Illinois: Foreclosure case lost – but be careful using TILA violations claims. . .

h/t “KC”

Deutsche Bank National Trust Co. v. Gilbert, 2012 IL App (2d) 120164

A judgment of foreclosure and order confirming the foreclosure sale vacated and the foreclosure action dismissed on the ground that plaintiff bank did not own the mortgage at the time the action was filed. But plaintiff bank, as an assignee, was not liable on defendant’s counterclaim alleging a violation of the TILA, since the alleged violation was not apparent on the face of the documents.

Deutsche Bank National Trust Company, filed a foreclosure suit against James L. Gilbert. Gilbert raised the affirmative defense that Deutsche Bank lacked standing at the time it filed the suit.

Gilbert also filed a counterclaim alleging violations of TILA 15 U.S.C. § 1601 (2006) and seeking damages.

The parties filed cross-motions for summary judgment.

The trial court initially found in favor of Gilbert on the issue of standing and dismissed the foreclosure.

However, following Deutsche Bank’s motion for reconsideration, the trial court reversed itself and granted summary judgment in favor of Deutsche Bank on all claims.

Gilbert appeals, arguing the trial court’s initial decision was correct, and that he is also entitled to summary judgment in his favor on the counterclaim.

The judgment of foreclosure was reversed and the cause dismissed and affirmed dismissal of the TILA counterclaim.

“If I had a picture of the “God of Real Estate”, I would put a name tag on its “chest” that said “MERS” on it … because these people think they rule the world and that when its attorneys show up in court, I should sit in the corner and cower while they misrepresent the truth in court. . . . MERS can’t do anything on its own because it’s a fiction, so it brings in its parents, MERSCORP Holdings, Inc., then filed an action in a California District Court attempting to get a judge to reverse and toss a quiet title action and expungement orders granted by a state judge (CA) . . . A federal judge tossing a state court judgment to quiet title? Really? Apparently MERS’ counsel is so big for its britches it thinks it can order any judge to do its bidding.”

Wisconsin: “Coyle Rule” (h/t Neil Garfield (“KC”) for article re MGIC Financial v Briggs)

Property buyers (i.e., homeowners) have rights to seek personal judgments and be subrogated in cases where they did not consent to conduct occurring but that same conduct deprived them of equitable rights, including the right to pay off obligations.

“Equity requires that the surety, [the Davises], likewise be released from the burden of having to forfeit their land to satisfy a debt for which the principal debtor already has been released.”

This is a common theme of bad practice today wherein homeowners are not disclosed of the ‘secret’ transactions and parties ‘behind the scenes’ and thus have no choice nor options to protect and defend their homes – but yet forced to fight litigation resulting from the same secretive conduct, that in most cases, ends in the homeowner losing their homes anyhow because they cannot fight what they cannot see or have access.

Under the “Coyle Rule” (Coyle v. Davis, 20 Wis. 564 (1866)):

. . . “a release of the mortgagor’s personal liability will subordinate or even release the lien of the mortgage as to a subsequent mortgage holder.”

“Where a mortgagee has notice of a later purchaser of part of the mortgaged premises, the mortgagee’s release of the mortgagor’s personal liability diminishes the subrogation rights of the later purchaser and thereby operates to discharge the lien against that part of the premises sold to the later purchaser.” (Altabet v. Monroe Methodist Church, 1989)

“The court held that this removed any incentive on R’s part to pay the debt and the mortgage lien was therefore extinguished.” (Modern Mortgage Law and Practice by Robert Kratovil, 1972)

In (PRECEDENTIAL) MGIC FIN. v. HA Briggs Co., 600 P.2d 573 (Wash. Ct. App. 1979) Court of Appeals of Washington, Filed: August 9, 1979; Citations: 600 P.2d 573, 24 Wash. App. 1; 24 Wn. App. 1 (1979) 600 P.2d 573:

“As subsequent purchasers, the Davises had the right to pay off the deed of trust note and be subrogated to whatever rights MGIC, the senior lienor, had against Briggs — including the right to seek a personal judgment against Briggs. MGIC has stipulated that it had notice of the Davises’ interest in lot 5 when it released Briggs from personal liability on the note. There is no question that the Davises did not consent to the release, and that the release deprived the Davises of their equitable right to pay off the debt and seek a personal judgment against Briggs. Moreover, interest accrued on the outstanding principal at an annual rate of 16 percent for 39 months while MGIC delayed in joining the Davises as defendants. We hold that this situation caused sufficient prejudice to the Davises’ equitable rights to discharge the lien against their property under the Coyle rule.”

“An examination of many cases and authorities convinces us that the very great weight of authority supports the view that the release given by the [mortgagee] to [the grantee/principal] had the effect of discharging the [mortgagor/surety] from further liability on the deficiency judgment.”

See also Corkrell v. Poe, 100 Wash. 625, 628, 171 P. 522, 12 A.L.R. 1524 (1918); 2 L. Jones, Law of Mortgages of Real Property, § 742 (8th ed. 1928).

___

In MGIC v Briggs, et al:

Plaintiff MGIC Financial Corporation (MGIC), the beneficiary under a deed of trust, appeals from a summary judgment in its foreclosure suit against defendants Eddy and Margaret Davis. We affirm.

On February 9, 1970, H.A. Briggs Company (Briggs) executed a promissory note to MGIC for about $1.42 million. To secure the note, Briggs and another company, Enterprise Company, executed a deed of trust which covered several parcels of land in King and Pierce Counties. MGIC also secured a personal guaranty on the note from Walter and Christine Kassuba. The note and deed of trust were recorded in both King and Pierce Counties.

On June 29, 1971, Enterprise conveyed one of the encumbered parcels, lot 5, to Eddy and Margaret Davis, for about $8,000. Although the preliminary title report disclosed MGIC’s interest, there was no assumption of it by Davis.

