auspices of the Mortgage Bankers Association (MBA), as the mortgage industry’s utility, to streamline the mortgage process by using electronic commerce to eliminate paper. Our Board of Directors and shareholders are comprised of representatives from the MBA, Fannie Mae, Freddie Mac, large and small mortgage companies, the American Land Title Association (ALTA), the CRE Finance Council, title underwriters, and mortgage insurance companies.

Our initial focus was to eliminate the need to prepare and record assignments when trading mortgage loans. Our members make MERS the mortgagee and their nominee on the security instruments they record in the county land records. Then they register their loans on the MERS® System so they can electronically track changes in ownership over the life of the loans. This process eliminates the need to record assignments every time the loans are traded. Over 3000 MERS members have registered more than 65 million loans on the MERS® System, saving the mortgage industry hundreds of millions of dollars in the process. The Federal Housing Administration (FHA) and Veterans Administration (VA) approved MERS for government loans because they recognized the value to consumers. On table-funded loans, MERS eliminates the cost to the consumer of the mortgage assignment ($30 – $150). In addition, the MERS process ensures that lien releases are not delayed by eliminating potential breaks in the chain of title. Similar to the residential product, we also addressed the assignment problem in the commercial market with MERS® Commercial, on which is registered over $110 billion in Commercial Mortgage-Backed Securities (CMBS) loans.

More than 60 percent of existing mortgages have an assigned MIN, making a total of 65,000,000 loans registered since the inception of the system in 1997. The corresponding data for these mortgages is tracked on the MERS® System from origination through sale and until payoff. MERS therefore offers a substantial base of historical data about existing loans that can be harnessed to bring transparency to existing MBS products. Attached are letters from the MBA, FHA, Fannie Mae and Freddie Mac on this point.

A good piece at Mother Jones, “Fannie and Freddie’s Foreclosure Barons” (hat tip Foghorn Leghorn) provides a window on a seamy big business: cut rate foreclosure processing machines that routinely ride roughshod over borrowers and the law.

Unfortunately, space limitations prevent the story from going deeply into some critical issues. The piece does a good job of explaining how these cut rate legal services operations are creations of Fannie and Freddie and illustrating how they are engaging in fabricating documents. The story focuses on a specific bad actor, a law firm founded by David Stern that handles roughly 1/5 of the foreclosures in Florida:

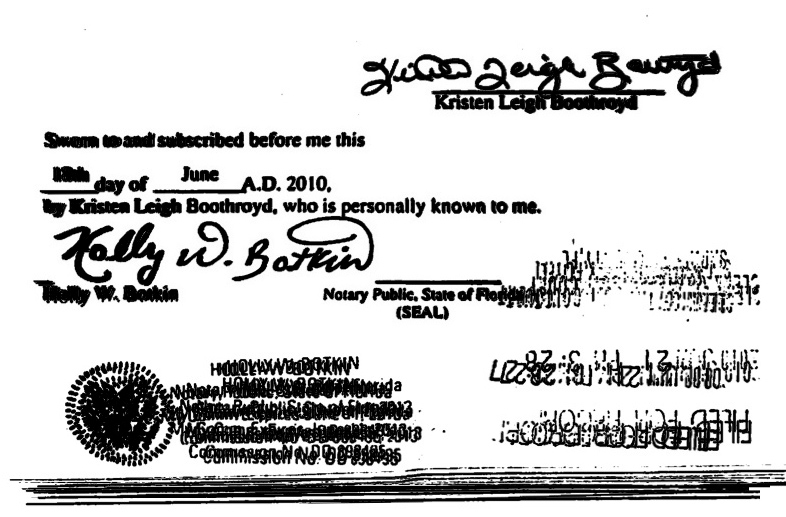

Ariane Ice sat poring over records on the website of Florida’s Palm Beach County…She and her husband, Tom, an attorney, ran a boutique foreclosure defense firm called Ice Legal…. Ice had a strong hunch that Stern’s operation was up to something, and that night she found her smoking gun.