In 1973 payments on the note became delinquent, and on December 21, 1973, the Kassubas and the two companies went into bankruptcy. On the same date, MGIC filed a lawsuit in King County against Briggs, based on the 1970 note and deed of trust, and another lawsuit in Florida, against the Kassubas, based on their personal guaranty on the note. MGIC did not join the Davises as defendants in the foreclosure action, even though it found out in January 1974 that the Davises owned lot 5.[1]

On May 31, 1974, MGIC, Briggs and the Kassubas reached a written settlement agreement. The agreement provided, in part:

(a) The Property shall be conveyed absolutely to MGIC, free and clear of all liens and encumbrances .. .

(b) Following such conveyance, MGIC shall cause all pending litigation against KASSUBA, as aforesaid, to be dismissed with prejudice.

(c) The aforesaid Deed of Trust Note (Exhibit “A”) and Deed of Trust (Exhibit “B”) shall be cancelled and satisfied of record and all parties shall be relieved of any further liability thereunder, whether as maker or guarantor.

In December 1974, pursuant to the May 1974 settlement agreement, most of the encumbered parcels were conveyed by quitclaim deed to MGIC. The parties have stipulated that the quitclaim deeds released Briggs from personal liability on the note and deed of trust. The Kassubas later were released from personal liability on August 20, 1975, when MGIC voluntarily dismissed its Florida lawsuit against them.

On April 4, 1977, more than three years after the original suit had been filed, MGIC amended its King County foreclosure complaint to join the Davises as defendants. On May 1, 1978, the trial court granted a motion for summary judgment in favor of the Davises and dismissed the complaint against them.

The trial court based its summary judgment upon the equitable rule set out in Coyle v. Davis, 20 Wis. 564 (1866): Where a mortgagee has notice of a later purchaser of part of the mortgaged premises, the mortgagee’s release of the mortgagor’s personal liability diminishes the subrogation rights of the later purchaser and thereby operates to discharge the lien against that part of the premises sold to the later purchaser.[2]

[2] In Coyle, as here, the mortgagor sold part of his mortgaged property by warranty deed to a purchaser. The mortgagor sold the remainder of the mortgaged property to a second purchaser. At the second sale the mortgagee, who knew about the first purchaser’s interest, nevertheless released the mortgagor from personal liability on the note, and agreed to look only to the second purchaser and to the encumbered land to secure the note. When the mortgagee later attempted to foreclose against the first purchaser’s property, the Wisconsin court barred the foreclosure, stating:

[The first purchaser of the mortgaged property] stands in the relation of a surety for [the mortgagor], and any agreement between [the mortgagee] and [the mortgagor] which operated to diminish [the purchaser’s] security or to increase her liability, was a release of all obligation on [the purchaser’s] part. The right of insisting upon the 5*5 personal liability of [the mortgagor] was one of the safeguards of [the purchaser’s] title, and, by voluntarily depriving [the purchaser] of that, [the mortgagee] deprived himself of the right of insisting upon the liens of his mortgages upon the lands owned by [the purchaser]. [The purchaser] is accordingly entitled to have them discharged.

Coyle v. Davis, supra at 568. The court pointed out that the first purchaser’s remedy under the covenant of warranty and the covenant against encumbrances — basically limited to the price paid for the property — would have been grossly inadequate because

the sums due upon the mortgages greatly exceed the price or value of the lands owned by [the purchaser], and she might be obliged to pay much more than the consideration money and interest in order to remove the incumbrances.

6*6 [3] We agree with the equitable principle expressed by the Wisconsin court in Coyle and Sexton, and we see no reason why it should not apply here. Subrogation is an equity extending to parties who, although not personally bound to pay a debt, are compelled to do so in order to protect their property interest. See G. Osborne, Mortgages, ch. 10, § 279, at 565 (2d ed. 1970); 73 Am.Jur.2d Subrogation § 3, at 600 (1974). Subrogation entitles the party paying the debt to all of the rights, priorities, liens and securities which the senior mortgagee had against the mortgagor. See Restatement of Security § 141 (1941); Restatement of Restitution § 162 (1937); 73 Am.Jur.2d Subrogation § 106, at 665 (1974).

As subsequent purchasers, the Davises had the right to pay off the deed of trust note and be subrogated to whatever rights MGIC, the senior lienor, had against Briggs — including the right to seek a personal judgment against Briggs. MGIC has stipulated that it had notice of the Davises’ interest in lot 5 when it released Briggs from personal liability on the note. There is no question that the Davises did not consent to the release, and that the release deprived the Davises of their equitable right to pay off the debt and seek a personal judgment against Briggs. Moreover, interest accrued on the outstanding principal at an annual rate of 16 percent for 39 months while MGIC delayed in joining the Davises as defendants. We hold that this situation caused sufficient prejudice to the

Davises’ equitable rights to discharge the lien against their property under the Coyle rule.[3]

This holding follows the spirit of the general rule of suretyship: Where a secured creditor surrenders to the debtor, negligently loses or damages the security, it discharges the surety to the extent of the value so lost. See American Law of Property § 16.141, at 332 n. 22 (1952); Restatement of Security § 132 (1941); H. Arant, Law of Suretyship and Guaranty §§ 62, 63, at 219 (1931). It also comports with the rule that the release of a principal, without consent of the surety, generally releases the surety. See Restatement of Security § 122 (1941). Washington implicitly adopted these basic principles in Insley v. Webb, 122 Wash. 98, 209 P. 1093, 41 A.L.R. 274 (1922), in which the principal debtor, an assuming grantee, had been released by the mortgagee from liability on a deficiency judgment. The court held that the release also absolved the mortgagor, who was a surety. The court stated at page 103:

An examination of many cases and authorities convinces us that the very great weight of authority supports the view that the release given by the [mortgagee] to [the grantee/principal] had the effect of discharging the [mortgagor/surety] from further liability on the deficiency judgment.