It involved something called an “assignment of mortgage,” the document that certifies who owns the property and is thus entitled to foreclose on it….By law, a firm must execute (complete, sign, and notarize) an assignment before attempting to seize somebody’s home.

A Florida notary’s stamp is valid for four years, and its expiration date is visible on the imprint. But here in front of Ice were dozens of assignments notarized with stamps that hadn’t even existed until months—in some cases nearly a year—after the foreclosures were filed. Which meant Stern’s people were foreclosing first and doing their legal paperwork later. In effect, it also meant they were lying to the court—an act that could get a lawyer disbarred or even prosecuted. “There’s no question that it’s pervasive,” says Tom Ice of the backdated documents—nearly two dozen of which were verified by Mother Jones. “We’ve found tons of them.”

This all might seem like a legal technicality, but it’s not. The faster a foreclosure moves, the more difficult it is for a homeowner to fight it—even if the case was filed in error. In March, upon discovering that Stern’s firm had fudged an assignment of mortgage in another case, a judge in central Florida’s Pasco County dismissed the case with prejudice—an unusually harsh ruling that means it can never again be refiled. “The execution date and notarial date,” she wrote in a blunt ruling, “were fraudulently backdated, in a purposeful, intentional effort to mislead the defendant and this court.”…

But the Ices had uncovered what looked like a pattern, so Tom booked a deposition with Stern’s top deputy, Cheryl Samons, and confronted her with the backdated documents—including two from cases her firm had filed against Ice Legal’s clients. Samons, whose counsel was present, insisted that the filings were just a mistake. She refused to elaborate, so the Ices moved to depose the notaries and other Stern employees whose names were on the evidence. On the eve of those depositions, however, the firm dropped foreclosure proceedings against the Ices’ clients.

It was a bittersweet victory: The Ices had won their cases, but Stern’s practices remained under wraps. “This was done to cover up fraud,” Tom fumes. “It was done precisely so they could try to hit a reset button and keep us from getting the real goods.”

Backdated documents, according to a chorus of foreclosure experts, are typical of the sort of shenanigans practiced by a breed of law firms known as “foreclosure mills.” ….The mills think “they can just change things and make it up to get to the end result they want, because there’s no one holding them accountable,” says Prentiss Cox, a foreclosure expert at the University of Minnesota Law School. “We’ve got these people with incentives to go ahead with foreclosures and flood the real estate market.”

Yves here. This is far from the only form of document forgeries. A widespread abuse is what bankruptcy attorney Max Gardner calls the “alphabet problem.”

Mortgage securitizations were very carefully designed to satisfy a number of concerns. One of them was bankruptcy remoteness, that if an originator failed, as Countrywide, New Century, IndyMac and a host of others did, that the creditors in the bankruptcy would not be able to claw mortgages back out of securitizations (assets sold close to the date of a bankruptcy may be deemed to have been conveyed fraudulently, and thus can be seized by the court on behalf of the creditors).

To prevent this from occurring, the Pooling and Servicing Agreement (the master document that governs the securitization) would provided for a minimum of two independent legal entities to sit between the originator and the trust that would hold the mortgages being securitized (technically, the note, which is the IOU; the mortgage, which is a lien, follows the note in 45 states). So the prescribed minimum number of steps was A (originator) => B => C => D (trust). Some securitizations (for reasons unrelated to establishing bankruptcy remoteness) would provide for even more steps.

Keep in mind that the PSA also required that the notes be conveyed to the trust, with the proper chain of endorsements, by closing; certain exceptions and fixes were permitted up to 90 days after closing, but these would be applicable only to a very small proportion of the pool.

Chain-of-title is not just an issue for the buyers and sellers of particular homes and title insurance companies. Some entity – and most likely several entities – are claiming these mortgages and loans

as assets when regulators and investors are determining solvency and compliance, but disavowing these same “assets” when acknowledgement of ownership would result in responsibilities ranging from payment of taxes to lawn mowing.