When MGIC took title to Briggs‘ property and released Briggs from personal liability pursuant to the May 1974 agreement, it in effect did the same thing that the mortgagee in Insley had done. That is, it released the principal debtor from liability on a deficiency judgment without the consent of the surety. Equity requires that the surety, the Davises, likewise be released from the burden of having to forfeit their land to satisfy a debt for which the principal debtor already has been released.

MGIC argues that the release of Briggs‘ personal obligation by itself causes insufficient prejudice to warrant application of the Coyle rule. It reasons that the Davises actually suffered no loss because they could not have paid off the 8*8 debt in the first place; and because even if they had paid the debt, they would have been subrogated to nothing more than the dubious right to seek a personal judgment against a bankrupt company. The Coyle and Sexton opinions, however, placed no minimum requirement as to the legal detriment to be incurred by the surety, and we find no such requirement in the cases or treatises which synopsize this rule. It is sufficient that there was a release, without which the Davises could have paid off the note and been subrogated to whatever rights MGIC had against Briggs‘ personal liability in federal bankruptcy court. MGIC bases its argument upon Scrivner v. Kansas City Life Ins. Co., 143 P.2d 619 (Okla. 1943). Contrary to MGIC’s assertions, the Scrivner court did acknowledge the rule that a surety will prevail where the mortgagee releases the mortgagor’s personal liability; the court found no occasion either to apply or reject the rule, however, because under the particular facts of the case, the junior interest holder had not lost even his subrogation rights. Scrivner v. Kansas City Life Ins. Co., supra at 621.

[4] In another assignment of error, MGIC argues that the trial court violated the “law of the case doctrine” by granting the motion for summary judgment several days after another trial judge had denied a similar motion. The law of the case doctrine generally applies only to parties who raise identical issues on successive appeals of the same case. Greene v. Rothschild, 68 Wn.2d 1, 10, 402 P.2d 356 (1965), 414 P.2d 1013 (1966); Pierce County v. Desart, 9 Wn. App. 760, 761 n. 1, 515 P.2d 550 (1973). MGIC presents no relevant authority for extending the doctrine to apply to motions raised several times at the trial court level. We see no reason to extend the doctrine here.[4]

Having examined the record submitted, we agree with the trial court’s conclusion that this case is ripe for summary judgment. It is undisputed that MGIC knew of the Davises’ surety interest. Yet without the Davises’ consent, MGIC garnered title to virtually all of the debtor’s real estate, released the debtor’s personal liability on the deed of trust note, and failed for more than 3 years to join the Davises as defendants in the foreclosure suit while interest steadily accrued on the debt. Whether by design or neglect, the net result of these omissions was decidedly one-sided in favor of MGIC. The trial court properly balanced the equities when it released the Davises from the danger of losing their land to satisfy the debt of a principal who already had been discharged of all liability.

The summary judgment in favor of the Davises is affirmed.

PETRIE and SOULE, JJ., concur.

Reconsideration denied August 29, 1979.

Review denied by Supreme Court November 30, 1979.

[1] On October 15, 1974, one of MGIC Financial Corporation’s attorneys wrote to the Davises advising them that their property was subject to the deed of trust, and that they “hence would be a party to our lawsuit if a foreclosure is necessary.” The letter, however, did not mention that the foreclosure suit already had been filed more than 9 months before.

[3] Although technically the Davises’ statutory warranty deed provided them with a remedy through the covenant against encumbrances, the remedy would have been inadequate in this case. The remedy for breach of the covenant against encumbrances is limited to the price paid for the property, plus interest. 7 G. Thompson, Law of Real Property § 3187, at 318-19 (1962 Repl.); 6 R. Powell, Law of Real Property § 907 (1979). The maximum recovery would have been dwarfed by the sum the Davises would have had to pay to clear the lien of the deed of trust from their title.

[4] The first trial judge denied the earlier summary judgment motion “without prejudice,” and reserved the right to require an additional pretrial conference, stating that “this case may be determined on the issues presented by the cases mentioned herein [i.e., Coyle v. Davis, 20 Wis. 564 (1866) and its related cases].” Several days later MGIC Financial Corporation paved the way for the second summary judgment motion by stipulating that it had notice of the Davises’ ownership interest in lot 5 when it released Briggs from personal liability on the 1970 note and deed of trust.

Of Course They ALL Knew! They also know about their own frauds…

Reuters-

Two senior officials at JPMorgan Chase & Co and predecessor companies repeatedly confronted Bernard Madoff over irregularities in his business, a new lawsuit said, suggesting that bank leaders had “direct knowledge” of his Ponzi scheme.

The lawsuit filed in federal court in Manhattan on Wednesday on behalf of shareholders against Chief Executive Jamie Dimon and 12 other current and former executives and directors was based in part by statements made by Madoff himself during a series of interviews.

“JPMorgan was uniquely positioned for 20 years to see Madoff’s crimes and put a stop to them,” the lawsuit said.

Like the rest of them in the past who disappointed us after vowing to do the same…I’ll believe it when I hear it!

American Banker-

No more Mr. Nice Guy.

That was the message that the Consumer Financial Protection Bureau’s No. 2 sent to mortgage servicers attending an industry conference on Wednesday. Steven Antonakes, the agency’s deputy director, said that servicers have had more than a year to prepare for a reform rule that took effect last month and suggested the CFPB would move quickly and harshly against violators.

Antonakes acknowledged that the agency has previously suggested it would be tolerant of mortgage servicing companies so long as they were making a “good-faith effort” to comply with the rule, but he warned that such allowances only extend so far.

WOW! Just WOW!! Will anyone care to investigate this matter?

WSJ-

As U.S. Bankruptcy Judge James Peck leaves the bench, one object is definitely going with him: a Lehman Brothers baby rattle.

Judge Peck, who presided over the Lehman Brothers bankruptcy, is joining law firm Morrison & Foerster LLP after stepping down from the Manhattan bankruptcy court. The rattle was purchased at an auction of Lehman memorabilia by a participant in the case who also was involved in the Residential Capital LLC Chapter 11 case, in which Judge Peck served as mediator.

Judge Peck spent thousands of hours over 5½ years working on Lehman’s U.S. bankruptcy case and related insolvency proceedings in courts around the world. More than 42,000 docket entries were filed in the case, the largest ever U.S. bankruptcy filing.

The one thing in life we seem to pay little attention to is our credit rating. Yet every month our credit rating is subject to change. Credit scores run from 350 all the way up to 850 generally; however, not one of us understands that the creditors we deal with actually control our credit histories and our lives, many times for the worse.

Any time you fill out a credit application … anywhere … and the creditor runs a check of your credit … an inquiry appears on your credit report. An inquiry is generally a computer coded entry that lists the name of the creditor (and sometimes a code number) and the date the credit report was pulled. Too many of these inquiries in a short period of time will actually reduce your credit score, but not many people know that applying for credit all over town is not a good thing.

As I’ve said in previous posts: There’s no such thing as “good credit” as opposed to what we all know as “bad credit”!

Washington (state): Bradburn v ReconTrust; Bank of America – won using the Constitution.

As a follow-up to the judge’s commentary “. . . under what authority did MERS have the right to name that trustee?” – what authority indeed.

Read the Motion for [Partial] Summary Judgment, Opposition and Reply to understand how Scott Stafne, Esq., attorney for Bradburn, used the Constitution and powerful, straightforward language to prevail in this case:

“This Court should grant Mr. Bradbum a partial summary judgment that ReconTrust, clothed by defendants BANA [Bank of America] and Fannie Mae, misused the immense power granted under the DTA [Deed of Trust Act] and through their actions caused Bradbum damages by wrongfully “stealing” Bradbum’s home in violation of the aforementioned provisions of the DTA, and that defendants are liable for such damages as a jury determines. Further, this Court should grant Mr. Bradbum a partial summary judgment that defendants misuse of the DTA and related robosigning practices constituted violations of the CPA [Consumer Protection Act] for which defendants are liable.”

In attorney Scott Stafne’s Reply to ReconTrust’s Opposition:

“. . . Default is not a defense to unlawful use of non-judicial foreclosure. If the Defendants could have lawfully foreclosed then they should have done so. Further, unlawful foreclosure, not default, has unlawfully deprived Bradburn of use and enjoyment of the property. . .”

In our Veteran’s Protection Project, TV5 is looking for veterans who served our country, only to face foreclosure, housing or medical problems on their return from active duty.

Imagine serving your country for years and returning home to find out the bank was foreclosing on your house.

That’s exactly what happened to one Mid-Michigan soldier.

On Tuesday, that soldier was in Bay City Federal Court fighting the foreclosure, saying his rights as a U.S. service member were violated.

To better understand a case is to read, read, read. The series of complaints (amended) in this case is a good example of language for Colorado cases in these regards.

It is not enough to simply regale over the opinions – studying the documents that were initially filed is where all the valuable lessons are – wins and losses! Read the losses to learn what to avoid and the good on what to expound upon.

BE SURE TO CAREFULLY REVIEW EVERY EXHIBIT . . .A LOT OF VALUABLE INFO CAN BE GLEANED FROM THE EXHIBITS!

UNITED STATES BANKRUPTCY COURT FOR THE CENTRAL DISTRICT OF CALIFORNIA SANTA ANA DIVISION

In re TRUDY KALUSH, Reorganized Debtor.

____________________

TRUDY KALUSH, Plaintiff,

vs.

DEUTSCHE BANK NATIONAL TRUST COMPANY AS TRUSTEE OF THE INDYMAC INDX DEED OF TRUST LOAN TRUST 2005-AR12, DEED OF TRUST PASS-THROUGH CERTIFICATES, SERIES 2005-AR12, UNDER THE POOLING AND SERVICING AGREEMENT DATED JUNE 1, 2005; ONEWEST BANK, FSB; and DOES 1-100, Inclusive, Defendants.

American International Group (AIG.N) is holding “hostage” an $8.5 billion deal to compensate investors who bought Bank of America Corp (BAC.N) mortgage securities, supporters of the deal said in court filings ahead of a hearing on Wednesday.

The supporters urged the judge overseeing the deal to reject AIG’s efforts to delay its approval, according to documents submitted to the court late on Friday.

Bank of America agreed to the settlement in June 2011 to resolve claims by investors who had bought $174 billion of mortgage-backed securities issued by Countrywide Financial before the U.S. housing crisis. The investors said Countrywide, acquired by Bank of America in 2008, misrepresented the quality of the underlying home mortgages, which went sour in the crisis.

Recently, our nation’s financial chieftains have been feeling a little unloved. Venture capitalists are comparing the persecution of the rich to the plight of Jews at Kristallnacht, Wall Street titans are saying that they’re sick of being beaten up, and this week, a billionaire investor, Wilbur Ross, proclaimed that “the 1 percent is being picked on for political reasons.”

Ross’s statement seemed particularly odd, because two years ago, I met Ross at an event that might single-handedly explain why the rest of the country still hates financial tycoons – the annual black-tie induction ceremony of a secret Wall Street fraternity called Kappa Beta Phi.

The banker suicide wave that started in late January has now become an epidemic, and it seems to be focusing on one bank: JP Morgan.

After the first suicide that took place in JPM’s London headquarters, ending the life of 39 year old Gabriel Magee, a vice president in the investment bank’s technology department, next it was 37 year old Ryan Crane, an executive director in the firm’s program trading division, who died under still unknown circumstances.