Stern employees often sign as if a bankrupt or out-of-business company or a failed bank owned the mortgage and loan up until foreclosure is imminent. In county recorders’ offices across the state, the Stern-created records show that the trusts acquired mortgages and loans on dates when no such acquisitions ever took place. The trusts claim ownership solely to prove that they have the right to foreclose. The date selected is arbitrary – chosen by Stern or LPS or the mortgage servicing company. In reality, residential mortgage-backed trusts did not rush to acquire billions of dollars in sub-prime non-performing loans in 2008 and 2009 as these assignments falsely state.

This is the follow up to the latest Depositions posted on SFF taken from The Law Offices of David J. Sterns’ employees Cheryl Samons and Shannon Smith.

In every foreclosure case, there are at least one, possibly two, points at which a legal notice must be published. In every foreclosure case, the notice of sale must be published in a local newspaper twice before the sale (Fla. Stat. § 45.031 (2)) and in some cases, if the owner of the property cannot be found, the plaintiff can serve by publication in the newspaper instead of having a process server deliver it personally.

But no matter what, any time a legal notice is published in a newspaper, some representative of the newspaper must provide a “Proof of Publication” affidavit, swearing that the ad was published on the dates indicated, and that the newspaper meets certain specified legal requirements.

In the Tampa Bay area, there is one newspaper that handles the legal notices for almost every foreclosure case: the Gulf Coast Business Review. And just last night, I had the opportunity to take a look at several of the “proof of publication” affidavits produced by that particular newspaper. You’ll be shocked at what I found.

Two things looked suspicious about the signatures on the affidavits. First, they were extremely uniform – almost identical. Second, the notary’s signature blocked out the signature line. Underneath the signature, instead of a line, there was just white space. These are classic signs of digital manipulation.

So I grabbed six different affidavits in a series of related foreclosure sales in Sarasota County. Once I had the digital images, I was able to copy the signature block by itself from each one, and digitally overlay them to see just how alike they were. One by one, the signatures shows themselves to be…

Every letter on every affidavit, whether typed or signed, fell in exactly the same place on each sheet of paper – except the notary stamp. What does this mean? The affidavits aren’t affidavits at all – they’re computer-generated images that some foolish notary has been stamping her seal on. Knowing the volume of legal ads run by this paper, they’re probably generating hundreds of them for every issue.

And here’s the problem:

A notary public may not sign notarial certificates using a facsimile signature stamp unless the notary public has a physical disability that limits or prohibits his or her ability to make a written signature and unless the notary public has first submitted written notice to the Department of State with an exemplar of the facsimile signature stamp….

A notary public may not notarize a signature on a document if the person whose signature is being notarized is not in the presence of the notary public at the time the signature is notarized. Any notary public who violates this subsection is guilty of a civil infraction, punishable by penalty not exceeding $5,000, and such violation constitutes malfeasance and misfeasance in the conduct of official duties. It is no defense to the civil infraction specified in this subsection that the notary public acted without intent to defraud. A notary public who violates this subsection with the intent to defraud is guilty of violating s. 117.105.

Fla. Stat. § 117.107 (2) & (9) Mass-producing affidavit signatures like this, by computer, is flatly illegal. And if that’s what is really happening over at the Gulf Coast Business Review, this business is about to take a very interesting turn – for the worse. And for homeowners, it means one more chink in the armor, one more place to attack, one argument of last resort, before the sheriff comes to remove you from your home.