Moments ago a third JPMorgan banker committed suicide, this time at the JPMorgan Charter House Asia headquarters in central Hong Kong, where a 33 year old man who was said to have been an FX trader for JPM, just jumped to his death.

Not much is known yet about the circumstances of the suicide, however according to early reports, the man was 33-years-old, surnamed Lee, and believed to be a forex trader for JP Morgan.

Bank of America Corp. and HSBC Holdings Plc (HSBA) agreed to settle lawsuits brought over property insurance that borrowers were forced to accept, lawyers for the homeowners said at a federal court hearing in Miami.

The lawyers told U.S. District Judge Federico Moreno today about the settlements without disclosing more details. The deals follow an earlier $300 million agreement with JPMorgan Chase & Co. and a $110 million settlement with Citigroup Inc. (C) on the same issue.

So-called force-placed insurance is taken out on homes by banks or mortgage servicers when, for example, a homeowner’s policy lapses or the bank decides the borrower doesn’t have enough coverage. The homeowners alleged that the banks got a financial windfall by cutting deals with insurance companies and over-charging borrowers for the coverage.

Superior Court of the State of Washington for Snohomish County

GEORGE N. BOWDEN JUDGE

SNOHOMISH COUNTY COURTHOUSE 3000 Rockefeller Avenue, M/S #502 Everett, WA 98201-4060 (425) 388-3532

Abraham K. Lorber Lane Powell, PC 1420 Fifth Avenue, Suite 4100 Seattle, WA 98101

Scott E. Stafne Stafne Trumbull, LLC 239 North Olympic Avenue Arlington, WA 98223

January 30, 2014

Re: Bradburn v. ReconTrust, et al. | No. 11-2-08345-2

Dear Counsel: Enclosed please find copies of my order denying the defendant’s motion for summary judgment, granting plaintiff’s cross motion for partial summary judgment on his consumer protection claims, and granting plaintiff’s motion for partial summary judgment declaring the foreclosure sale to be void and setting it aside.

I chose not to enter specific findings or conclusions of law, since they are not required. And any appellate court will undoubtedly sort through the record and discuss those salient facts which may be pertinent to its decision on review.

However, I did want to share my reasoning for the decisions I entered.

Obviously, this is yet another convoluted case in the minefield of mortgage foreclosure litigation involving MERS. Most of the facts surrounding the procedural history are not in dispute.

While I recognize that the law is well-settled that a borrower like Mr. Bradburn generally does not have recourse when he’s denied a refinance loan, I was troubled by the allegation that he was told that he should stop making his mortgage payments so that he could qualify for refinancing with Bank of America (BANA) and that once he fell behind he not only wasn’t approved for that refinance but then found himself unable to bring his mortgage loan current or resolve what he believed was a dispute about how much he was behind. Of course, that’s not enough to prevail on a motion for summary judgment. And for purposes of these motions, it was accepted that he was in default on his loan. And there’s also no question that the loan documents allowed for the nonjudicial foreclosure sale of his home in the event of default.

I was not concerned with the fact that the sale was ultimately postponed more than 120 days by the trustee, since a new notice of foreclosure sale was had been issued. I could find nothing in the Deed of Trust Act (DTA) or case law which required the lender or trustee to start over by filing another notice of default. The Act forbids a sale less than 120 days after that notice of default. This sale was well beyond that. I also felt that there was ample proof that the required notices were issued and posted, notwithstanding Mr. Bradburn’s claims to the contrary. That’s not to say that the notices were correct or proper under the DTA.

What seems to have been intended as a fairly simple procedure to avoid the necessity of a judicial foreclosure, namely the DTA, might be made more complicated and confounding than in the case at bar but it is difficult for me to see how. The DTA seems to contemplate a borrower and a lender with an independent trustee having the power to foreclose on the deed of trust in the event of default by the borrower. The lender would normally hold the underlying note and be the beneficiary of it. Here matters have been complicated by the sale of the underlying note from HomeStar Lending to Countrywide, which was later acquired by BANA. Fidelity Title was identified as the trustee but then MERS was characterized as the beneficiary “as the nominee” of the lender and their assigns. At summary judgment it was claimed that the note was “owned” by Fannie Mae although it was “held” by BANA, which was then described as the “servicer” of the note at the behest of Fannie Mae.

There was no evidence that MERS was ever the owner or holder of the note. Hence, under the Bain decision, MERS could not have been the beneficiary. Bain left open the issue of whether MERS could act as an agent of the lender or trustee, and in support of its motion for summary judgment defendants make that assertion here. More troubling is the role of ReconTrust. It was ReconTrust which issued the notice of default to the borrower. ReconTrust was not the trustee when that notice was issued. It’s undisputed that ReconTrust was, at all times, a wholly owned subsidiary of BANA. There’s no reason, or at least none that I could see, that would preclude ReconTrust from issuing a notice of default as an agent of BANA. But thereafter MERS named ReconTrust as the trustee. Or perhaps ReconTrust named itself as the trustee, since the signatory “G. Hernandez” was not an employee of MERS but rather was employed by ReconTrust. While the DTA appears to have been amended and arguably might permit a subsidiary to act as a trustee, the statutory requirement remains that the trustee be independent and not beholden to the lender or borrower. Acting as an agent of BANA and being a wholly owned subsidiary of BANA, it seems specious to attempt to argue that ReconTrust was an independent trustee.

And under what authority did MERS have the right to name that trustee? As the agent of BANA, having been named as the “nominee” by BANA’s predecessors in interest? The evidence either compels or strongly points to the conclusion that MERS was a separately owned corporation and acted independently; it was not owned by BANA, and I do not see where it owed any fiduciary obligation or fealty to BANA (or Fannie Mae for that matter). While there is evidence to support the claim that the defendants were following the servicing guidelines promulgated by Fannie Mae, that’s not tantamount to a claim that they were acting at the direction and control of the owner of this note.