As a manager with the Los Angeles County Registrar Recorder, I am in charge of the software development team who creates applications to handle property document recording. Whenever one buys, sells or refinances a house or land, property documents are generated. These documents must be submitted to a County Recorder for storage and indexing to be made available as a public record. Los Angeles County – having well over 10 million residents – is the most populous county in the United States and contains 88 separate cities. As such, my office records – or processes – over 2 million property document recordings per year. Until now, each one of those documents must be brought in by hand, looked over, entered into our application and then scanned for permanent storage. (The current system was brought online in January 2007, as documented by this video: ELECTRONIC RECORDING ARCHIVE – 2007)The transport, handling and mailing back of paper documents is an overwhelming task. It is also very expensive both in terms of labor and time. For years, the various county Recorder offices wished to pursue something more streamlined. With the advent of newer, less expensive and more accessible technology, the possibility of scanning in documents at the title company (http://en.wikipedia.org/wiki/Title_insurance) offices and electronically sending these documents to the county offices is a reality. State law, however, impeded the process for many years. Up until today, only Orange and San Bernardino counties were allowed by law to electronically record title company documents. In order to change this, several County Recorders worked with the State Legislature and Attorney General office to pass a law (AB 578 – http://ag.ca.gov/erds1/) entitled the Electronic Recording Delivery Act, which enabled a statewide standard and governance for an Electronic Recording Delivery System (ERDS). Los Angeles decided to partner with Orange, Riverside and San Diego counties to move forward with an in-house developed system, which allowed for economies of scale, flexible implementation and leveraged the 10-year electronic recording experiences of the Orange County Clerk-Recorder. The new system was dubbed, SECURE. It was developed by in-house staff, along with a contractor, who also maintains (as a vendor) the current Orange County recorder system. All four counties own the software and work together to move forward with improvements.[CLICK ABOVE FOR LARGER IMAGE]The above screen shows the common submitter client to be used by title companies, service providers and other institutions in order to submit documents. In this case a Deed is being prepared to be sent to Los Angeles County. The submitter – if authorized – is able to send these documents to any county in the system.Each county participating in the SECURE system is able to leverage the infrastructure built for the system and hosted at the Orange County data center. This data center is a purpose-built facility designed for extreme reliability and high availability. All title companies and other submitters – such as banks – will submit documents through an encrypted Internet connection to the Orange County data center. The documents will be held there until the various participating county recorders pick them up and process them.The structure will look similar to this:All submitters – Financial Institutions such as banks, Title Companies and eventually governmental departments such as the IRS and SSA –are able to use the common client, submit to the common data center and be assured that their documents are routed to the appropriate County Recorder.The system started out on December 1, 2009 with only Orange and Los Angeles counties active. Within six months, it is expected that other counties will be brought online. As the system is enhanced and developed title companies will be allowed to submit more documents and eventually scale back their paper handling processes altogether.This will result in a decrease in costs to the title companies as well as to the counties as a result of paper handling efficiencies. Of the two million annual documents recorded and by the Los Angeles County Recorder, 60% will be able to be processed eventually through this system. Since each document must currently be mailed back to the customer by the recorder, an annual savings in postage and mail handling is expected to show efficiencies.Once the document has been submitted to the Recorder office, it will be examined and – if valid – accepted for recording. The document will be stored in the recording archive and is available for further activities as needed by the general public.[CLICK ABOVE FOR A LARGER IMAGE]After the document has been recorded, the lead sheet (in the case of LA County, who attaches a separate sheet to the front of each document) and the first page are returned to the submitter. They are then able to print and mail the document back to the customer.[CLICK ABOVE FOR A LARGER IMAGE]As seen in the above image, the recorded document has been automatically returned to the submitter. At this stage, the process is complete for the county recorder.Since the SECURE (www.secure-erds.com) group owns the software, the counties will be free to upgrade and enhance the software to fit future needs. These future processes will include an interface to allow banking institutions direct access to send documents such as reconveyances and liens directly from their internal systems. This will further reduce costs as those documents are currently delivered via certified mail. Further enhancements will include electronic delivery of notary signatures, when that becomes allowed in the state. Because the system is built to abstract the back-end recording system from the delivery system, any number of California counties are able to join as participants and leverage the infrastructure already built by Orange, LA, Riverside and San Diego counties.

In accordance with Title 17 U.S.C. Section 107, any copyrighted work in this

message is distributed under fair use without profit or payment for non-profit

research and educational purposes only. GRG [Ref.http://www.law.cornell.edu/uscode/17/107.shtml]

(2)")

")

{kind=link}

Recent Comments