Then there are the contradictory statements in the notices that were filed. BANA filed a declaration with ReconTrust which identified Fannie Mae as the owner and beneficiary of the deed of trust, yet ReconTrust later identified BANA as the beneficiary. Was that because of MERS purported assignment of the note in favor of BANA? What rights did MERS have to assign over to BANA the rights which presumably vested with Fannie Mae at that time? And if BANA somehow became the beneficiary, under what authority did ReconTrust, acting as the trustee, accept a credit bid from Fannie Mae at the foreclosure sale? Was that predicated on BANA’s assignment of the deed of trust some three weeks after the trustee’s sale? A primary reason for the requirement that the trustee have evidence to correctly identify the beneficiary of the deed of trust is so the borrower will know who he needs to contact to try to reinstate or resolve disputes about his loan, something which appears underscored by Mr. Bradburn’s stated belief that he had been current with his payments until advised to fall in arrears and his dispute about how far behind his loan had fallen.

The case law has consistently held that the DTA must be strictly followed. Absent a valid waiver of the protections under the DTA, the failure to materially comply with that statute renders a foreclosure sale pursuant to it invalid. While Mr. Bradburn did not avail himself of the ability to seek to enjoin the sale, I felt the failure to strictly follow the requirements of the DTA required setting aside this foreclosure sale, particularly the appointment of a trustee that was not independent. I could not find that Fannie Mae as the claimed owner of the underlying note was a bona fide purchaser for value, even if it was not complicit in the violations of the DTA.

Having found the foreclosure sale to be fatally flawed by defendants’ failure to strictly comply with the DTA, it follows a priori that plaintiff was “injured”. I believe plaintiff met his burden to show that defendants’ actions constituted an unfair or deceptive practice, that it occurred in a trade or commerce, and that those practices impacted the public interest. Insofar as plaintiff’s home was wrongfully sold, he was “injured”. The measure of his damages will need to be proven at trial. If he was in default in his loan and would have faced the loss of his home, he may yet face the same ultimate result. A jury may conclude that his damages are de minimus. And if he claims significant monetary damages, it will be up to plaintiff to prove causation, namely that those damages resulted from the wrongful conduct of defendants.

The memo that Fannie and Freddie stockholders never got–no future profits for you. Ever!

NYT –

Would you buy stock in a company that barred you from sharing in its future earnings? Of course not. Participating in the upside is what stock ownership is all about.

And yet, as of December 2010, holders of Fannie Mae and Freddie Mac common stock were subject to such a restriction by the United States government. They didn’t know it at the time, though, because the policy was not disclosed.

This month, an internal United States Treasury memo that outlined this restriction came up at a forum in Washington.

New remixed music video features Eminem, Ice Cube, Korn and Anonymous aligning forces to set off the Worldwide Wave of Action ~ https://WaveOfAction.org/ ~ 4.4.14

This video is made in accordance to Fair Use laws for non-profit, non-commercial, educational and socially beneficial use only. It is political speech, as protected by the 1st amendment of the US Constitution. This artist supported transformative video contains original and remixed material, with over 100 clips from many different videos. It is also protected by Anonymous and supported by the Digital Hip Hop Collective.

Do not think your nightmare is over because you have signed and returned a permanent loan modification. Loan servicers are notorious for failing to honor permanent loan modifications. In our experience, they’re all bad, but Bank of America is the worst.

Here’s how to improve your chances of getting your loan modification honored:

First, meticulously follow the instructions provided with your loan modification. No matter how nuanced and ridiculous the instructions are, follow them exactly. For example, one servicer provides a sheet titled “Instructions for Notary,” for which there are multiple versions, but some require any months to be spelled out. If you write “Dec.” or “12” instead of “December,” the servicer will tell you months later that you have not entered into a loan modification because you did not follow instructions. This is obviously a bad faith attempt to collect additional payments from you before foreclosing on you, but nonetheless, you must not give the servicer reasons to do so.

Second, make your payments distinctly identifiable to the modified payment. If you are paying by check, write in the memo line, for example, “June 2014 loan modification payment.” If you are paying by phone (because your ridiculous servicer requires you to), insist that they note the “June 2014 loan modification payment” information on your account. This can be crucial to successful litigation later. Your servicer will later defend your lawsuit on grounds that it never signed and returned the agreement (“statute of frauds” defense). Well, by following this advice, you are creating the “partial performance” exception to the statute of frauds defense.

Nevada has reached a $6 million settlement with Lender Processing Services Inc. that resolves the state’s civil action alleging the firm violated the state’s deceptive trade practices act, the state attorney general announced Friday.

The settlement also resolves all other outstanding issues or claims related to the litigation, Catherine Cortez Masto said in a statement. Lender Processing Services is now known as Black Knight Financial Services.

Nevada originally decided not to join a multi-state settlement with LPS signed in 2011 with 49 other states. LPS was recently acquired by Fidelity National Financial Inc., which allowed for negotiations to begin again, the attorney general said.

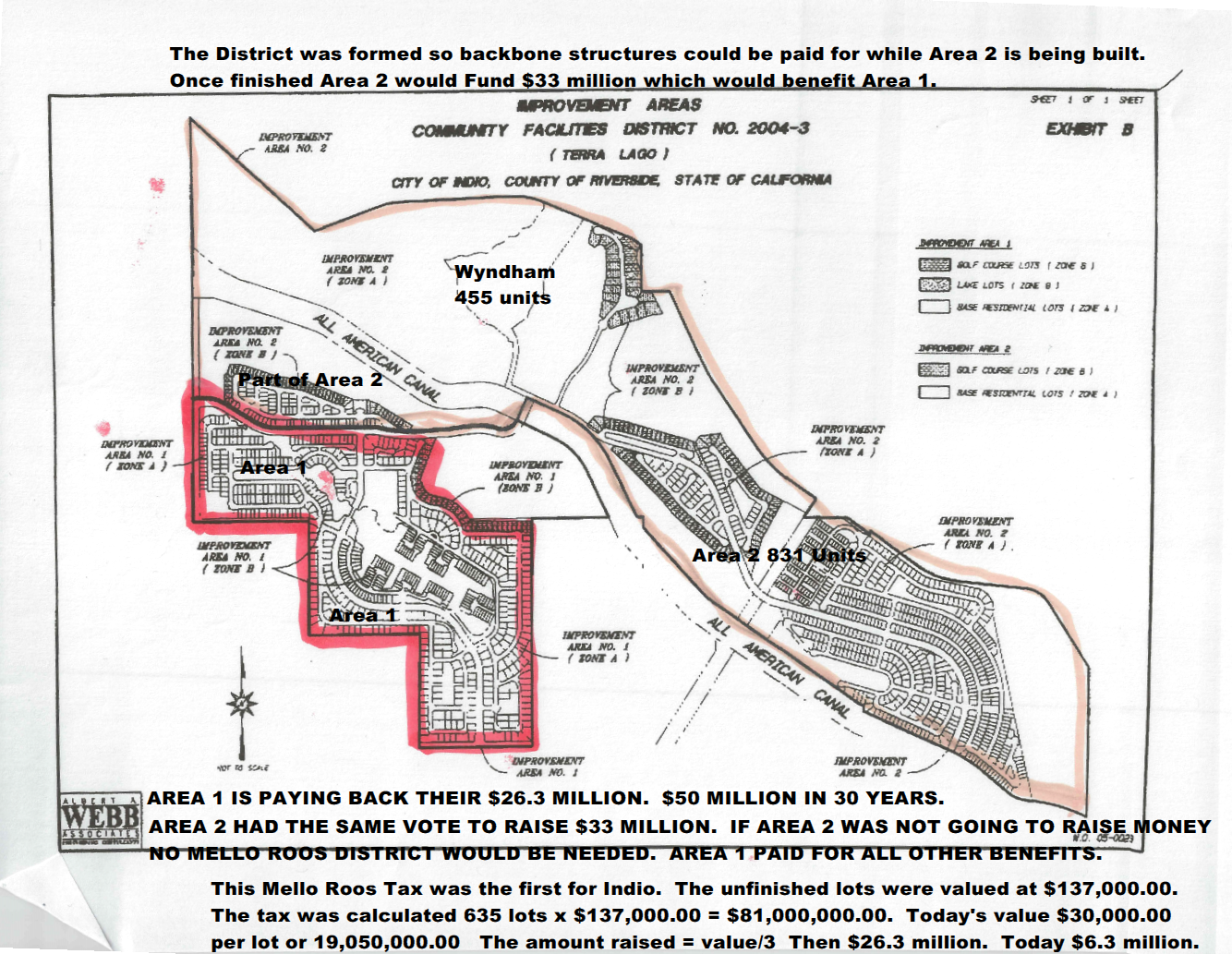

This is the Story of a botch Mello Roos Offering, the first for the City of Indio.

Indio Community Facilities District (CFD) 2004-3 is a Mello Roos Tax District issued by The City of Indio California, and it was their very first. An Intro to Mello Roos Tax Districts

Mello Roos Tax is an extra tax that a City may place on new development and the City gets say $26.3 million and splits it with the Developer.

Here they took $26.3 million, and used it for things that did not help the development.

It was 98% completed.

It was used to help another undeveloped area.

It was used to help the Indio Water Authority build its own infrastructure.

But should the undeveloped area pay it back?

The City says no.

That does not pass the smell test. Why would the City do that?

Rooftops, yes they want homes in Indio.

They now have a new developer and have worked out a secret deal which uses Area 1 money as credits for the new developer to build.

The builder will have no Mello Roos Tax.

The houses will sell for $70,000 more without the Mello Roos Tax.

Won’t that hurt Area 1 home sales?

Yes, that is why the fight.

by K. Hovnanian’s® Four Seasons at Terra Lago

New homes coming soon

K. Hovnanian’s Four Seasons at Terra Lago in Indio is our newest upcoming community for those 55 and better! This brand new collection of homes at Terra Lago will feature single family homes up to approximately 2,747 square feet and up to 4 bedrooms. These open home designs feature spacious living areas perfect for functional living. K. Hovnanian’s Four Seasons is known for its resort-style living, and that’s just what you’ll find at The Lodge clubhouse. Here you will experience incredible amenities such as a state-of-the-art fitness center with an aerobics/yoga studio, ballroom, beauty salon with massage room, and an indoor pool. Outdoors, you will find a resort-style pool with spa and cabanas, a bocce ball court, tennis courts, and so much more! This active adult community features fun activities, clubs and events for all of your interests including crafting, games, and more. Join our VIP Interest list to be among the first to receive updates on this exciting new community and start planning your move now! Call 888-408-6590! less

How is that possible?

The City issues a bond for the money and future residents or homeowners, who move in pay back the money over 30 years.

It is not easy to understand.

If there is a missed payment then the City can sell their house.

I forgot to mention, the Developer/landowner votes for the tax before they meet you.

This allows Developers and a City uses their tax exempt status to help issue bonds and every deal is done behind closed doors, and there is no oversight.

None?

No None!

Is there a Mello Roos Police? No and believe you me I have begged for help to expose the problem.

No one other than the lawyers who make money from it who understand it.

The Idea for the City (“ME”) to have instant money in their pockets and have future residents pay the bill over 30 years is appealing. To the City and Developer.

So what happened here?

It is really bad, and it would take a long to explain it.

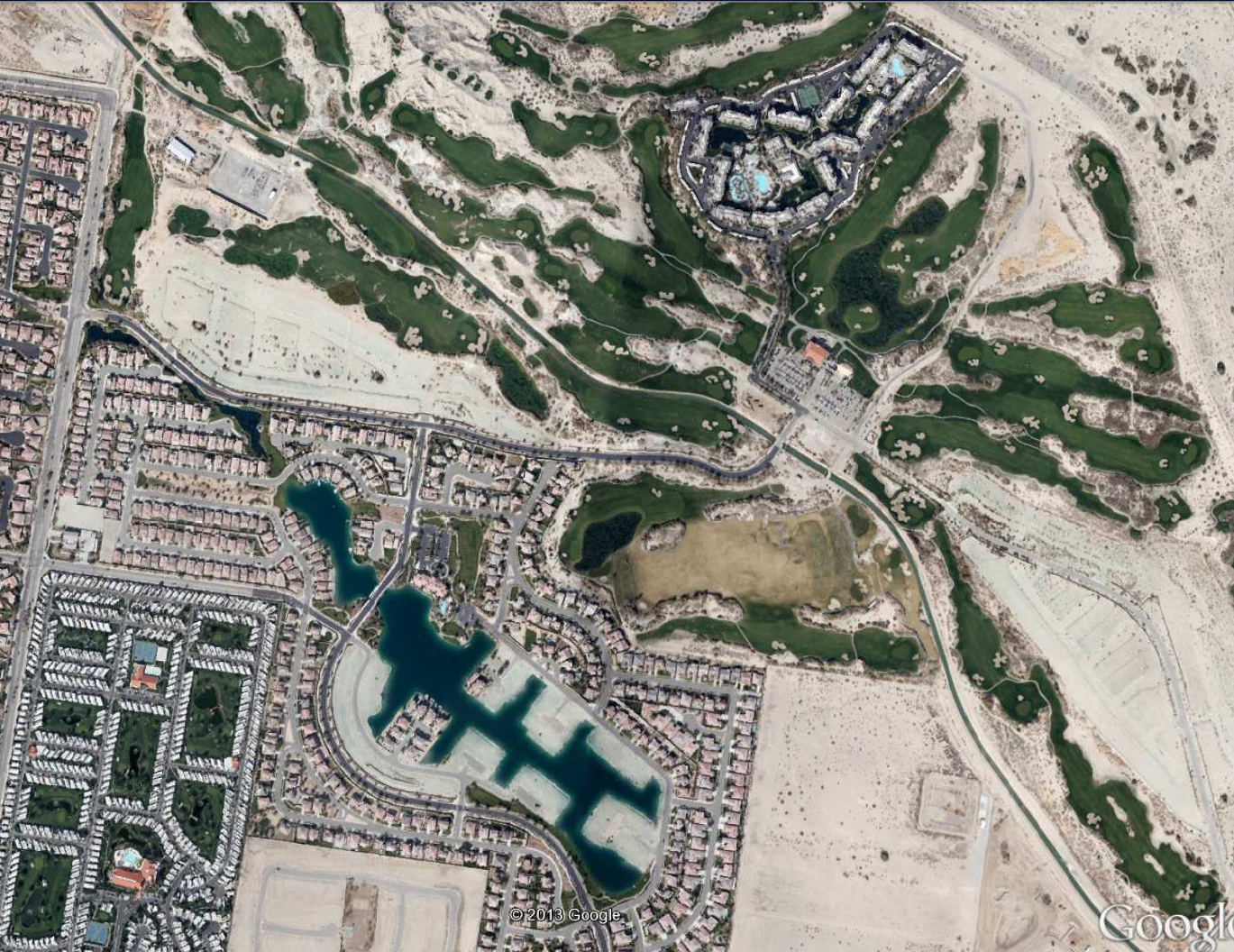

If you look at the map of Indio below, only 1 community pays $360.00 per month for 30 years. Or for that matter any Mello Roos Tax.

It paid for Wyndham Resorts Water problems and $9 million for others.

Certainly someone wants to pay them back. Don’t They? I mean it is only fair.

But who owns the properties?

Rabobank Na.A. in one of their various Limited Liability Companies

RB Indio Holdings, LLC or RB Terra Lago or even another with the builder K-Hovanian.

But they should be able to afford to pay more than the homeowners, shouldn’t they as they are a Bank and a major developer.

I guess we will see.

Area 1 Red – Area 2 Green -Wyndham Top

AREA 1 HOMEOWNERS PAY $360.00 PER MONTH FOR 30 YEARS AND ALL THE STREETS ARE PRIVATE.

98% of the infrastructures were in by the September 2005 $26.3 million funding.

And whats worse, there are also 110 lots owned by Rabobank, N.A. around the lake – &- they don’t pay either.

The City has made us fight to get anything.

Why would the City of Indio be afraid if they did all of this correctly and the money spent as they say?

Why would they not do a Forensic Audit?

Why not get a Bond Counsel Involved instead of the City Attorney?

Those are good questions and the City just ignores those questions.

If you just watch the recent council meeting on February 4, 2014, you would see what I believe are lies that the City Attorney is spouting or pontificating.

But what are you going to do?

Keep Fighting.

I bet you are getting paid alot to do this aren’t you?

No I am sorry to say but someone must do it so other will be protected, the Mello Roos Laws certainly don’t do it.

We must fight again.

WHO GOT THE MONEY – – -THE CITY OF INDIO.

AREA 1 LEFT EMPTY 110 LOTS AROUND THE LAKE. THEY DO NOT PAY ANYTHING. AREA 2 AND WYNDHAM RESORT PAY NOTHING AND BENEFIT.

Recent Comments